PHOTO

Byblos Bank Headquarters, August 16, 2018: Byblos Bank issued today the results of the Byblos Bank Real Estate Demand Index for the second quarter of 2018.

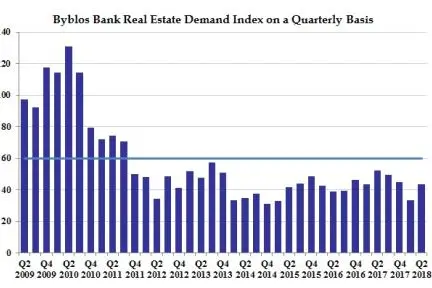

The results show that the Index posted a monthly average of 43.7 points in the second quarter of 2018, constituting an increase of 31.8% from 33.2 points in the first quarter of 2018 and a decrease of 16.3% from 52.3 points in the second quarter of 2017. The second-quarter results constitute their 14th lowest level in 44 quarterly readings.

Commenting on the results, Mr. Nassib Ghobril, Chief Economist and Head of the Economic Research and Analysis Department at the Byblos Bank Group, said: “the increase of the Index in the second quarter of the year was mainly due to the announcement in April by the ministries of Finance and Social Affairs that the government intends to allocate LBP 1,000 billion to subsidize interest rates on housing loans, which raised expectations that affordable mortgages for limited-income citizens will resume after their suspension at the beginning of the year.'' He added “another important, but understated, factor that contributed to the improvement of the Index is the fact that Banque du Liban and commercial banks processed pre-approved applications for subsidized housing loans that were pending during the first quarter of the year, which allayed the concerns of applicants at the time.”

However, Mr. Ghobril cautioned that ”the increase of the Index in the second quarter should not be viewed as a change in the dynamics of the housing market, as the improvement comes from a very low base following the first-quarter results that constituted the Index’s third lowest level in 44 quarterly readings.” Further, the Index’s average monthly score in the second quarter of 2018 came 67% lower from the peak of 131 points registered in the second quarter of 2010, and remained 60% below the annual peak of 109.8 points posted in 2010. Also, it was 27% lower than the Index's monthly trend average score of 60 points since the Index’s inception in July 2007.

The answers of respondents to the Index's survey questions in the second quarter of 2018 show that 4.9% of Lebanese residents had plans to either buy or build a residential property in the coming six months compared to 3.8% in the first quarter of the year and to 5.9% in the second quarter of 2017. In comparison, 6.8% of residents in Lebanon, on average, had plans to buy or build a residential unit in the country between July 2007 and June 2018, with this share peaking at nearly 15% in the second quarter of 2010.

Mr. Ghobril considered that ”Lebanese citizens need to see the authorities’ intentions to restore subsidies on mortgages translated into concrete measures, as any delay or uncertainty about this issue may dent the expectations of households and, in turn, further reduce demand for housing.'' He pointed out that ''the ongoing suspension of the subsidy program will continue to weigh on the willingness of prospective buyers to acquire a residential unit, given that buying a house constitutes one of the most important investment decisions for the Lebanese, and the value of a house is usually the single most important non-financial asset for Lebanese residents." He noted that ''it remains the responsibility of the executive branch to not only cover interest subsidies on housing loans for limited-income citizens, but also to take the lead in developing a comprehensive housing policy that stimulates demand for all segments of the residential housing market in Lebanon.''

The results of the Index show that demand for housing was the highest in the South in the second quarter of 2018, as 7.8% of its residents had plans to build or buy a house in the coming six months, compared to 3.4% in the first quarter of 2018. The Bekaa followed with 6% of its residents planning to build or buy a residential unit in the coming six months, up from 1.7% in the preceding quarter; while 4.6% of residents in Mount Lebanon had plans to buy or build a house, relative to 3.2% in the previous quarter. In addition, 4% of residents in the North intend to buy or build a house, down from 6% in the preceding quarter, while 3% of residents in Beirut had plans to build or buy a residential unit, down from 4.6% in the first quarter of 2018. In parallel, real estate demand increased among all income brackets in the second quarter of 2018.

The Byblos Bank Real Estate Demand Index is a measure of local demand for residential units and houses in Lebanon. The Index is compiled, implemented and analyzed in line with international best practices and according to criteria from leading indices worldwide. The Index is based on a face-to-face monthly survey of a nationally representative sample of 1,200 males and females living throughout Lebanon, who reflect the demographic, regional, religious, professional and income distribution of Lebanon. The surveyed persons are asked about their plans to buy or build a house in the coming six months. The Byblos Bank Economic Research and Analysis Department has been calculating the Index on a monthly basis since July 2007, with November 2009 as its base month. The survey has a margin of error of ±2.83%, a confidence level of 95% and a response distribution of 50%. The monthly field survey is conducted by Statistics Lebanon Ltd, a market research and opinion-polling firm.

-Ends-

For further information, please contact:

Nassib Ghobril

Chief Economist

Head of Group Economic Research & Analysis Department

Byblos Bank, Beirut, Lebanon

Phone: (961) 1 338 100 ext. 0205

Fax: (961) 1 217 774

E-mail: nghobril@byblosbank.com.lb

© Press Release 2018Disclaimer: The contents of this press release was provided from an external third party provider. This website is not responsible for, and does not control, such external content. This content is provided on an “as is” and “as available” basis and has not been edited in any way. Neither this website nor our affiliates guarantee the accuracy of or endorse the views or opinions expressed in this press release.

The press release is provided for informational purposes only. The content does not provide tax, legal or investment advice or opinion regarding the suitability, value or profitability of any particular security, portfolio or investment strategy. Neither this website nor our affiliates shall be liable for any errors or inaccuracies in the content, or for any actions taken by you in reliance thereon. You expressly agree that your use of the information within this article is at your sole risk.

To the fullest extent permitted by applicable law, this website, its parent company, its subsidiaries, its affiliates and the respective shareholders, directors, officers, employees, agents, advertisers, content providers and licensors will not be liable (jointly or severally) to you for any direct, indirect, consequential, special, incidental, punitive or exemplary damages, including without limitation, lost profits, lost savings and lost revenues, whether in negligence, tort, contract or any other theory of liability, even if the parties have been advised of the possibility or could have foreseen any such damages.