PHOTO

- Egyptian M&A deal value goes up almost quadruples over 2017

- Egypt’s share of MENA deal value more than double last year’s share

- Egypt’s private equity buyouts gather pace

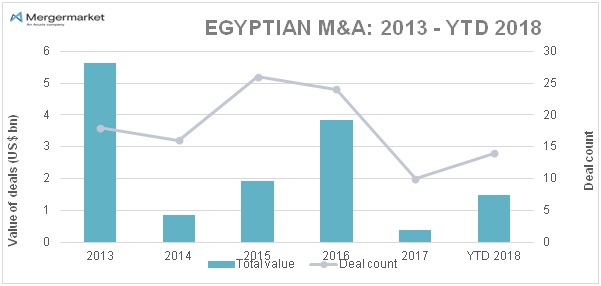

Cairo, Egypt: Mergermarket, the leading provider of M&A data and intelligence, has announced that Egypt’s M&A deal value has soared to US$ 1.5bn with 14 deals in total so far this year, overtaking 2017 which had only 10 deals worth US$ 389m. The bulk of this value came from the energy, mining and utilities sector, which saw two of the biggest deals of the year, Mubadala Petroleum’s acquisition of a 10% in the Zohr oil field from Eni; and SOCO International’s acquisition of Merlon Petroleum El Fayum Company. The data was announced at Mergermarket’s inaugural Egypt M&A and Private Equity Forum held in Cairo on 14th November.

The knock-on effect of a good year globally in M&A – because of cheap financing in developed economies which made leverage cheaper for companies in emerging markets, was evident in the Middle East and North Africa (MENA) region. The region’s deal value rose from US$ 15.9bn in 2017 to US$ 23.4bn in 2018 so far. Helped by favourable general macro-economic conditions, Egypt’s share in the MENA M&A deal value rose to 6.3%, over twice its share in 2017 (2.5%). 2017 was quite an eventful year for Egypt, with a number of domestic economic challenges taking its toll on M&A and private equity figures.

https://www.zawya.com/images/features/181114-EMP.jpg

Mohamed Khodeir, Partner & Head of Capital Markets at Al Tamimi commented: “The structural reforms to the investment climate in Egypt, as part of the Economic reform program, including reforms to subsidies, monetary and fiscal policies along with a new investment regime have all been factors boosting confidence of funds and private equity players in the Egyptian market.”

Heba Abdelrahman, Editor at Dealreporter commented: "As Egypt's economic reforms are beginning to bear fruit, the country provides an exciting opportunity for private equity practitioners and financiers in several sectors. Few countries can compare on turnaround, growth and population potential."

Mr. Hussein Choucri, Chairman and Managing Director at HC Securities & Investment commented: “M&A is a core activity of our firm and we follow its developments very closely. In this context, we believe the timing is right for cross-border M&A into Egypt given the stable political environment and improving economic outlook.”

Egyptian buyouts rose significantly since last year, a year of total inactivity in the Egyptian private equity market, likely linked to the market’s general lack of consistent yearly activity. So far this year, Egypt has seen four buyout deals worth a combined US$ 110m, more than 2016 (when there were only three deals worth US$ 40m) and 2017, when there were no private equity deals recorded in Egypt. An emerging trend in private equity is education, a sector which saw a significant acquisition of four international schools by EFG Hermes Private Equity worth US$ 56m.

Mohamed Gabr, Partner, Head of Corporate Commercial – Egypt at Al Tamimi & Company commented: “The Egyptian market is witnessing growing interest in the education sector, whether K-12 or higher education. The sector is producing solid returns on investment, and is largely unaffected by economic and political circumstances. The demand for quality private education is consistently on the rise. In the meantime, investment in education provides investors the opportunity to produce a positive social impact, which makes it even more attractive.”

-Ends-

About the inaugural Mergermarket Egypt M&A and Private Equity Forum

This forum is designed to encourage conversations driving the market in Egypt. From post-revolution deals to the growth in activity from the health and education sectors, this half-day event provides financial professionals in the region with the opportunity to take stock of the market and network with senior M&A and private equity professionals. The event is held on 14th November 2018 at the Ritz Carlton The Nile in Cairo in strategic partnership with Al Tamini & Co, HC Securities & Investment, EY-Parthenon. Visit https://events.mergermarket.com/egypt#agenda

About Mergermarket

M&A intelligence, data and research

In M&A, information is the most valuable currency. Mergermarket, an Acuris company, reports on deals 6-24 months before they become public knowledge, giving our subscribers a powerful competitive advantage. With the largest network of dedicated M&A journalists and analysts, Mergermarket offers the most comprehensive M&A intelligence service available today. Our reporters are based in 67 locations across the Americas, Europe, Asia-Pacific, the Middle East and Africa. Visit mergermarket.com.

Media Enquiries

Ioiana Luncheon

PR Manager, EMEA

Acuris

E: ioiana.luncheon@acuris.com

T: +44 (0)20 3741 1391

© Press Release 2018

Disclaimer: The contents of this press release was provided from an external third party provider. This website is not responsible for, and does not control, such external content. This content is provided on an “as is” and “as available” basis and has not been edited in any way. Neither this website nor our affiliates guarantee the accuracy of or endorse the views or opinions expressed in this press release.

The press release is provided for informational purposes only. The content does not provide tax, legal or investment advice or opinion regarding the suitability, value or profitability of any particular security, portfolio or investment strategy. Neither this website nor our affiliates shall be liable for any errors or inaccuracies in the content, or for any actions taken by you in reliance thereon. You expressly agree that your use of the information within this article is at your sole risk.

To the fullest extent permitted by applicable law, this website, its parent company, its subsidiaries, its affiliates and the respective shareholders, directors, officers, employees, agents, advertisers, content providers and licensors will not be liable (jointly or severally) to you for any direct, indirect, consequential, special, incidental, punitive or exemplary damages, including without limitation, lost profits, lost savings and lost revenues, whether in negligence, tort, contract or any other theory of liability, even if the parties have been advised of the possibility or could have foreseen any such damages.

{kind=link}