The reliance on oil revenues constitutes a long term risk for the Gulf countries

The Gulf Cooperation Council (GCC) countries are facing considerable pressure from the ongoing slump in oil prices, as they are heavily dependent on oil and gas revenues. Oil prices have been declining since the fourth quarter of 2014, falling around 48% year-on-year and raising concerns over how long GCC countries will be able to maintain their fiscal surplus positions. In the beginning of this year, the International Monetary Fund (IMF) downgraded its 2015 projection on GCC's consolidated fiscal surplus from $275 billion to around $100 billion, and warned that some countries will face fiscal deficits if public spending continued at current levels. Nevertheless, most GCC countries are still delivering high rates of economic growth, and managed to avoid a downturn so far due to the resilience of their governments' spending, which is supported by large fiscal reserves. Yet, their reliance on oil exports remains a downside risk on the long run, according to the IMF. The international organization stressed the importance of increasing economic diversification and strengthening the non-oil sectors in the GCC to sustain growth and maintain fiscal surplus in the distant future.

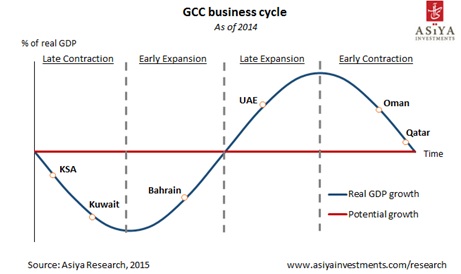

Gulf states share similar economic features, and lower oil prices have a major impact on the two GDP components that contribute the most to their economies, government spending and net exports. However, the evolution of private consumption and investment, which are less oil-driven, differs from one country to the next. As a result, GCC countries can be considered to be in different business cycle stages, in spite of their shared characteristics. The business cycle reflects the fluctuations of a country's real GDP growth in relation to its potential growth, and is defined in terms of expansion and contraction. When real GDP growth is trending upwards, the economy is considered to be in an expansion stage, while a downward trending of real GDP growth indicates a contraction stage. The expansion phase usually involves rising employment, industrial output, sales and personal income. We look at these factors in particular, isolating the direct impact of falling oil prices on GDP. There is a second parameter to take into account when analyzing business cycles. Countries below potential growth are underusing their resources. They usually present unemployment, unused manufacturing capacity and falling inflation. Countries above potential growth suffer from overheating, inflation and overused factories.

There are four out of the six GCC countries considered to be in the contraction stage as of the fourth quarter of 2014. More specifically, Oman and Qatar are in early contraction, defined as the beginning of an economic slowdown but still above their long-term growth rate. The deceleration is mainly due to weaker exports, and softening private consumption and investment. Leading indicators such as credit and liquidity growth suggest that the slowdown could continue for a prolonged time. Kuwait and Saudi Arabia have been decelerating as well, but their countries are considered to be in a later stage of contraction. They already show some signs of recovery in different sectors, such as the housing sector in Kuwait, and the banking sector in Saudi Arabia. Furthermore, leading indicators started to pick up, suggesting more spending and positive sentiment going forward.

Bahrain and the United Arab Emirates (UAE) ended the year in an expansionary cycle. . The slump in oil prices did not affect their export growth as much as in other GCC countries, due to the diversification of exported goods. The good momentum of their labour markets allowed the countries to experience strong private consumption, as a result of their healthy labor markets. Additionally, both countries present a positive outlook, in particular UAE, after it secured the organization of Expo 2020 and the stock market was upgraded by MSCI from the frontier markets index to emerging markets index.

Overall, oil continues to be the one factor driving economic performance in the GCC. Economic diversification is a key element for the Gulf countries to ensure future healthy growth. It is necessary for GCC governments to diversify their sources of income away from fossil revenue. Regional governments should continue to improve their legal and tax frameworks while ensuring a stable political framework. GCC authorities must set the conditions to engage the private sector, the only one that can address the upcoming challenge of demographic pressure and youth unemployment.

- Ends

IMPORTANT DISCLAIMER: The information contained in this report is prepared by the Research Department of the Asiya Investments is believed to be reliable, but its accuracy and completeness are not warranted. Research recommendations do not constitute financial advice nor extend offers to participate in any specific investment on any particular terms. Investors should consider this material as only a single factor in making their decisions.

About Asiya Investment:

Asiya Investments is a subsidiary of KCIC which was founded by an Emiree Decree with a capital of KD 80 million and a mandate to invest in domestic demand-driven sectors in Asia, namely energy, real estate, healthcare, infrastructure, and financial services. KCIC is the Parent Company of a Group that includes Asiya Investments Dubai Limited and Asiya Investments Hong Kong Limited. Asiya Investments Dubai Limited serves as the investment advisory hub for KCIC. Asiya Investments Hong Kong Limited is fully equipped with a skillful and experienced investment team which has further demonstrated KCIC's commitment to the Asian markets. The publicly-listed Group employs a team of Asia specialists and currently manages assets in excess of a billion. Key shareholders of KCIC include the Kuwait Investment Authority (Kuwait's Sovereign Wealth Fund), National Investments Company (one of the leading investment banks in the Middle East), and Alghanim Industries (one of the largest conglomerates in the Middle East).

Reporters may contact:

Leslie Mouawad

Bensirri PR

+965 99981334

leslie@bensirri.com

© Press Release 2015