PHOTO

Solar project capex across the Middle East region is expected to increase by up to 3 percent with longer commissioning timelines due to logistics disruptions linked to the Iran war, according to a Wood Mackenzie senior analyst.

In an opinion article, Yana Hryshko, Wood Mackenzie’s Senior Research Analyst and Head of Global Solar Supply Chain said developers and EPC [Engineering, Procurement and Construction] contractors are delaying shipments, revising delivery schedules and reassessing procurement timelines amid heightened risks along key maritime routes, rising freight rates and increased insurance costs.

“As a result, project CAPEX across the region is expected to increase by approximately 1–3 percent, with commissioning timelines extending by several months in some cases,” she said.

On Thursday, Reuters had reported that shipping traffic through Hormuz was at virtual standstill despite ceasefire.

Last month, major container shipping lines including Maersk, Hapag-Lloyd, and CMA CGM implemented emergency surcharges causing a sharp increase in container shipping costs to the Gulf.

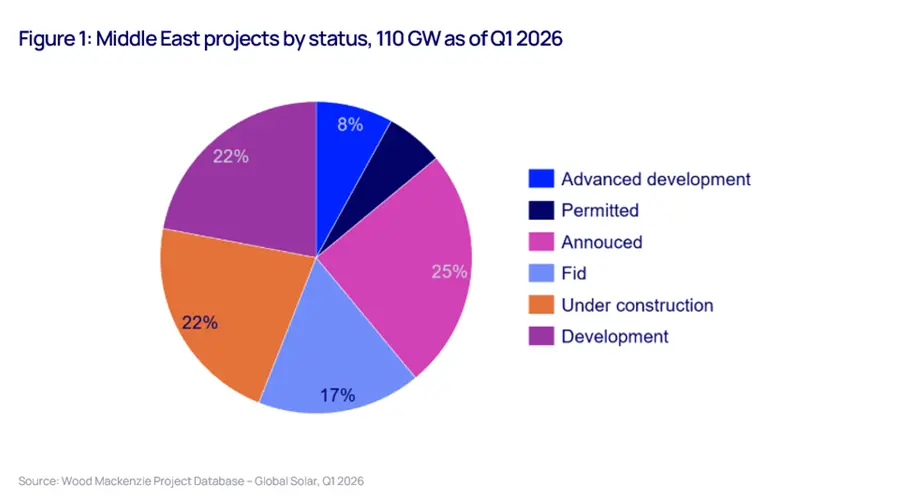

110GW pipeline

Wood Mackenzie estimates that approximately 110 GW of solar capacity in the Middle East is currently in execution or various stages of development.

“While impacts are most immediate for projects under construction, the broader pipeline is increasingly exposed to delays, cost inflation, and supply uncertainty,” said Hryshko.

Manufacturing ambitions

At a structural level, war-related disruptions are also expected to impact the Middle East's emerging solar manufacturing sector, and the broader global supply chain diversification agenda.

This burgeoning industry had attracted over 30GW of planned capacity investments across modules, cells and upstream segments, driven by the region's low-cost energy, industrial policy support and proximity to key markets.

Hryshko noted that the current disruptions are delaying project timelines, deferring investment decisions and shifting focus toward short-term operational stability.

She underlined that the impact extends beyond module assembly.

“The development of supporting component supply chains - including solar glass, aluminium frames, and mounting structures - is also being delayed. These components are critical for achieving cost-competitive, localised production. Without them, manufacturing remains dependent on imported inputs and structurally less competitive.”

Reliance on China

In the longer term, delays in manufacturing expansion in the Middle East are expected to extend the timeline for global supply chain diversification while reinforcing reliance on established supply chains, particularly in China.

“Rather than accelerating the transition toward a more distributed manufacturing base, the Middle East conflict is likely to delay that transition and reinforce existing supply concentration, at least over the next investment cycle,” Hryshko concluded.

(Editing by Anoop Menon) (anoop.menon@lseg.com)

Subscribe to our Projects' PULSE newsletter that brings you trustworthy news, updates and insights on project activities, developments, and partnerships across sectors in the Middle East and Africa.