PHOTO

At times of intensified uncertainty and dispersion like today, investing becomes less about forecasting and more about favouring more liquid, high quality assets that can be resilient across a variety of scenarios.

Global growth has been more resilient than expected despite growing divergence below the surface. What has changed is the addition of a major new source of risk: the conflict in the Middle East. If this proves to be a short-term disruption, as markets are currently pricing, then the baseline outlook still assumes moderate global growth. However, a prolonged disruption would pose more significant challenges and increase global recession risks.

Geopolitical risks tend to transmit to the economy through changes to consumer and business confidence, financial conditions, and – most importantly today – energy prices. The Strait of Hormuz, a critical waterway for oil and energy shipments, remains effectively blocked. Similar to Russia’s invasion of Ukraine in 2022, this threatens to spark a global energy supply shock.

Energy supply shocks are stagflationary

Unlike in 2025, when divergent trends left global growth broadly unchanged, the Middle East conflict is likely to be stagflationary, lifting inflation while hurting growth. We see four main transmission channels: higher energy and food prices; disrupted supply chains and trade flows; tighter financial conditions; and lower business and consumer confidence.

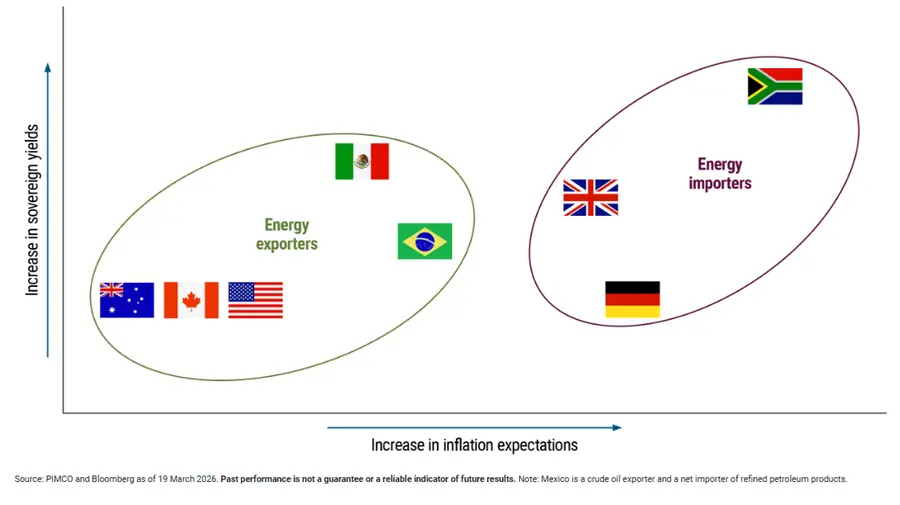

Negative oil supply shocks are inflationary for all economies, while growth effects will differ. Higher energy prices are stagflationary for net oil importers – transferring income abroad through more expensive energy imports while reducing household real (inflation-adjusted) income and business real profit – and expansionary for net oil exporters.

Within developed markets, Europe, the U.K., and Japan are energy importers and face larger downside growth risks. Canada and Australia should benefit from their net energy export status. Two decades of shale production increases have turned the U.S. from a net energy importer to a slight exporter. However, the U.S. is still a large economy with an energy sector as opposed to a commodity economy. Since energy is an important input into all goods it imports, the U.S. will likely still behave as a net energy importer to some extent.

Figure 1: Changing rates and inflation expectations affect energy importers the most. Chart shows the rise in sovereign yields and inflation expectations since the Iran conflict.

Central banks face a tug of war – but this isn’t 2022

The risk of higher inflation alongside lower growth puts central banks in a tricky spot. Conventionally, central banks tend to look through supply shocks, especially in economies that are net energy importers. After the elevated post-pandemic inflation period, however, central banks will be closely focused on the risk that a large supply shock could lead to more persistent pressures as inflation expectations and wages also adjust higher.

Yet economies are in much different positions than they were in 2022. At that time, the world was still dealing with pandemic-related pent-up demand, and governments had injected trillions of dollars into the private sector. The result was a large demand shock on top of a large supply shock. Labor markets were also extremely tight, driving both nominal wages and prices higher.

Today, by contrast, fiscal policy is tight across many regions as elevated post-pandemic sovereign debt forces restraint. Labor markets are much looser. Monetary policy is already neutral to slightly restrictive across most developed market economies.

As a result, economies are much more likely to adjust to the current shock through lower real incomes, weaker nominal wage adjustments, and greater recessionary risks.

Investment implications: resilience, quality, and liquidity

This is not an environment set up to reward bold forecasts or narrow bets. Instead, today’s conditions favour more liquid, high quality portfolios built to weather shifts in market sentiment and a range of potential outcomes.

Resilient headline growth alongside widening dispersion strengthens the case for high quality fixed income. Starting yields are much higher today than in 2022, providing cushion against inflationary tail scenarios and strengthening the role of bonds as both a return generator and a hedge against downside risks.

Markets rarely price geopolitical risk well. When there is a global shock, portfolio liquidity can allow investors to take advantage of market inefficiencies and valuation gaps that arise. As volatility rises and dispersion widens, the ability to manage downside risk and redeploy capital as conditions evolve matters more than trying to capture incremental yield by forfeiting liquidity.

High quality bonds once again play a meaningful role in portfolios and look attractive across a variety of economic scenarios. For portfolios that have drifted heavily toward equities, this is a practical moment to consider rebalancing. Yields across more liquid fixed income remain attractive, laying a solid foundation for market-driven income and return.

We prefer a modest overweight to duration and more balanced curve exposure, as yields look attractive across a range of maturities.

The case for global diversification remains strong. Differences across countries are widening, creating both risks and opportunities.

Looking across the continuum of public and private credit today, we see the greatest value in areas including U.S. agency mortgage-backed securities (MBS), investment grade issuers with stable, predictable cash flows, and high quality securitized credit.

Currency positioning matters more in this environment, particularly given the growing divergence between energy exporters and importers. Inflation-sensitive assets also deserve a more deliberate role in portfolios today. Commodities, real assets, and Treasury Inflation Protected Securities (TIPS) can help hedge real-world purchasing power and diversify returns when traditional asset relationships become less reliable. These exposures may help improve portfolio resilience.

Conclusion – recentre towards fixed income?

This is a market that rewards preparation for an uncertain set of outcomes. Higher yields, wider dispersion, and greater volatility create a favourable backdrop for active management when portfolios are built with liquidity and flexibility in mind.

For investors, this is a moment to consider recentring portfolios toward fixed income, to use global diversification and inflation tools intentionally, to treat liquidity as an asset, and to emphasise quality and resilience in the face of layered uncertainty.

Disclosures

Past performance is not a guarantee or a reliable indicator of future results.

All investments contain risk and may lose value. Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and low interest rate environments increase this risk. Reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. Inflation-linked bonds (ILBs) issued by a government are fixed income securities whose principal value is periodically adjusted according to the rate of inflation; ILBs decline in value when real interest rates rise. Treasury Inflation-Protected Securities (TIPS) are ILBs issued by the U.S. government. Mortgage- and asset-backed securities may be sensitive to changes in interest rates, subject to early repayment risk, and while generally supported by a government, government-agency or private guarantor, there is no assurance that the guarantor will meet its obligations. References to Agency and non-agency mortgage-backed securities refer to mortgages issued in the United States. Investing in foreign-denominated and/or -domiciled securities may involve heightened risk due to currency fluctuations, and economic and political risks, which may be enhanced in emerging markets. Currency rates may fluctuate significantly over short periods of time and may reduce the returns of a portfolio. Commodities contain heightened risk, including market, political, regulatory and natural conditions, and may not be appropriate for all investors. Equities may decline in value due to both real and perceived general market, economic and industry conditions. Private credit involves an investment in non-publicly traded securities which may be subject to illiquidity risk. Portfolios that invest in private credit may be leveraged and may engage in speculative investment practices that increase the risk of investment loss. Investments in asset-based lending and asset-backed instruments are subject to a variety of risks that may adversely affect the performance and value of the investment. These risks include, but are not limited to, credit risk, liquidity risk, interest rate risk, operational risk, structural risk, sponsor risk, monoline wrapper risk, and other legal risks. Asset-backed securities may not achieve business objectives or generate returns, and their performance can be significantly impacted by fluctuations in interest rates. The value of real estate and portfolios that invest in real estate may fluctuate due to: losses from casualty or condemnation, changes in local and general economic conditions, supply and demand, interest rates, property tax rates, regulatory limitations on rents, zoning laws, and operating expenses. Bank loans are often less liquid than other types of debt instruments and general market and financial conditions may affect the prepayment of bank loans, as such the prepayments cannot be predicted with accuracy. There is no assurance that the liquidation of any collateral from a secured bank loan would satisfy the borrower’s obligation, or that such collateral could be liquidated. Management risk is the risk that the investment techniques and risk analyses applied by an investment manager will not produce the desired results, and that certain policies or developments may affect the investment techniques available to the manager in connection with managing the strategy. The credit quality of a particular security or group of securities does not ensure the stability or safety of an overall portfolio. Diversification does not ensure against loss.

Forecasts, estimates and certain information contained herein are based upon proprietary research and should not be interpreted as investment advice, as an offer or solicitation, nor as the purchase or sale of any financial instrument. Forecasts and estimates have certain inherent limitations, and unlike an actual performance record, do not reflect actual trading, liquidity constraints, fees, and/or other costs. In addition, references to future results should not be construed as an estimate or promise of results that a client portfolio may achieve.

Statements concerning financial market trends or portfolio strategies are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will work under all market conditions or are appropriate for all investors and each investor should evaluate their ability to invest for the long term, especially during periods of downturn in the market. Investors should consult their investment professional prior to making an investment decision. Outlook and strategies are subject to change without notice.

Correlation is a statistical measure of how two securities move in relation to each other. Duration is the measure of a bond's price sensitivity to interest rates and is expressed in years. A K-shaped recovery is when segments of an economy recover from a recession at different rates. References to liquidity refer to normal market conditions. A “safe haven” is an investment that is perceived to be able to retain or increase in value during times of market volatility. Investors seek safe havens to limit their exposure to losses in the event of market turbulence. All investments contain risk and may lose value.

For professional use only

Per the information available to us you fulfill the requirements to be classified as professional clients as defined in the MiFiD II Directive 2014/65/EU Annex II Handbook. Please inform us if otherwise. The services and products described in this communication are only available to professional clients as defined in the MiFiD II Directive 2014/65/EU Annex II Handbook and its implementation of local rules and as defined in the Financial Conduct Authority's Handbook. This communication is not a public offer and individual investors should not rely on this document. Opinion and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. We believe the information provided here is reliable, but do not warrant its accuracy or completeness.

This material contains the opinions of the manager and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed.

PIMCO Europe Ltd (Company No. 2604517, 11 Baker Street, London W1U 3AH, United Kingdom) is authorised and regulated by the Financial Conduct Authority (FCA) (12 Endeavour Square, London E20 1JN) in the UK. The services provided by PIMCO Europe Ltd are not available to retail investors, who should not rely on this communication but contact their financial adviser. Since PIMCO Europe Ltd services and products are provided exclusively to professional clients, the appropriateness of such is always affirmed. PIMCO Europe GmbH (DIFC Branch) (Company No. 9613, Index Tower Floor 10, unit 1001 Dubai International Financial Centre, Dubai, United Arab Emirates) are regulated by the Dubai Financial

Services Authority ("DFSA") (Level 13, West Wing, The Gate, DIFC) in accordance with Art. 48 of the Regulatory Law 2004. The services provided by PIMCO Europe GmbH are available only to professional clients as defined in Section 67 para. 2 German Securities Trading Act (WpHG). They are not available to individual investors, who should not rely on this communication. According to Art. 56 of Regulation (EU) 565/2017, an investment company is entitled to assume that professional clients possess the necessary knowledge and experience to understand the risks associated with the relevant investment services or transactions. Since PIMCO Europe GMBH services and products are provided exclusively to professional clients, the appropriateness of such is always affirmed.

No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America LLC in the United States and throughout the world. ©2026, PIMCO