PHOTO

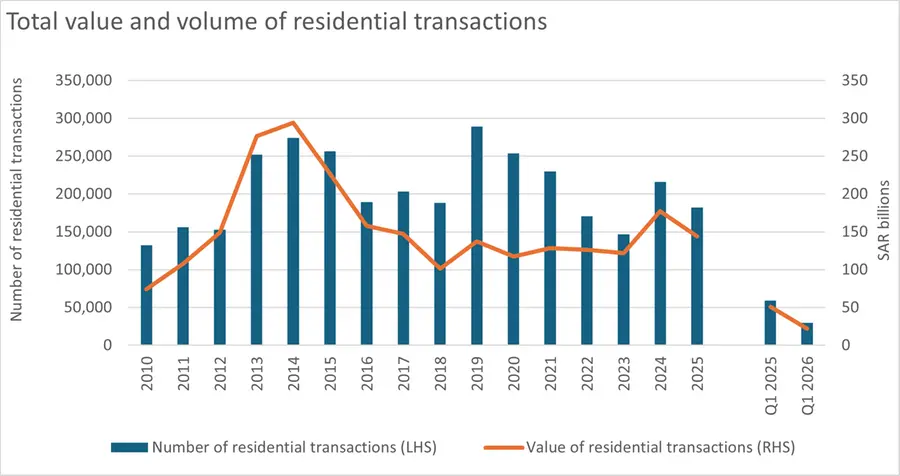

- Residential transaction values declined 57% to SAR 22 billion over the last 12 months

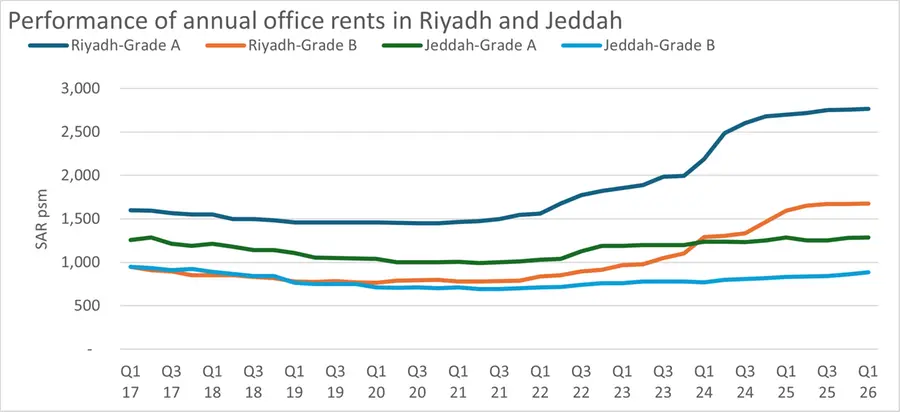

- Riyadh Grade A office rents increased 6.3% year-on-year, with occupancy remaining at 95%

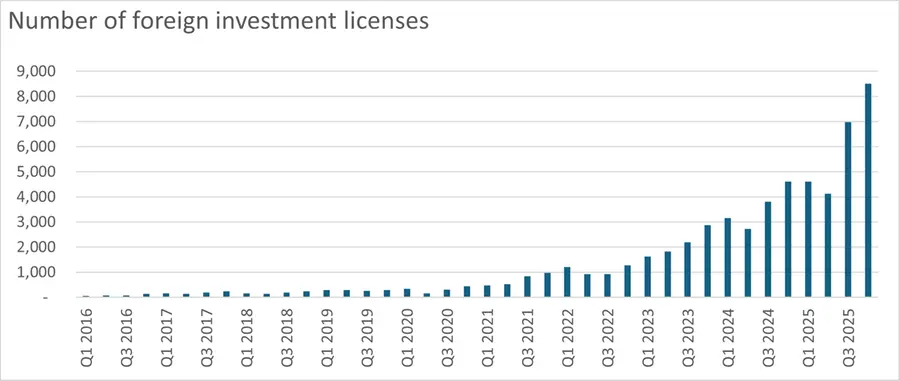

- Foreign investment licences rose almost 20% year-on-year as regional HQ commitments surpass 700

Riyadh: Saudi Arabia's residential market recorded a sharp slowdown in activity during Q1 2026, with transaction volumes falling by 50% year-on-year to 29,493 deals and transaction values declining by 57% to SAR 22 billion, according to global property consultancy, Knight Frank’s latest analysis.

The slowdown was most pronounced in Riyadh, where transaction volumes and values declined by 82% year-on-year during the first quarter. Jeddah, the Dammam Metropolitan Area (DMA), Makkah and Madinah also recorded weaker activity, reflecting growing affordability pressures, softer mortgage demand and while negative sentiment stemming from the regional conflict also dampened demand.

Faisal Durrani, Partner - Head of Research, MENA, said: "Predictably, the regional conflict has added to the weight of factors contributing to the slowing in residential sales activity that was evident well before the regional conflict began. The moderation in residential transaction activity reflects the well-entrenched affordability pressures, particularly in Riyadh, rather than a weakening of underlying demand. Indeed, our forecasts show a need for over 830,000 homes across the Kingdom by 2030 for the growing Saudi population alone. The challenge today is building housing at the right price points.

“Separately, the regional conflict has very likely heightened nervousness amongst prospective buyers who are unwilling to make what is likely to be their largest financial commitment during a time of elevated regional geopolitical uncertainty. For some households, the prospect of getting a ‘better deal’ should prices retreat as a result of the conflict is also another important consideration."

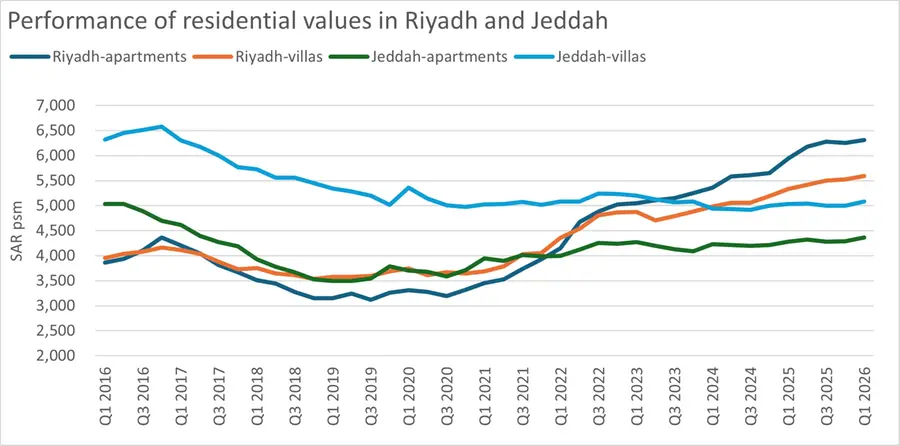

Despite weaker transaction activity, residential values continued to rise across most major markets. Apartment values in Riyadh increased by 6.3% year-on-year during Q1 2026, while villa values rose by 4.9%. Apartment values in Jeddah and the DMA increased by 2% and 2.3%, respectively. These price increases, Knight Frank says, are reflective of the resilience of pricing during the peace-time months of January and February, with the full impact of the conflict yet to crystalise in overall deal activity data.

Nonetheless, the slowdown in residential transactions coincided with weaker mortgage activity. New residential mortgage contracts declined by 25% year-on-year during the first four months of 2026, while the total value of mortgage lending fell by 34%.

Government housing initiatives continue to support long-term market fundamentals. Homeownership has increased from 47% in 2016 to more than 66% in 2025, while initiatives such as Sakani, Tawazon and the National Housing Company's large-scale residential developments continue to expand housing accessibility and supply across the Kingdom.

Durrani added, “The launch of the Tawazon platform has generated significant demand for planned and serviced residential land plots in Riyadh, with prices capped at SAR 1,500 psm. The initiative has been specifically designed to address housing affordability challenges by expanding access to lower-cost land, providing Saudi households with an alternative route to homeownership and supporting the government's broader objective of increasing housing accessibility across the capital”.

The National Housing Company remains a key driver of residential supply growth through the delivery of large-scale master-planned communities across the Kingdom. Residential stock in Riyadh is forecast to increase from approximately 2.7 million units in 2025 to more than 3.3 million units by 2030, while housing stock in Jeddah is expected to reach 1.47 million units and supply in the DMA is forecast to approach one million units over the same period.

Saudi Arabia's evolving regulatory framework is also expected to support long-term market growth. The updated Law of Real Estate Ownership by Non-Saudis, which comes into effect in 22 February 2026, represents one of the most significant openings of the Kingdom's real estate market to international capital. The reforms are expected to strengthen investor confidence, improve market transparency and support long-term demand across both residential and commercial real estate sectors.

Susan Amawi, General Manager - KSA, said: "Saudi Arabia's real estate market continues to benefit from one of the world's most ambitious economic and regulatory reform programmes. The introduction of the updated international non-resident ownership framework, combined with measures aimed at enhancing affordability and market stability, demonstrates the government's commitment to creating a more transparent, accessible and internationally competitive real estate sector. These reforms are expected to strengthen investor confidence and support long-term capital inflows across both residential and commercial real estate.

“The government's recently announced five-year freeze on residential and commercial rental increases within Riyadh is also expected to influence market dynamics. The measures are designed to encourage development, improve affordability, support residents and businesses facing rising occupancy costs”.

RHQ programme and foreign investment continue to support office demand

Elsewhere, Saudi Arabia's office market continued to demonstrate strong fundamentals during Q1 2026, particularly in Riyadh, where Grade A office rents increased by 2.5% year-on-year to SAR 2,770 psm. Occupancy levels remained high at 97%, reflecting sustained occupier demand and the ongoing shortage of institutional-grade office space in the capital.

Harmen De Jong, Regional Partner and Head of Consultancy, MENA, explained: "Demand continues to be driven by multinational corporations establishing their regional headquarters in the Kingdom, alongside expanding requirements from professional services firms, technology companies and other private sector occupiers. While leasing activity remains healthy, occupiers are becoming more selective, with requirements generally smaller in size and transactions taking longer to complete. In many cases, leasing decisions are being led directly by business owners and senior decision-makers rather than dedicated corporate real estate teams, resulting in a less structured and more considered leasing process.

Nevertheless, the office sector continues to benefit from the success of the Regional HQ Programme, which has attracted over 700 multinational companies to establish regional headquarters in the Kingdom, significantly exceeding the original Vision 2030 target of 500 companies."

Foreign investment activity also continued to strengthen. The number of foreign investment licences increased from 4,615 in Q1 2025 to 5,516 in Q1 2026, reinforcing Saudi Arabia's position as one of the region's most attractive destinations for international businesses and investors. Knight Frank believes the appetite from global businesses to expand across the region may be subdued while uncertainty surrounding the conclusion of regional hostilities remains unresolved, which may impact Q2 data once released by the authorities.

While office demand remains robust, the market is gradually entering a new phase as significant volumes of new office supply are planned for delivery. Riyadh's office stock is forecast to increase from approximately 6 million sqm in 2025 to more than 10.6 million sqm by 2032, helping to improve occupier choice and support the Kingdom's long-term economic growth ambitions. However, experience suggests that not all announced office developments are delivered within their original timelines.

The regional conflict has added further uncertainty, contributing to higher construction costs, which are up by an average of over 20% since the start of the year, says Knight Frank. In addition, rising freight and fuel prices, and supply chain disruptions linked to shipping constraints across key regional trade routes are likely to further push out completion timelines, potentially slowing the pace at which new supply enters the market and extending the current shortage of high-quality office accommodation in Riyadh.

Amar Hussain, Associate Partner - Research, MENA, said: "Occupier demand remains exceptionally strong, supported by the Regional HQ Programme, rising international investment activity and continued economic diversification. While new office supply will gradually improve occupier choice, demand for high-quality office accommodation remains robust, albeit larger requirements have been paused by occupiers due to the uncertainty driven by ongoing events. Separately, Riyadh Metro is also emerging as an increasingly important factor in occupier decision-making, enhancing connectivity between key business districts and supporting the growth of new commercial hubs across the capital."

Notes

Source: Knight Frank, MOJ

Source: Knight Frank, MOJ

Source: Knight Frank, Ministry of Investment

Source: Knight Frank

About Knight Frank

Knight Frank LLP is the leading independent global property consultancy. Headquartered in London, the Knight Frank network has 740+ offices across 50+ territories and more than 27,000 people. We advise clients ranging from individual owners and buyers to major developers, investors, and corporate tenants. For further information about the firm, please visit www.knightfrank.com.

In the MENA region, we have strategically positioned offices in key countries such as the United Arab Emirates, Saudi Arabia, Bahrain, Qatar and Egypt. For the past 16 years, we have been offering integrated residential and commercial real estate services, including transactional support, consultancy and management.

Understanding the unique intricacies of local markets is at the core of what we do, we blend this understanding with our global resources to provide you with tailored solutions that meet your specific needs. At Knight Frank, excellence, innovation and a genuine focus on our clients drive everything we do. We are not just consultants; we are trusted partners in property ready to support you on your real estate journey, no matter the scale of your endeavour.

https://www.knightfrank.com.sa/en