PHOTO

Global oil markets moved into deficit in early June, according to market fundamentals. While signs of a recovery in physical oil markets are emerging and supply is responding, experts say that the fallout from COVID-19 will be long-lasting.

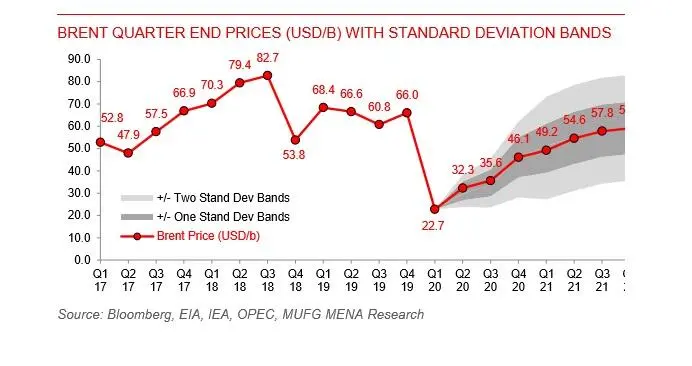

“As the world emerges from lockdowns, a combination of weaker economic growth and the lingering impacts of COVID-19 mobility restrictions will still be a drag on the recovery in oil demand, especially jet fuel. As such, we continue to forecast the damage persisting into next year, with oil demand only reaching a pre-COVID-19 run-rate by Q3 2021,” said Ehsan Khoman, Director and Head of MENA Research and Strategy, MUFG Bank.

The International Energy Agency (IEA) has voiced a similar view, stating that COVID-19 will flatten global growth and oil demand this year, but supply cuts from OPEC+ and a record rebound in demand next year will help rebalance the oil market.

While the world's demand for crude will drop by 8.1 million barrels a day this year, demand in 2021 will rebound by a record 5.7 million barrels a day, IEA said in its monthly oil-market report on Tuesday.

Around 2.8 billion people will be living under confinement measures aimed at containing the novel coronavirus at the end of May, down from 4 billion in April, the Paris-based IEA said.

Oil cartel OPEC has said that demand would fall by 6.4 million barrels per day (bpd) in the second half of 2020, less than the drop of 11.9 million bpd in the first six months of the year, with a "gradual recovery" seen until the end 2020.

On Monday, oil giant BP revised down its long-term investment appraisal price to an average of just $55 per barrel for Brent in real terms between 2021 and 2050. The company expects the coronavirus pandemic to have an enduring impact on the global economy with the potential for weaker demand for energy for a sustained period. It also cited the potential for an accelerated transition to a lower-carbon economy and energy system.

According to MUFG, the pulse in global oil markets is caught between two competing forces – cautious re-openings (and the Fed's credit support), versus apprehensions about the second wave of coronavirus attacks.

"On the one hand, the ongoing reopening of economies across the world, in conjunction with a very proactive Fed that continues to appease markets by ensuring that financing conditions stay loose for longer, has in effect put a floor in oil prices.

"Meanwhile, on the other hand, global oil markets are not discarding the further catch up in global risk, with respect to ongoing fractures in oil demand, as after weeks of diminishing focus on COVID-19 new infections in China, investors are beginning to scrutinise new infection numbers more materially," Khoman said in the note.

The energy agency has acknowledged the spur in the recovery in crude demand is mainly because coronavirus lockdowns are being lifted, and economies are returning to life at different paces worldwide.

However, "we should not underestimate the enormous uncertainties" the market still faces, IEA said, adding, "the biggest [uncertainty] is whether governments can ease the lockdown measures without sparking a resurgence of COVID-19 outbreaks. Another is whether a high level of compliance with the OPEC+ agreement will be achieved and maintained by all the major parties."

Given the lack of any medical breakthroughs (vaccine or treatments) for now, global risks will have to weather the concerns of second waves in the coming months, as many economies attempt further easing in their lockdown measures, MUFG said in its note. It cited the example of Bejing ordering all schools to close and elevating the city's emergency response one notch to level 2, the second-highest among four levels of disease response.

Oil prices fell more than one percent in early trade on Thursday as an increase in new coronavirus cases in China and the US renewed fears that people would stay home and stall recovery in fuel demand even as lockdowns ease, Reuters reported.

Brent crude futures fell 1.1 percent, or 45 cents, to $40.26 a barrel.

(Reporting by Seban Scaria; editing by Anoop Menon)

#COVID-19 #OIL #MUFG #IEA #OPEC

Disclaimer: This article is provided for informational purposes only. The content does not provide tax, legal or investment advice or opinion regarding the suitability, value or profitability of any particular security, portfolio or investment strategy. Read our full disclaimer policy here.

© ZAWYA 2020