PHOTO

Hotel development activity across the Middle East continued to expand in the first quarter of 2026, led by Saudi Arabia and the UAE, as governments and investors pressed ahead with tourism diversification plans despite prevailing geopolitical tensions in the region.

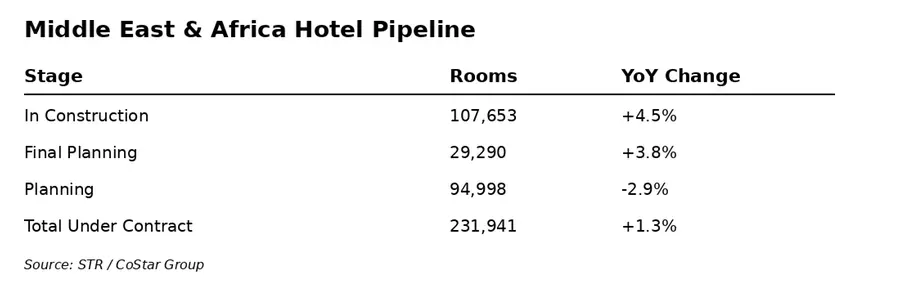

The Middle East and Africa region recorded 107,653 hotel rooms under construction at the end of March, up 4.5 percent year on year, while rooms in final planning rose 3.8 percent to 29,290, according to CoStar, a global provider of real estate data and analytics. Total hotel rooms under contract across the region stood at 231,941.

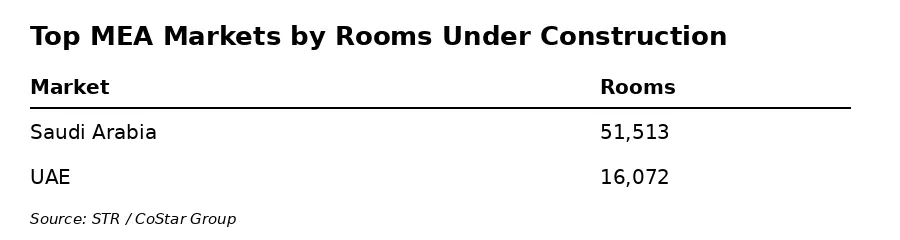

Saudi Arabia remained the region’s dominant market with 51,513 rooms under construction, accounting for nearly half of all active hotel development in the Middle East and Africa region, followed by the UAE with 16,072 rooms.

This comes as Saudi Arabia is targeting 150 million annual tourists by 2030 under Vision 2030, while the UAE continues to expand tourism, aviation and business travel infrastructure as part of broader economic diversification efforts.

“Continuous investment in hotel pipeline is required to ensure the successful realisation of the ambitious economic diversification plans and visions such as Dubai Economic Agenda D33 and PIF Strategy 2026-2030, for example,” said Kostas Nikolaidis, associate account director for the Middle East and Africa at STR.

“New supply to meet national demand targets. Greenfield Saudi giga projects like Red Sea, AlUla, Diriyah etc., are embedded in these masterplans and expected to help generate demand beyond traditional hubs like Makkah and transform the Kingdom into a global tourism destination,” he added.

Data from STR, CoStar Group’s hospitality analytics division, showed Saudi Arabia’s pipeline is spread across multiple segments, with upscale and luxury developments leading activity as the Kingdom accelerates tourism and hospitality investments tied to Vision 2030 projects.

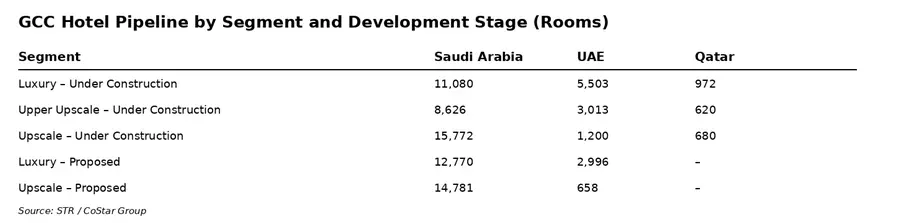

Saudi Arabia’s upscale segment accounted for 15,772 rooms under construction, followed by 11,080 luxury rooms and 8,626 upper-upscale rooms. The Kingdom also had 5,217 upper-midscale rooms under construction and 8,852 unaffiliated rooms in the pipeline.

In the planning stages, Saudi Arabia recorded 4,954 upscale rooms in final planning, 3,436 upper-upscale rooms, and 3,226 luxury rooms, while proposed projects included 14,781 upscale rooms, 12,770 luxury rooms, and 8,004 upper-midscale rooms.

The UAE pipeline also remained heavily weighted toward premium hospitality assets. Luxury projects accounted for 5,503 rooms under construction, alongside 3,013 upper-upscale rooms and 1,200 upscale rooms.

The country also had 1,718 luxury rooms and 551 upper-upscale rooms in final planning, while proposed developments included 2,996 luxury rooms, 1,746 upper-upscale rooms, and 658 upscale rooms.

Qatar’s pipeline was comparatively smaller but remained focused on high-end hospitality, with 972 luxury rooms and 620 upper-upscale rooms under construction.

The strong focus on premium hospitality assets reflects investor preference for high-value developments tied to flagship tourism destinations and large-scale mixed-use projects.

“The GCC hotel pipeline remains considerably skewed toward the top hotel classes such as luxury and upper upscale, reflecting a clear strategic focus on premium positioning and investor demand for high-value assets,” Nikolaidis said.

“The majority of the Saudi giga projects are positioned as predominantly luxury-led destinations with premium accommodation forming a core component. The luxury brand appeal is intentional as a lever to attract affluent leisure travellers and premium MICE demand,” he added.

Nikolaidis said the market is expected to gradually diversify into broader hospitality categories.

“In due course, the pipeline is expected to broaden into more midscale and lifestyle segments primarily in secondary cities,” he said.

Developers and operators are also closely monitoring geopolitical risks stemming from the ongoing US-Israel-Iran conflict, although the region’s hospitality sector has so far shown resilience against external shocks.

“The Middle East has demonstrated that it is not only resilient in the face of shocks such as Covid or the global financial crisis but also perfectly capable of emerging stronger,” Nikolaidis said.

“What differentiates the Middle East is the unwavering commitment to long-term development by governments, investors and developers to maintain momentum and reinforce the long term confidence in the hospitality sector,” he added.

Analysts expect hotel supply additions across Saudi Arabia and the UAE to accelerate over the next two to three years as giga-projects move closer to operational phases and international visitor targets continue to rise.

(Reporting by SA Kader; Editing by Anoop Menon)

(anoop.menon@lseg.com)

Subscribe to our Projects' PULSE newsletter that brings you trustworthy news, updates and insights on project activities, developments, and partnerships across sectors in the Middle East and Africa.