PHOTO

Geneva -- The International Air Transport Association (IATA) released data for May 2026 global air cargo markets showing:

- Total demand, measured in cargo tonne-kilometers (CTK), increased by 6.0% compared to May 2025 levels (6.5% for international operations).

- Capacity, measured in available cargo tonne-kilometers (ACTK), increased by 1.9% compared to May 2025 (2.8% for international operations).

“Air cargo demand grew 6% year-on-year in May, with Africa, Asia-Pacific, Europe, and North American regions all reporting above trend growth. Carriers in the Middle East, however, reported a combined contraction of 8.9% year-on-year as war-related impacts continued.

May’s strong performance coupled with macro-economic factors give cautious optimism for air cargo’s prospects over the remainder of the year. Trade and manufacturing output are both growing. Airlines have adapted operations to align with shifting demand patterns and supply chain needs. Meanwhile, yield growth and higher load factors are helping to recoup higher fuel costs. It’s still a tough year, particularly as Middle East uncertainties weigh heavily on parts of the industry, but robust demand and airline resilience are clear,” said Willie Walsh, IATA’s Director General.

Several factors in the operating environment should be noted:

- Global trade increased by 5.0% year-on-year, extending 25 months of consecutive annual growth.

- Jet fuel prices fell by 16.3% month-on-month in May but remained 93.5% above year-earlier levels.

- Global manufacturing activity remained supportive in May, but export orders weakened. The Global Manufacturing Output Purchasing Managers’ Index (PMI) rose to 53.5, while the New Export Orders Index stayed below the 50-mark at 49.6, suggesting air cargo growth was supported by selected trade flows rather than a broad-based rise in global exports.

May Regional Performance

Asia-Pacific airlines saw an 8.0% year-on-year growth in air cargo demand in May. Capacity increased by 5.1% year-on-year.

North American carriers saw a 10.5% year-on-year increase in air cargo demand in May. Capacity increased by 2.4% year-on-year.

European carriers saw a 6.7% year-on-year increase in demand for air cargo in May. Capacity increased by 2.2% year-on-year.

Middle Eastern carriers saw an 8.9% year-on-year decrease in demand for air cargo in May, the weakest performance of all regions. Capacity decreased by 9.2% year-on-year.

Latin American and Caribbean carriers saw a 1.9% year-on-year increase in demand for air cargo in May. Capacity increased by 5.6% year-on-year.

African airlines saw a 13.3% year-on-year increase in demand for air cargo in May, the strongest performance of all regions. Capacity increased by 1.3% year-on-year.

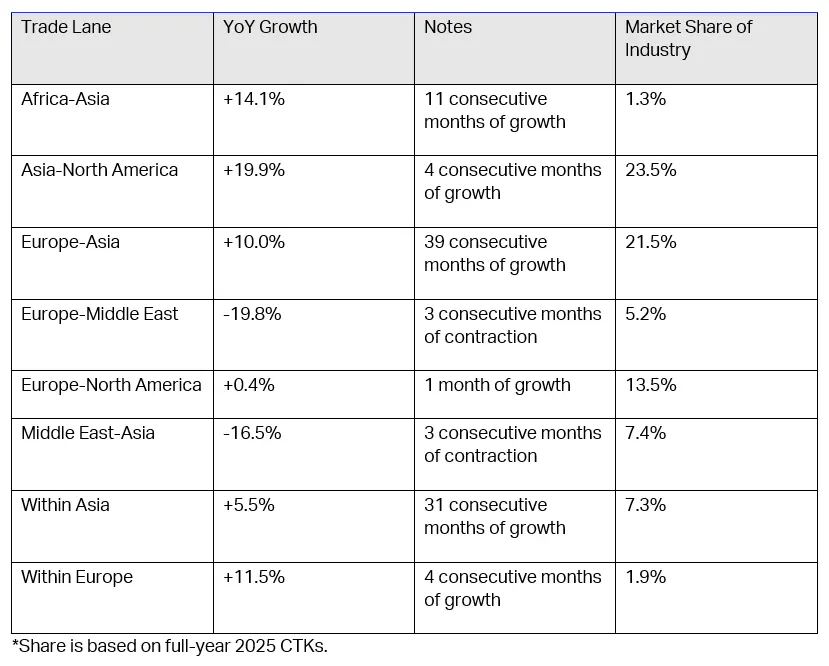

Trade Lane GrowthAir cargo performance diverged across major trade lanes in May. Asia-North America led growth followed by Africa-Asia, intra-Europe and Europe-Asia. In contrast, Gulf-linked corridors were still severely disrupted by the ongoing conflict in the Middle East.

For more information, please contact:

Corporate Communications

Email: corpcomms@iata.org

About IATA

- IATA (International Air Transport Association) represents over 370 airlines accounting for some 85% of global air traffic.

- You can follow us at follow us on X for announcements, policy positions, and other useful industry information.

- Fly Net Zero.

- Explanation of measurement terms:

- CTK: cargo tonne-kilometres measures actual cargo traffic

- ACTK: available cargo tonne-kilometres measures available total cargo capacity

- CLF: cargo load factor is % of ACTKs used

- IATA statistics cover international and domestic scheduled air cargo for IATA member and non-member airlines.

- Total cargo traffic market share (2025) by region of carriers in terms of CTK is: Asia-Pacific 35.8%, Europe 21.4%, North America 24.6%, Middle East 13.2%, Latin America and Caribbean 2.9%, and Africa 2.1%.