PHOTO

Dubai: Alpen Capital, an investment banking advisory firm, announced the publication of its report on the GCC Insurance Industry. The report showcases the current state of the insurance industry across the GCC nations while presenting the recent trends, growth drivers and challenges. The report also provides an outlook of the industry until 2021. It profiles some of the prominent insurance providers in the region while evaluating their financial and market valuation metrics.

The GCC insurance sector maintains resilient growth, given the significant penetration gap compared to the advanced economies and despite challenges such as drop in oil prices and reduced, public and business spending. Nevertheless, developing regulations, economic diversification efforts, mandatory health insurance and favorable demography present a bright outlook for the sector. The GCC Insurance industry is stepping into the next phase of growth, fueled by rising insurance awareness, economic revival and infrastructure developments and an expanding consumer base. Further, the maturing and stringent regulatory environment is likely to create strong, stable and sustainable business models”, says Sameena Ahmad, Managing Director, Alpen Capital (ME) Limited

“The GCC insurance sector has started showing signs of consolidation following the strengthening regulatory landscape. The trend is gathering momentum due to stringent reserving and solvency requirements in some countries. The M&A activity in the GCC insurance sector has picked up in the last couple of years, as companies are looking for strategic expansion or mergers to form stronger entities. In addition to intraregional deals, the region witnessed several cross-border acquisitions, wherein overseas insurers acquired stakes in local companies to penetrate the market. Regional players also made a few strategic investments in foreign companies to diversify geographic presence”, says Siraj Bhavnagarwalla, Managing Director, Alpen Capital (ME) Limited

Industry Outlook

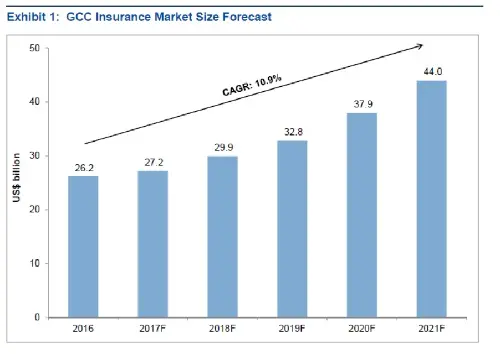

According to Alpen Capital, the GCC insurance market is projected to grow at a CAGR of 10.9% from US$ 26.2 billion in 2016 to US$ 44.0 billion in 2021. This projection is based on existing fundamentals of the industry and economic outlook.

The growth in GWP is likely to be moderate in 2017, as the industry players are adapting to the new regulations amidst increasing competition and recovering economic activity. On one hand, increased capitalization requirement and actuarial pricing are improving the financial performance of insurers and on the other hand, the regulations are encouraging consolidation activity.

Country wise forecast

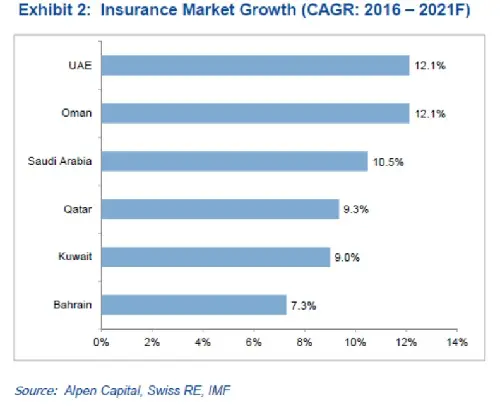

Between 2016 and 2021, insurance markets in the UAE and Oman are anticipated to grow at the fastest annualized average pace of 12.1%, followed by Saudi Arabia at 10.5%.

The premium growth in Oman is likely to be driven largely by the introduction of mandatory health insurance and that in the UAE by new motor insurance pricing regime. Additionally, macro factors like population growth, infrastructure developments and revival of business activity will aid growth across the countries. While the market rankings of the countries are not expected to change through 2021, the share of UAE and Oman are likely to expand and that of others may contract.

Life and Non-Life Insurance forecast

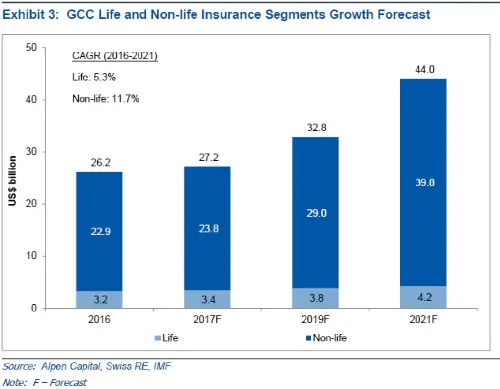

The non-life insurance market is expected to grow at a rapid CAGR of 11.7% between 2016 and 2021). At US$ 39.8 billion in 2021, the segment will comprise 90.4% of the total insurance market, an increase of 2.8 ppts from 2016.

During the forecast period, the life insurance GWP is projected to grow at an annual average rate of 5.3% to US$ 4.2 billion.

Insurance Penetration and Density

Insurance penetration in the region is forecasted to expand from 1.9% in 2016 to 2.5% in 2021. The expansion is driven by an improvement in penetration of non-life insurance to 2.3%, while that of life insurance is expected to remain stable at 0.24%.The penetration rates continue to remain below the international average, presenting immense scope of growth. Insurance density in the region is anticipated to increase at a CAGR of 8.4% to US$ 729.6, of which life insurance density is projected at US$ 69.7 and non-life density at US$ 659.9.

Growth Drivers

Economic diversification efforts have intensified in the GCC to build a sustainable economy in view of the low oil price environment. This has given a boost to construction activities across sectors, with the total active projects estimated at US$ 2.4 trillion. Completion of such projects is likely to create a large base of insurable assets, thus providing underwriting opportunities to insurance firms.

Mandatory health insurance has boosted the GWP in the UAE in recent years and in Saudi Arabia in the past. A gradual implementation of such law in the other GCC countries is likely to steer industry growth, as health insurance business accounts for ~40% of the GCC insurance market.

The GCC insurance market is becoming competitive with its evolving regulatory landscape. Regulations such as risk-based capital reporting and actuarial-led pricing are likely to improve the financial strength and market conduct of the firms and build stronger business models in the long term.

A growing population (comprising young and working people), rising urbanization and high disposable incomes are the factors driving demand for life and non-life insurance products in the GCC. The consumer base is set to grow further, with an anticipated addition of 6.5 million people by 2021.

As a large number of people in the GCC are Muslims, demand for Takaful insurance has been on the rise in the region. Family Takaful, in particular, has significant opportunities, given the underpenetrated life insurance market.

In view of high cession rates in the GCC and financial as well as tax incentives offered by autonomous financial centers in Dubai and Qatar, foreign reinsurance and management firms are attracted to these centers to lend their underwriting capabilities. As the business base grows, new reinsurers are likely to set up branches in these hubs and support the advancement of the insurance sector.

Challenges

Though the GCC Insurance sector is on a sustainable growth path, it is not devoid of challenges.

Fall in oil prices and the ensuing austerity measures have disrupted economic activity in the GCC and subsequently the underwriting business.

The GCC insurance sector is intensely competitive as well as concentrated, with the top five insurers in each GCC country, barring Bahrain, accounting for over 60% of the market. Moreover, a less diversified product portfolio has led to price competition in motor and medical insurance lines and hence, high loss ratios.

The GCC insurers are challenged by a shortage of skilled workforce as well as high staffing cost and attrition rates. Inability to hire the candidates with requisite skills could affect the growth of the sector.

Insurance firms in the UAE, Qatar and Kuwait have high exposure to equity and real estate investments, making them prone to economic shocks. As a result, Investment income of many such insurers has declined in the recent years.

The insurers are likely to face an increase in operating cost in the short term, as they will have to make operational changes to comply with the new regulations.

Each GCC country is making an attempt to improve regulations; however, there is a dire need for the regulations to be homogenous. To facilitate a level playing ground for all the insurers, the GCC countries need to harmonize as well as modernize their insurance regulations by adopting best international practices.

Diplomatic rift between Qatar and other GCC states leading to severance of trade and economic ties is likely to have a negative impact on the insurance sector.

Trends

Growing consolidation: The GCC insurance sector has started showing signs of consolidation, with the trend gathering momentum particularly in Saudi Arabia and the UAE due to stringent reserving and solvency practices.

Rising consumer awareness: Regulators have collaborated with insurance companies to educate the consumers on protection against risks. Further, new risks such as cyber risk and political risk are emerging and hence the related insurance covers.

Improving investments in debt markets: The sector is witnessing an improving investment exposure to debt instruments. This is mainly due to increasing sovereign bond issuances and regulations imposing investment limits.

Rising potential of Bancassurance: Insurance sold through banks is increasing, as the banks seek new income sources amid low interest rates and slow credit offtake. Other than the UAE, the composition of Bancassurance is low in the other GCC insurance markets, but it has become an attractive as well as profitable business for banks and insurance providers

Technological advancement: Earlier the focus was on pricing and reducing distribution cost, however rising competition and use of smartphones have put customers at the center. In addition, the rapidly evolving and changing technologies are influencing the entire insurance value chain, right from product development to distribution.

Advent of Insurance aggregators: Insurance aggregators are entering the market to take advantage of the expanding premiums and digital consumer.

Financial Performance

We have analyzed the latest three-year financial performance of 19 listed insurance companies in the GCC based on the size of premiums and assets.

Consolidated GWP of the selected insurance companies in the GCC stood at US$ 13.1 billion in 2016, signifying a CAGR of 13.0% from 2014. Consolidated net underwriting profit of the selected insurance companies grew at a CAGR of 21.5% from US$ 1.1 billion in 2014 to US$ 1.6 billion in 2016[1]. The top three providers accounted for 67.6% of the underwriting results during the year. The average Return on Equity (ROE) of the select peers remained volatile during 2014 and 2016, with returns improving to 12.2% in 2016 after a fall in 2015 to 9.1%.

The GCC-based insurance companies are trading at an average P/E multiple of 12.0x and P/B multiple of 1.7x. At current multiples, other than the companies in Saudi Arabia that appear to be pricey, the insurance companies in other GCC countries look undervalued, in view of the underpenetrated insurance market coupled with the underwriting potential arising from revenue diversification efforts and changes in insurance regulations. These are reflective of a clear upside potential in valuations going forward.

-Ends-

If you would like to receive a copy of the GCC Insurance Industry report, please email your request to alpencapital.events@alpencapital.com .

For more information please contact:

Sameena Ahmad, Corporate Affairs

Telephone +971 (0)4 363 43 00

e-mail: sameena.ahmad@alpencapital.com

Alpen Capital (ME) Ltd – www.alpencapital.com

Alpen Capital (ME) Limited is incorporated as a limited liability company in the Dubai International Financial Centre, Dubai, United Arab Emirates and is licensed by the Dubai Financial Services Authority. With local know-how and regional expertise, Alpen Capital offers a full range of investment banking advisory services in the areas of M & A, Debt, Equity and Capital markets. Apart from Dubai, it has offices in Abu Dhabi, Doha, Muscat, Mumbai and New Delhi.

[1] Source: Thomson Reuters Eikon; National General Insurance Co. has been excluded, as the CAGR in underwriting profits is extraordinary at 194.4%

© Press Release 2017