PHOTO

Abu Dhabi, UAE – The United Arab Emirates has initiated a transformative fiscal policy with the introduction of a federal corporate tax, aiming to cement its economic future’s resilience and prosperity. This strategic policy shift, outlined in Federal Decree-Law No. (47) of 2022, aligns with international tax standards and best practices, further solidifying the UAE's stature as a competitive global financial and business centre.

This new taxation framework, informed by extensive benchmarking and impact assessments, ensures public participation through a digital consultation phase. It spans the UAE’s free zones, which are integral to its diversified economic framework and international investment attractiveness. The tax policy is designed to amplify the UAE’s development as a global commerce and finance nexus by encouraging the free movement of capital and business expansion.

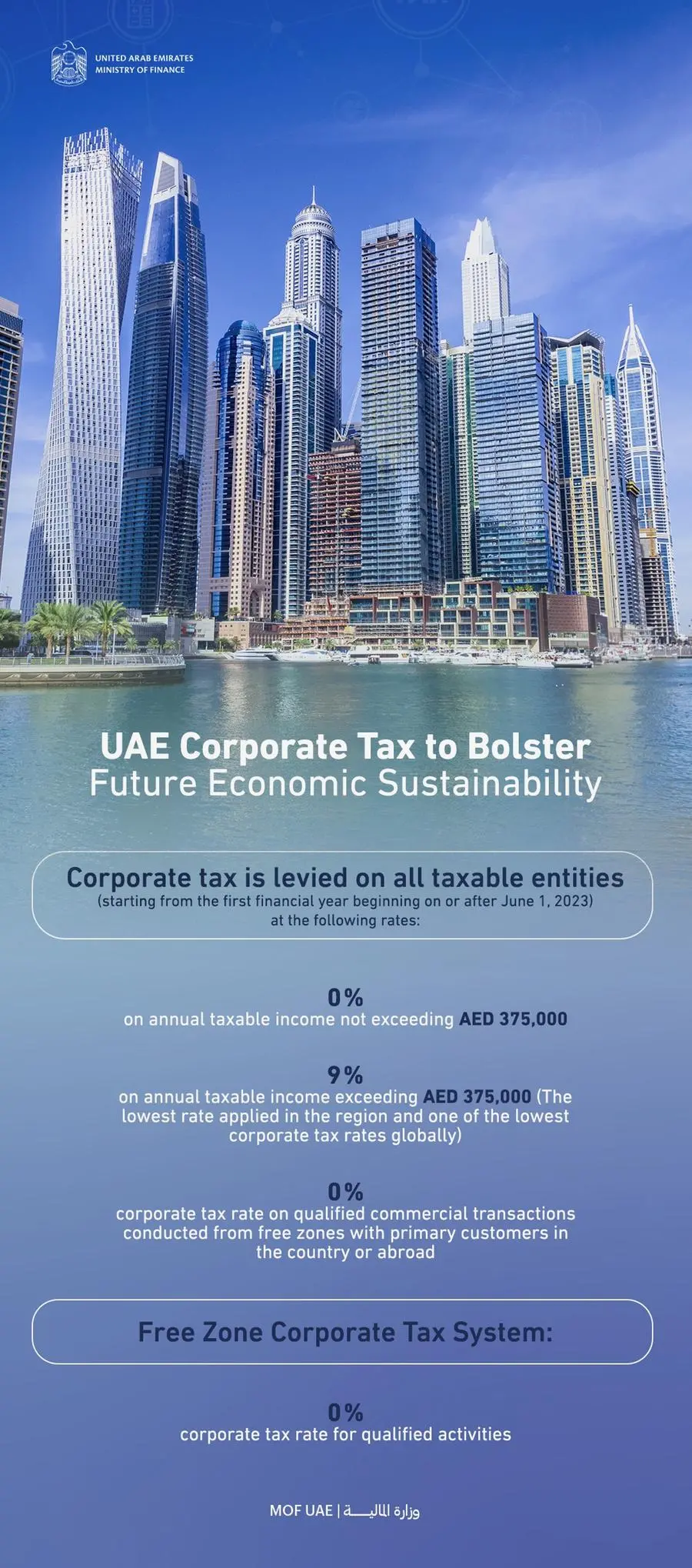

From June 2023, corporate tax stands levied at 0% for annual taxable incomes up to AED375,000 and 9% beyond that threshold. Free zone commercial transactions maintain the 0% rate, underscoring the UAE’s globally competitive tax environment. The OECD’s recognition of the UAE tax system within the top tier of 134 worldwide systems attests to its robustness and global alignment, particularly with the goals of the Base Erosion and Profit Shifting (BEPS) project.

The corporate tax’s vital role in sustainable development lies in its ability to foster a sustainable revenue base, advance the country’s strategic objectives, and uphold tax transparency and fairness. The legislative framework and subsequent regulatory decisions have been meticulously crafted, involving updates to existing tax procedures and regulations to improve societal, environmental, and fiscal health in coordination with the Federal Tax Authority.

Sustainable Development

The UAE has incorporated sustainable development goals as a cornerstone of its vision for the future, particularly within its National Agenda 2030. In 2019, the UAE established the National Committee for Sustainable Development Goals to oversee the implementation and progress of these goals on a national scale. This body actively involves stakeholders in the process. It regularly reports on the UAE’s progress, ensuring that sustainable development goals are interwoven with the nation's development priorities.

The committee evaluates the influence of tax policies on economic growth, and the UAE has been proactive in reforming these policies to address growth challenges, improve inclusivity, and support sustainable economic expansion. These reforms include simplifying the tax system and broadening its base, thus promoting a fair recovery and financial improvement.

Since October 2017, the UAE has broadened the range of goods subject to tax and has continuously updated tax regulations to increase taxpayer flexibility. Notably, it has reduced penalties for non-compliance with value-added tax and introduced a temporary exemption system offering a substantial reduction in fines.

In 2018, the UAE committed to the BEPS programme’s inclusive framework and supported the OECD’s Pillar Two initiative. This initiative establishes a global minimum corporate tax rate to prevent base erosion and profit shifting (BEPS), counter harmful tax practices, and promote global tax fairness.

The UAE has distinguished itself as a regional leader by initiating a public digital consultation on the global minimum tax, thus becoming the first country in its region to do so. This consultation encourages feedback from a broad spectrum of international stakeholders, reflecting the UAE’s commitment to crafting tax policies that support its strategic goals of competitiveness, ease of doing business, and investor confidence.

Strategic Directions and Partnerships

The UAE has introduced a federal corporate tax system as a key component of its broad transformational projects aimed at fortifying the nation's financial infrastructure to effectively manage future challenges and adhere to its national priorities. This initiative is a collaborative effort between the Ministry of Finance and the Federal Tax Authority, ensuring the efficient administration, collection, and enforcement of the new tax laws.

These reforms are part of the UAE’s strategy to bolster its economic resilience over the next decade and beyond, as it aspires to maintain its leadership in digital government innovation. The Ministry of Finance’s strategic plan for 2023–2026 is centred on financial sustainability, including developing balanced tax policies responsive to local and global economic trends.

The introduction of corporate tax is a proactive measure in response to the dynamic global economy, marked by volatility and financial uncertainty, including concerns over global financial stability, growing global debt, rising inflation, and the urgent need to confront climate change. The tax is designed to ensure financial sustainability and inclusivity for the future.

Mobilising public revenue through this corporate tax is crucial for the UAE, as it seeks to build stable and sustainable government revenue streams. Such financial stability is key to supporting projects that align with sustainable development goals, enhancing local resources, diversifying income sources, and ensuring a sustainable flow of finances. These measures are expected to positively impact the nation’s economy and society by funding developmental projects that contribute to the overall well-being and growth of the UAE.

Regulatory Decisions

Following the establishment of the federal corporate tax law in the UAE, the Cabinet and the Ministry of Finance have released over 25 detailed regulatory decisions to guide its implementation and clarify its provisions. Key decisions include exemptions from tax registration for certain entities, stipulations for taxable persons and companies in the free zone to maintain audited financial statements, and conditions under which non-residents are not deemed to have a permanent establishment in the UAE for tax purposes.

The Ministry has also outlined requirements for maintaining transfer pricing documentation and set forth conditions for corporate tax exemptions. It has established decisions regarding accounting standards, pension funds, social security, participation exemptions, transitional provisions for corporate tax, tax groups, interest deduction restrictions, and the tax treatment of joint ventures, foreign partnerships, family establishments, and intra-group transfers.

Furthermore, specific ministerial decisions address the tax treatment of resident and non-resident individuals, the conditions for investment funds, and the definition of public benefit entities eligible for corporate tax exemption. The Cabinet has also set administrative fines for violations of the corporate tax law, with significant penalties for delayed tax registration as determined by the Federal Tax Authority.

These decisions reflect the UAE’s dedication to creating a transparent, fair, and competitive tax environment that supports economic growth and affirms the country’s commitment to becoming a global trade and investment hub. The issuance of Cabinet Decision No. (74) of 2023 marks a significant update to the existing tax procedures, in line with the new Tax Procedures Law, ensuring that taxpayers are well-informed and compliant with the current tax system from its effectivity date.

Awareness and Consultation

The UAE Ministry of Finance is actively working to ensure that the business community understands the new federal corporate tax law, its framework, and its specific implications for various business sectors and taxpayer groups. The Ministry has initiated public awareness sessions for the general public and the media to demystify the provisions of corporate tax law and demonstrate its economic impact, covering both mainland and free zone areas.

Emphasising the necessity of accurate information, the UAE Ministry of Finance insists that official communication, such as releases and bulletins issued by both the Ministry of Finance and the Federal Tax Authority, should be the sole sources of information regarding the interpretation and application of Federal Decree-Law No. (47) of 2022 on corporate tax, its subsequent amendments, and related ministerial decisions. This approach underscores the government’s commitment to transparency and the correct dissemination of information concerning federal taxes in the UAE.