11 August 2008

Investor sentiment towards the Egyptian banking sector remains pessimistic following the postponement of merger talks between two leading players, says a new report.

A delay in the sale of a majority stake in Banque du Caire and Moody's revision of the deposit rates outlook have contributed to the negative view. But the long-term earning prospects of the sector remain robust, says the review by Cairo-based investment bank Prime Holding.

Local and foreign investor sentiment towards the sector has remained lacklustre since the start of the year and the first-half results of some loss-making banks have been hit further by increased provisioning requirements for bad loans.

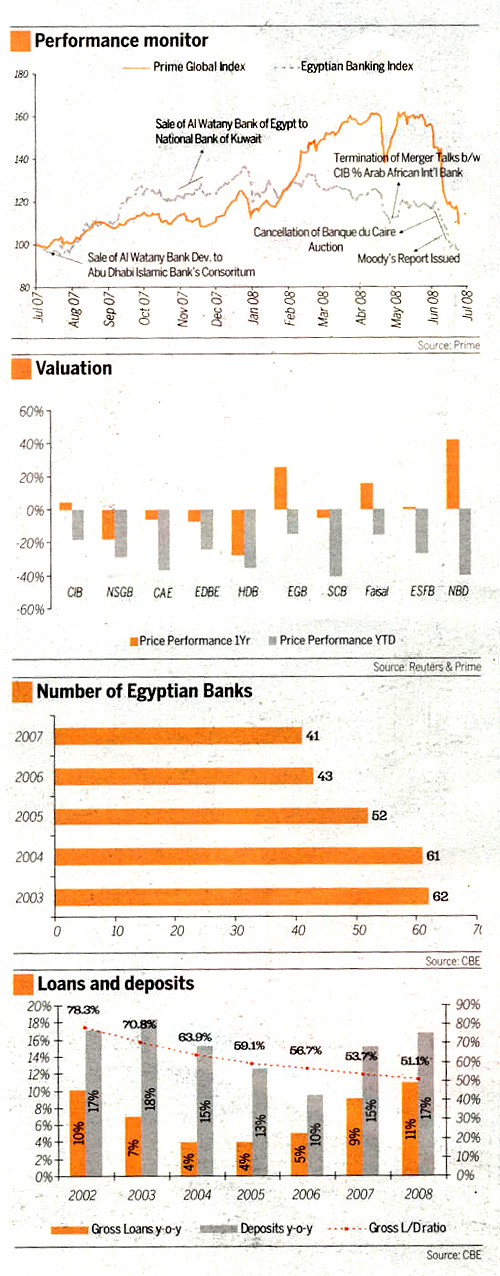

"Numerous domestic events have led to bearish performance of the banking stocks since the start of the year," says the report. "These include the cancellation of the merger talks between Commercial International Bank and Arab African International Bank, the postponement of a 67 per cent stake sale in Banque du Caire and a recently issued report by the Moody's rating agency revising the country's bank deposit ratings in view of the rising inflation and interest rate conditions."

However, the long-term earning prospects for the sector are good with the average return on aggregate assets (RoAA) of 10 leading banks expected to go up from 0.6 per cent in 2007 to 1.3 per cent in 2008.

The private sector banks such as the Commercial International Bank (CIB) and Export Development Bank (EDB) achieved a ratio well over two per cent. The number of Egyptian banks has fallen from 62 in 2003 to 41 in 2007 following government measures and consolidation in the sector.

"Local banks are currently well capitalised on their excess liquidity while maintaining better credit quality standards," the report adds.

The prospects for the growth of the Egyptian economy are robust and the real gross domestic product growth is expected to average 6.3 per cent over the forecast period of 2008 until 2012. This is slightly below the growth rate recorded in recent years as investment growth and export growth gradually slow, the report says. The inflation rate reached 19.7 per cent in May 2008 but will fall to an average of 9.7 per cent in 2009 from an average 17.1 per cent in 2008.

Inflation control measures of the Central Bank of Egypt (CBE) - including raising interest rates and the use of long-term instruments such as CBE deposits and treasuries to absorb surplus liquidity in the banking system - will bring down the figure.

Annual lending last year rose by nine per cent compared to five per cent in 2006. Lending to households is growing as a proportion of total loans, with the ratio reaching 19.2 per cent in May 2008 compared to 17.8 per cent a year ago. Many banks are shifting to the more lucrative but risky retail sector by expanding their branch networks.

The cost of funding within the banks is expected to increase modestly due to high inflation and interest rates. Credit quality is improving after the CBE forced many of the small banks - Export Development, Faisal Islamic, Suez Canal and Egyptian Saudi - to transfer their year-end profits to cover the shortage in their provision accounts.

Prime's analysts say banking sector valuations look attractive and banks such as Export Development Bank, Suez Canal Bank and Egyptian Saudi Finance Bank offer greater upside potential for investors in the small cap banking area. National Societe General Bank's (NSGB) offers maximum potential among the large-cap banks followed by Credit Agricole Egypt.

Reviewing the first-quarter performance and first-half expectations of Commercial International Bank (CIB), the report says the bank will post a net income figure of EGP769.6 million (Dh534.7m), a year-on-year growth of 16 per cent but quarter-to-quarter decline of 25 per cent.

Acquisition of the remaining 50 per cent stake in its subsidiary, CI-CH, is expected to boost the bank's future earnings. CIB reported a net income of EGP440.8m - 65 per cent year-on-year growth. Net banking income advanced by 58.7 per cent.

The bank's net income during the first quarter was boosted by provisions reversed worth EGP94.8m and a EGP50.3m gain from the sale of its stake in Contact Cars. The bank is expected to expand its retail banking using the excess liquidity. A one-for-two stock dividend distribution for shareholders will increase its capital from EGP1.95 billion to EGP2.93bn.

NSGB's net income is estimated to have increased by 14 per cent to EGP388.3m during first half 2008. The bank is expected to boost its net interest income by introducing retail banking. The report predicts an increase in fees and commissions income and expects the net loans to deposits ratio to settle at 54.2 per cent in the first half 2008, slightly higher than the 53.1 per cent achieved in the comparable period last year.

Credit Agricole Egypt had a net income of EGP107.75m in the first quarter of 2008 and is expected to report a net income of EGP225.7m, up 6.7 per cent year-on-year. However, the bank's net income growth is expected to be curtailed due to higher provision requirements for its growing loans portfolio. The report warns that the bank's regular loan provision reversal for the past five quarters is not sustainable in the coming quarter. The bank will face a slight increase in cost of funds compared to its large cap banking peers due to higher concentration of its deposit base in time and saving deposits.

The Export Development Bank, which reported low profits due to higher provision requirements by the CBE, is set to report a net profit after unusual items of EGP305.1m - 40.5 per cent up from EGP7.5m in 2007.

"Starting 2009, the bank is expected to utilise its recent capital increase proceeds worth EGP200m to expand its loan portfolio, in particular, lending activities to export-based small and medium enterprises," the report says. It adds the cost of funding will also come under pressure as the bank attracted a sizeable amount of time and saving deposits last year to overcome sluggish deposit trends.

The Housing and Development Bank, which reported EGP42m profit in the first quarter 2008 from EGP21.6m in the previous year period, is expected to improve its bottom line to EGP130.3m in the first half of 2008. Prime expects the bank's quality of revenue will improve due to high-income flow from sale of housing units and mortgage lending activities through its subsidiaries.

Egyptian Gulf Bank (EGB), which reported an increase in its net income figure by 36.5 per cent year-on-year to EGP43.1m, is expected to report five per cent growth to EGP68.8m in the first half of 2008 backed by higher provisioning. EGB is acquiring a 20 per cent stake in Prime.

Suez Canal Bank, which continued to report a zero net income figure in first quarter 2008 similar to the comparable period last year, is expected to book a zero bottom line for the first half. The report says the bank's net income growth was constrained by significant provisioning and it is expected to fully restructure its loan portfolio.

Faisal Islamic Bank too declared a zero net income during the first quarter and the first half too the net income will remain zero due to limited visibility concerning the bank's remaining shortage in the total provisioning account. The bank is expanding its paid up capital from EGP528.1m to EGP792.2m through a rights issuance process in an effort to support its financial position.

Egyptian Saudi Finance Bank (ESFB), which reported zero net income in first quarter compared to EGP20.9m in the comparable period last year, is expected to report 84 per cent decline in net profit to EGP6.7m. "In an effort to alleviate the credit quality problems of the bank it attained a loan worth $20m (Dh73.6m) from its parent bank to cover up a portion of the shortage in its provisioning account. The bank will reach 100 per cent coverage at most by year 2010 when it will distribute dividends to shareholders."

The National Bank for Development will report a net loss of EGP182m. The bank will undertake additional restructuring of its net loans portfolio. Gains of EGP140m from the sale of one of its subsidiaries will cushion the net income fall. The bank management continued to book significant loan provisions.

Investor sentiment towards the Egyptian banking sector remains pessimistic following the postponement of merger talks between two leading players, says a new report.

A delay in the sale of a majority stake in Banque du Caire and Moody's revision of the deposit rates outlook have contributed to the negative view. But the long-term earning prospects of the sector remain robust, says the review by Cairo-based investment bank Prime Holding.

Local and foreign investor sentiment towards the sector has remained lacklustre since the start of the year and the first-half results of some loss-making banks have been hit further by increased provisioning requirements for bad loans.

"Numerous domestic events have led to bearish performance of the banking stocks since the start of the year," says the report. "These include the cancellation of the merger talks between Commercial International Bank and Arab African International Bank, the postponement of a 67 per cent stake sale in Banque du Caire and a recently issued report by the Moody's rating agency revising the country's bank deposit ratings in view of the rising inflation and interest rate conditions."

However, the long-term earning prospects for the sector are good with the average return on aggregate assets (RoAA) of 10 leading banks expected to go up from 0.6 per cent in 2007 to 1.3 per cent in 2008.

The private sector banks such as the Commercial International Bank (CIB) and Export Development Bank (EDB) achieved a ratio well over two per cent. The number of Egyptian banks has fallen from 62 in 2003 to 41 in 2007 following government measures and consolidation in the sector.

"Local banks are currently well capitalised on their excess liquidity while maintaining better credit quality standards," the report adds.

The prospects for the growth of the Egyptian economy are robust and the real gross domestic product growth is expected to average 6.3 per cent over the forecast period of 2008 until 2012. This is slightly below the growth rate recorded in recent years as investment growth and export growth gradually slow, the report says. The inflation rate reached 19.7 per cent in May 2008 but will fall to an average of 9.7 per cent in 2009 from an average 17.1 per cent in 2008.

Inflation control measures of the Central Bank of Egypt (CBE) - including raising interest rates and the use of long-term instruments such as CBE deposits and treasuries to absorb surplus liquidity in the banking system - will bring down the figure.

Annual lending last year rose by nine per cent compared to five per cent in 2006. Lending to households is growing as a proportion of total loans, with the ratio reaching 19.2 per cent in May 2008 compared to 17.8 per cent a year ago. Many banks are shifting to the more lucrative but risky retail sector by expanding their branch networks.

The cost of funding within the banks is expected to increase modestly due to high inflation and interest rates. Credit quality is improving after the CBE forced many of the small banks - Export Development, Faisal Islamic, Suez Canal and Egyptian Saudi - to transfer their year-end profits to cover the shortage in their provision accounts.

Prime's analysts say banking sector valuations look attractive and banks such as Export Development Bank, Suez Canal Bank and Egyptian Saudi Finance Bank offer greater upside potential for investors in the small cap banking area. National Societe General Bank's (NSGB) offers maximum potential among the large-cap banks followed by Credit Agricole Egypt.

Reviewing the first-quarter performance and first-half expectations of Commercial International Bank (CIB), the report says the bank will post a net income figure of EGP769.6 million (Dh534.7m), a year-on-year growth of 16 per cent but quarter-to-quarter decline of 25 per cent.

Acquisition of the remaining 50 per cent stake in its subsidiary, CI-CH, is expected to boost the bank's future earnings. CIB reported a net income of EGP440.8m - 65 per cent year-on-year growth. Net banking income advanced by 58.7 per cent.

The bank's net income during the first quarter was boosted by provisions reversed worth EGP94.8m and a EGP50.3m gain from the sale of its stake in Contact Cars. The bank is expected to expand its retail banking using the excess liquidity. A one-for-two stock dividend distribution for shareholders will increase its capital from EGP1.95 billion to EGP2.93bn.

NSGB's net income is estimated to have increased by 14 per cent to EGP388.3m during first half 2008. The bank is expected to boost its net interest income by introducing retail banking. The report predicts an increase in fees and commissions income and expects the net loans to deposits ratio to settle at 54.2 per cent in the first half 2008, slightly higher than the 53.1 per cent achieved in the comparable period last year.

Credit Agricole Egypt had a net income of EGP107.75m in the first quarter of 2008 and is expected to report a net income of EGP225.7m, up 6.7 per cent year-on-year. However, the bank's net income growth is expected to be curtailed due to higher provision requirements for its growing loans portfolio. The report warns that the bank's regular loan provision reversal for the past five quarters is not sustainable in the coming quarter. The bank will face a slight increase in cost of funds compared to its large cap banking peers due to higher concentration of its deposit base in time and saving deposits.

The Export Development Bank, which reported low profits due to higher provision requirements by the CBE, is set to report a net profit after unusual items of EGP305.1m - 40.5 per cent up from EGP7.5m in 2007.

"Starting 2009, the bank is expected to utilise its recent capital increase proceeds worth EGP200m to expand its loan portfolio, in particular, lending activities to export-based small and medium enterprises," the report says. It adds the cost of funding will also come under pressure as the bank attracted a sizeable amount of time and saving deposits last year to overcome sluggish deposit trends.

The Housing and Development Bank, which reported EGP42m profit in the first quarter 2008 from EGP21.6m in the previous year period, is expected to improve its bottom line to EGP130.3m in the first half of 2008. Prime expects the bank's quality of revenue will improve due to high-income flow from sale of housing units and mortgage lending activities through its subsidiaries.

Egyptian Gulf Bank (EGB), which reported an increase in its net income figure by 36.5 per cent year-on-year to EGP43.1m, is expected to report five per cent growth to EGP68.8m in the first half of 2008 backed by higher provisioning. EGB is acquiring a 20 per cent stake in Prime.

Suez Canal Bank, which continued to report a zero net income figure in first quarter 2008 similar to the comparable period last year, is expected to book a zero bottom line for the first half. The report says the bank's net income growth was constrained by significant provisioning and it is expected to fully restructure its loan portfolio.

Faisal Islamic Bank too declared a zero net income during the first quarter and the first half too the net income will remain zero due to limited visibility concerning the bank's remaining shortage in the total provisioning account. The bank is expanding its paid up capital from EGP528.1m to EGP792.2m through a rights issuance process in an effort to support its financial position.

Egyptian Saudi Finance Bank (ESFB), which reported zero net income in first quarter compared to EGP20.9m in the comparable period last year, is expected to report 84 per cent decline in net profit to EGP6.7m. "In an effort to alleviate the credit quality problems of the bank it attained a loan worth $20m (Dh73.6m) from its parent bank to cover up a portion of the shortage in its provisioning account. The bank will reach 100 per cent coverage at most by year 2010 when it will distribute dividends to shareholders."

The National Bank for Development will report a net loss of EGP182m. The bank will undertake additional restructuring of its net loans portfolio. Gains of EGP140m from the sale of one of its subsidiaries will cushion the net income fall. The bank management continued to book significant loan provisions.

By VM Satish

Emirates Business 24/7 2008