(Geneva) - The International Air Transport Association (IATA) released data for global air freight markets in November showing that freight volumes improved compared to October, but remain depressed compared to 2019. Capacity remains constrained from the loss of available belly cargo space as passenger aircraft remain parked.

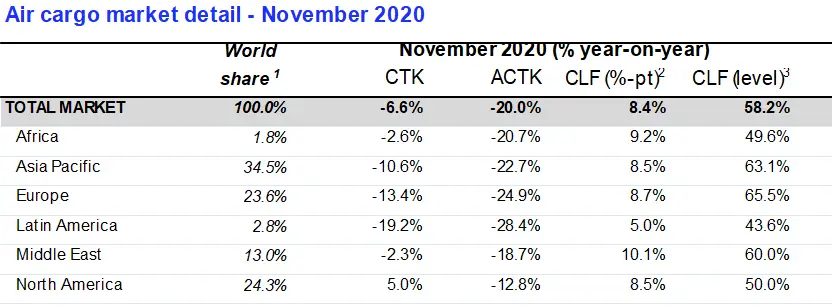

- Global demand, measured in cargo tonne-kilometers (CTKs*), was 6.6% below previous-year levels in November (-7.7% for international operations). This was on par with the 6.2 % year-on-year drop in October. The year-on-year decline is skewed as November 2019 had a boost in demand from the waning US-China trade war.

- Seasonally adjusted demand (SA CTKs) continued to improve, increasing 1.6% month-on-month in November. This was a slight improvement over the monthly growth rate of 1.1% in October. Current month-on-month gains indicate that SA CTKs will return to 2019 levels around March or April 2021.

- Global capacity, measured in available cargo tonne-kilometers (ACTKs), shrank by 20% in November (‑21.3% for international operations) compared to the previous year. That is nearly three times larger than the contraction in demand. The capacity crunch is caused by a 53% decrease in in belly capacity. This has only been partially offset by a 20% increase in freighter capacity.

- Strong regional variations continue with North American carriers reporting year-on-year gains in demand (+5%), while all other regions remained in negative territory compared to a year earlier.

- Economic conditions in November, normally the peak season for air cargo, remained positive:

- The new export orders component of the manufacturing Purchasing Managers’ Index (PMI) remained in growth territory in both developed and emerging markets for the third month in a row after two years of indicating negative growth.

- Retail sales for November were up by around 5% over 2019 for both China and the US, propelled by events like Black Friday and Singles Day.

“Air cargo demand is still down 6.6% compared to the previous year, however we are seeing continuing month-on-month improvements. Severe capacity constraints persist as large parts of the passenger fleet remain grounded. This will put pressure on the industry as it gears up to deliver vital COVID-19 vaccines,” said Alexandre de Juniac, IATA's Director General and CEO.

November’s Regional Performance

Asia-Pacific airlines reported a decline in year-on-year international demand of 9.5% in November 2020 compared to the same month a year earlier. This was a 2.2% improvement from the 11.7% fall in October 2020. While international traffic within the region remains weak (down 19.6% year-on-year in November), exports on the Asia-North America and Asia-Europe routes are strong, driven by demand for e-commerce and PPE. International capacity remained constrained in the region, down 25.3%. However, this was an improvement over the 28.5% fall the previous month.

North American carriers posted a 1% increase in international demand in November compared to the previous year—just the third month of growth in 12 months. This stronger performance compared to the rest of the industry was driven by a less stringent capacity crunch compared to other regions, with international capacity only down 12.7% in November. Strong traffic on the Asia-North America routes also contributed to the performance, reflecting rising e-commerce demand for products manufactured in Asia.

European carriers reported a decrease in international demand of 13.7% in November compared to the previous year. This was a 2.7% decline in performance compared to October 2020. Air cargo in the region has been significantly affected by the resurgence of the COVID-19 virus and the impact of lockdowns on consumer demand and business activity. Lack of capacity remains a challenge, as international capacity decreased 24.9% in November.

Middle Eastern carriers reported a decline of 2.2% in year-on-year international cargo volumes in November, a 1.1% deterioration from October. The lack of international connectivity is hampering air cargo recovery in the region, however seasonally adjusted demand remains on an upward trend. International capacity decreased by 18.6%.

Latin American carriers reported a decline of 19.4% in international cargo volumes in November compared to the previous year. This was a drop from the 12.2% fall in October 2020. Air cargo in the region has been significantly affected by the resurgence of the COVID-19 virus and the impact of lockdowns on consumer demand and business activity. International capacity decreased 24.8% in November, an improvement from the 28.9% fall in October.

African airlines saw international demand fall by 1.7% year-on-year in November, after three months of positive year-on-year growth. This is primarily driven by a soft performance on the Asia-Africa route, which was down 4.5% year-on-year. International capacity decreased by 19.4%.

View the November Air Cargo Market Analysis (pdf)

-Ends-

For more information, please contact:

Four Communications

Email: iata@fourcommunications.com

- Please note that as of January 2020 onwards, we have clarified the terminology of the Industry and Regional series from ‘Freight’ to ‘Cargo’, the corresponding metrics being FTK (changed to ‘CTK’), AFTK (changed to ‘ACTK’), and FLF (changed to ‘CLF’), in order to reflect that the series have been consisting of Cargo (Freight plus Mail) rather than Freight only. The data series themselves have not been changed.

- IATA (International Air Transport Association) represents some 290 airlines comprising 82% of global air traffic.

- You can follow us at twitter.com/iata for announcements, policy positions, and other useful industry information.

- Explanation of measurement terms:

- CTK: cargo tonne-kilometers measures actual cargo traffic

- ACTK: available cargo tonne-kilometers measures available total cargo capacity

- CLF: cargo load factor is % of ACTKs used

- IATA statistics cover international and domestic scheduled air cargo for IATA member and non-member airlines.

- Total cargo traffic market shares by region of carriers in terms of CTK are: Asia-Pacific 34.5%, Europe 23.6%, North America 24.3%, Middle East 13.0%, Latin America 2.8%, and Africa 1.8%.

© Press Release 2021

Disclaimer: The contents of this press release was provided from an external third party provider. This website is not responsible for, and does not control, such external content. This content is provided on an “as is” and “as available” basis and has not been edited in any way. Neither this website nor our affiliates guarantee the accuracy of or endorse the views or opinions expressed in this press release.

The press release is provided for informational purposes only. The content does not provide tax, legal or investment advice or opinion regarding the suitability, value or profitability of any particular security, portfolio or investment strategy. Neither this website nor our affiliates shall be liable for any errors or inaccuracies in the content, or for any actions taken by you in reliance thereon. You expressly agree that your use of the information within this article is at your sole risk.

To the fullest extent permitted by applicable law, this website, its parent company, its subsidiaries, its affiliates and the respective shareholders, directors, officers, employees, agents, advertisers, content providers and licensors will not be liable (jointly or severally) to you for any direct, indirect, consequential, special, incidental, punitive or exemplary damages, including without limitation, lost profits, lost savings and lost revenues, whether in negligence, tort, contract or any other theory of liability, even if the parties have been advised of the possibility or could have foreseen any such damages.