PHOTO

Dubai's real estate consultancies remain hopeful of better times ahead despite the fact that the five-year downward slump in prices shows no signs of abating.

Real estate consultancy JLL said in a press release accompanying its Q2 2019 UAE Market report on Monday that the market is likely to stabilise over the next 12 months, with the economy enjoying a slight uptick in GDP growth to 2.2% in the first quarter of 2019 and a series of new initiatives such as a new freehold law in Abu Dhabi and a new 'Golden Card' offering permanent residency likely to boost demand.

“Overall market sentiment should improve in the long run with the announcement of stimuli such as the new visa regulations," JLL MENA research associate Dana Salbak said in the press release.

"While the benefits of these initiatives are not likely to have an immediate impact, we do expect some sectors of the real estate industry to pick up in the run up to 2020.”

JLL's report stated that around 400 Golden Cards had been issued during the quarter, but added that a further 6,800 cards are due to be issued by the end of the year.

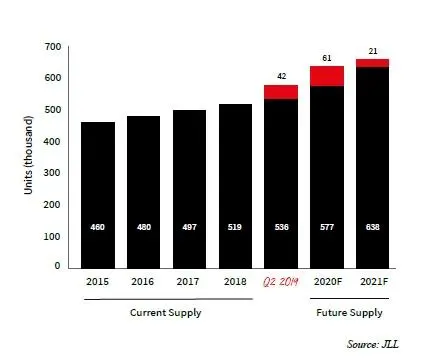

In Dubai, the report said both apartment and villa prices declined by 9% year-on-year, and that more than 6,800 new units had been added during the quarter (bringing the total number of new properties added so far this year to 17,000). A further 42,000 are scheduled to be delivered by the end of this year, which would bring the total number of units in Dubai to 577,000, and some 61,000 units are scheduled for delivery next year, meaning total units by the end of 2020 would reach 638,000.

However, the firm cautioned that it remained "cautious on timely delivery of future supply and delays can be expected".

Cavendish Maxwell's second quarter report, also published on Monday, was similarly cautious on the likelihood of timely delivery by developers.

Its Q2 report stated that just 2,950 Dubai apartments and villas were handed over during the last three months, bringing the total so far this year to 10,088. It expects "materialisation rates" - i.e. the actual number of units set to be delivered, to be between 40-50% of the projected rate, meaning that only 10,000-13,000 more units are expected to be delivered over the next six months, senior consultant Aditi Hariharan said in an emailed response to Zawya.

"In response to market demand, some projects which may be completed may not necessarily be handed over within the year," said Hariharan.

Cavendish Maxwell reported a 15.1% year-on-year decline in apartment prices and a 14.7% fall in apartment prices during the quarter.

It reported year-on-year rental declines of 12.5% for Dubai apartments and 12.6% for villas and townhouses and said that an expected increase in handovers of new units was "expected to continue to exert downward pressure on rents".

Dubai residential unit supply

More to offer

Yet even as developers extend the timeline of existing projects as market conditions worsen, developers are continuing to add new stock to the market, a Q2 report published by consultancy Asteco on Monday pointed out.

It said that it expects 17,000 residential units (12,000 apartments and 5,000 villas) to be added to Dubai's pipeline during the second half of 2019, adding to the 13,250 units (11,050 apartments and 2,200 villas) completed in the first half.

"Despite prevailing oversupply concerns, developers continued to launch new projects including One Park Avenue at Sobha Hartland (by Sobha Realty), Zada in Business Bay (by Damac) and Vincitore Benessere in Arjan (by Vincitore Realty)," Asteco's report said.

It also said Dubai apartment prices dropped 15% year-on-year, and villa prices dropped by 14%.

Other parts of the Dubai real estate market are also continuing to suffer from oversupply. JLL's report stated that vacancy rates for office space in the city's central business district increased by 3% year-on-year to 13% in Q2, while rents dropped by 10% to 1,510 per square metre per annum. Vacancy rate for retail space increased by 4% year-on-year to 18% of the total, while rents in prime centres dropped by 14% and rents in secondary centres fell by 24%. The amount of retail space in Dubai is set to increase by 42% within the next two and-a-half years to stand at 5.4 million sq m of gross leasable area by the end of 2021.

Although Abu Dhabi hasn't had to contend with the same problem of a burgeoning supply pipeline, there is still an overhang of space from the last boom that still needs to be filled, JLL's report shows.

In the office market, specifically, vacancy rates are now at more than one quarter (26%) of available space, and is forecast to rise further over the next 12 months. Grade A rents have declined by 6% over the past 12 months to 1,605 dirhams per sq m per annum. Vacancy rates in retail centres has also increased by 8% to 23% of total stock, with average rent declining by 5% and tenant demand remaining "weak".

Residential supply remains relatively muted, with just 2,420 units delivered during the first half of the year, but demand continues to be weak. Apartment sale prices in the capital are down 15% year-on-year, and villa sale prices are 14% lower, according to JLL. Rents have also declined by 12% and 14% respectively.

“While the residential sector in both Abu Dhabi and Dubai witnessed subdued performance overall, new initiatives to drive expat home ownership will likely boost demand," JLL's Salbak said. "The office sector, too, will witness potential upside from these new initiatives launched to stimulate the economy.”

(Reporting by Michael Fahy; Editing by Mily Chakrabarty)

Our Standards: The Thomson Reuters Trust Principles

Disclaimer: This article is provided for informational purposes only. The content does not provide tax, legal or investment advice or opinion regarding the suitability, value or profitability of any particular security, portfolio or investment strategy. Read our full disclaimer policy here.

© ZAWYA 2019