PHOTO

Dubai – Mashreq, one of the leading financial institutions in the MENA region, has delivered exceptional results for the full year 2025, marked by transformational international expansion, record loan and deposit growth, and a strategic repositioning as the connector bank for emerging trade corridors spanning Asia, the Middle East, Europe and North America.

Key Highlights:

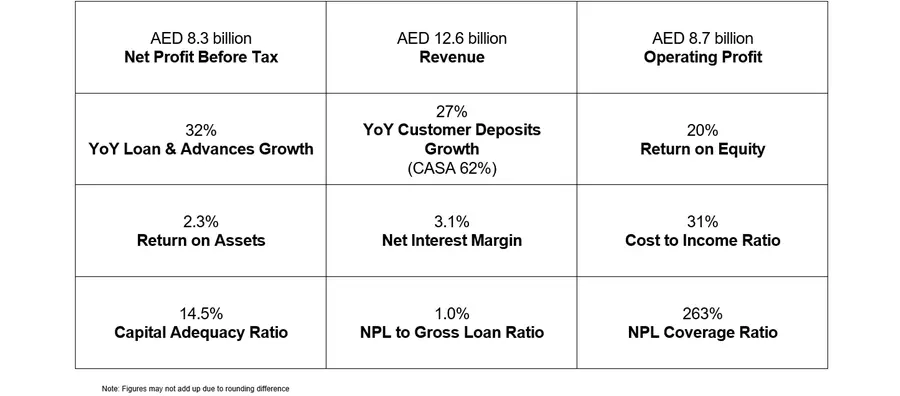

Operating income reached AED 12.6 billion, while net profit before tax totaled AED 8.3 billion, reflecting resilient performance and disciplined execution in a softer rate and higher-tax environment.

Performance in 2025 was driven by strong balance-sheet expansion, with customer loans growing 32% year-on-year, customer deposits increasing 27%, and total assets rising 25% to AED 335 billion, as Mashreq scaled its digital-first operating model and captured increased trade and capital flows across key global corridors.

Mashreq maintained strong efficiency, with a cost-to-income ratio of 31%, supported by a structurally strong funding profile underpinned by a CASA ratio of 62%. Asset quality remained industry-leading, with a non-performing loan ratio of 1.0% and a coverage ratio of 263%, underpinned by strong portfolio performance and sustained credit discipline across geographies.

The year also marked a milestone in Mashreq’s institutional standing, with its designation as a Domestic Systemically Important Bank (D-SIB) by the Central Bank of the UAE, reflecting the Bank’s scale, systemic relevance and robust risk governance as it continues to expand its global footprint.

Revenues and Income Generation

Strong operating income reflecting the scalability of Mashreq’s diversified, globally connected franchise, underpinned by strong balance-sheet growth and expanding trade and transaction flows.

- Operating income reached AED 12.6 billion in 2025, up 3% year-on-year on an adjusted basis excluding the one-off gain resulting from the IDFAA partial divestment in 2024, supported by higher origination volumes and stronger income contribution across Mashreq’s franchises.

- Net interest margin (NIM) remained resilient at 3.1% for the full year, despite cumulative policy rate cuts of 175 basis points since H2 2024, supported by disciplined repricing and a stable low-cost funding base, with Current Account Savings Account (CASA) at 62%.

- Non-interest income increased 16% year-on-year (excluding one off gain from partial divestment of IDFAA), driven by a 53% increase in investment income and a 30% increase in other income (excluding one-offs), reflecting higher transaction intensity and reinforcing the shift toward a more balanced and fee-accretive earnings mix.

- Cross-sell ratio rose to 35%, up approximately 400 basis points year-on-year (excluding one-offs), demonstrating a step-up in multi-product adoption across core client relationships and reinforcing the durability and diversification of the income mix.

Expenses and Efficiency

Mashreq delivered a strong and resilient efficiency outcome in 2025, maintaining a healthy cost profile while executing international expansion and accelerating investment in digital and AI capabilities.

- Operating expenses increased by 5% year-on-year, reflecting targeted investments in digital platforms, AI capabilities and international build-out, while maintaining disciplined cost management amid materially higher business volumes.

- Cost-to-income ratio stood at 31%, remaining healthy and competitive in a year marked by elevated investment activity and geographic expansion, underscoring the scalability of Mashreq’s operating model.

- Significant investment during the year focused on AI deployment, digital onboarding, credit decisioning and transaction processing capabilities, enhancing straight-through processing, reducing manual intervention and strengthening operational resilience across retail, SME and wholesale businesses.

Earnings and Profitability

Strong profitability and superior returns delivered in a year marked by record balance-sheet growth, disciplined execution and a structurally higher tax environment.

- Net profit before tax reached AED 8.3 billion in 2025, with net profit after tax of AED 7.0 billion, reflecting the Bank’s ability to translate scale, diversification and operating discipline into strong earnings despite the introduction of corporate income taxation.

- Return on equity remained strong at 20%, with return on assets at 2.3%, underscoring Mashreq’s ability to generate high-quality returns through disciplined capital deployment, stable margins and a diversified income base.

- Impairment charges remained low at AED 444 million, equivalent to a cost of credit of 27 basis points, demonstrating strong portfolio performance and credit discipline across geographies despite rapid loan growth.

- Tax expense increased to AED 1.3 billion in 2025 from AED 869 million in 2024, with the effective tax rate rising to 15.63% from 8.79%, primarily reflecting the introduction of the UAE Domestic Minimum Top-Up Tax (DMTT) and the application of Pillar Two rules; notwithstanding this structural step-up, profitability and returns remained firmly strong.

Asset Quality and Risk Management

Industry-leading asset quality sustained through a year of exceptional balance-sheet expansion, underpinned by strong portfolio performance and disciplined credit execution across geographies.

- Mashreq delivered the lowest non-performing loan ratio in the sector at 1.0% as at 31 December 2025, improving from 1.4% a year earlier, despite 32% year-on-year growth in customer loans.

- Coverage ratio strengthened to a robust 263%, providing a substantial buffer against potential downside risk and reinforcing balance-sheet resilience as activity levels and transaction volumes expanded.

- Strong asset quality outcomes were supported by disciplined credit selection, portfolio steering and sustained credit discipline across geographies, enabling Mashreq to scale lending activity while preserving best-in-class credit metrics.

Balance Sheet Strength

Balance-sheet momentum accelerated in 2025, driven by strong client demand, disciplined balance-sheet deployment and continued expansion across Mashreq’s core franchises

- Total assets increased 25% year-on-year to AED 335 billion as at 31 December 2025, reflecting broad-based balance-sheet growth across the UAE franchise and selective expansion aligned with client activity.

- Total lending across customers and banks grew 30% year-on-year to AED 230 billion, supported by strong origination across wholesale, retail and financial institution portfolios and higher transaction and financing volumes.

- Customer deposits rose 27% year-on-year to AED 205 billion, underpinned by continued growth in granular retail and corporate balances, with a CASA ratio of 62% providing a stable, low-cost funding base.

Capital and Liquidity Position

Strategic capital and liquidity management in 2025 reinforced Mashreq’s ability to fund growth, absorb volatility and support expanding client activity across markets.

- Liquidity metrics remained comfortably above regulatory requirements, with a liquid assets ratio of 28%, loan-to-deposit ratio of 80% and liquidity coverage ratio of 158%, supporting elevated lending and transaction activity.

- Funding resilience was further strengthened through two highly successful and oversubscribed transactions in 2025: a USD 2 billion syndicated loan facility and a debut USD 500 million Sukuk issuance, underscoring strong investor demand and confidence in Mashreq’s credit profile.

- Capitalisation remained among the strongest in the sector, with a capital adequacy ratio of 14.5%, Tier 1 ratio of 13.4% and CET1 ratio of 12.3%, supported by solid internal capital generation and best-in-class asset quality.

H.E. Abdul Aziz Al Ghurair, Chairman, Mashreq

“As we reflect on 2025, Mashreq’s progress is defined by resilience, disciplined growth, and a clear commitment to our purpose as a trusted enabler of financial advancement across borders. In a year that tested global markets and accelerated the shift toward a digital-first economy, Mashreq delivered a strong performance, achieving a net profit before tax of AED 8.3 billion.

This outcome reflects the strength of our strategy, the trust of our clients, and the enduring relevance of our role in the UAE’s evolving financial landscape. Being recognised as a Domestic Systemically Important Bank by the Central Bank of the UAE is not only an honor but also a responsibility, one that underscores our position as a foundational pillar in the country’s continued rise as a regional and global financial hub.

Looking ahead, we remain focused on advancing innovation, expanding our international reach, and embedding sustainability into our long-term agenda. With a strong foundation and a forward-looking vision, Mashreq will continue to empower clients, communities, and economies through inclusive, human-centric and technology-enabled banking.”

Ahmed Abdelaal, Group Chief Executive Officer, Mashreq

“2025 marked another pivotal year in Mashreq’s journey as a digitally advanced, globally connected bank serving clients across some of the world’s most dynamic trade and investment corridors. In a year of continued transformation and growth, we delivered operating income of AED 12.6 billion, expanded our total assets by 25% to AED 335 billion, and achieved a return on equity of 20%, all while maintaining a cost-to-income ratio of 31%, among the best in the industry.

This performance reflects our ability to scale strategically, remain agile in a changing economic environment, and deliver value through a diversified business model. Our expansion across strategic markets such as Türkiye, India, Egypt, and the US, the launch of our fully digital bank in Pakistan, and the continued development of Mashreq NEO platforms have enabled us to serve clients across retail, SME, and institutional segments with speed, intelligence and consistency.

As the only US dollar clearing bank based in the region, we have strengthened our role as a critical hub for cross-border trade, capital markets, and settlement infrastructure. Our wholesale banking and capital markets franchises continued to grow, and we were proud to support regional clients in accessing global investors and liquidity through innovative financing solutions.

Digital transformation remains central to our operating model. In 2025, we accelerated the deployment of AI tools across lending, onboarding, credit decisioning, and fraud prevention. Our in-house digital studios played a vital role in building scalable platforms and journeys that deliver real-time experiences while ensuring operational resilience and regulatory compliance.

We also deepened our focus on sustainability. By year-end, we facilitated significant volumes of sustainable finance, expanded our range of green retail offerings, and advanced our environmental commitments through high-efficiency operations and certified buildings across key markets.

Above all, it is our people who drive this transformation. We continued to invest in leadership development, inclusion, and nationalization, while supporting flexible work models and continuous learning through platforms such as WERise and WELearn. Across the organisation, our colleagues have shown exceptional commitment to our shared purpose.

Looking to the future, we will continue to deliver responsible growth, deepen our international footprint, and lead with technology and purpose. Our ambition remains to shape the future of banking by empowering clients, communities, and our people to thrive in an increasingly connected world. With resilience and purpose, we are well-positioned to navigate the opportunities and complexities of the year ahead.”

Year-End 2025 Financial Highlights

| Income Statement Highlights (AED mn) | 12M’25 | 12M’24 | ΔYoY% | 12M’24 (1) | ΔYoY%(1) | 4Q’25 | 3Q’25 | 4Q’24 | ΔQoQ% | ΔYoY% | 4Q’24(1) | ΔYoY%(1) | |

| Net Interest Income & Income from Islamic Financing | 8,141 | 8,388 | (3%) | 8,388 | (3%) | 2,061 | 2,119 | 2,054 | (3%) | 0% | 2,054 | 0% | |

| Fees & Commission | 1,333 | 1,465 | (9%) | 1,465 | (9%) | 301 | 388 | 301 | (22%) | 0% | 301 | 0% | |

| Investment Income | 350 | 229 | 53% | 229 | 53% | 39 | 99 | 21 | (60%) | 89% | 21 | 89% | |

| Insurance, FX & Other Income | 2,752 | 3,335 | (17%) | 2,124 | 30% | 785 | 597 | 1,941 | 32% | (60%) | 730 | 8% | |

| Non-Interest Income | 4,435 | 5,028 | (12%) | 3,817 | 16% | 1,126 | 1,083 | 2,263 | 4% | (50%) | 1,052 | 7% | |

| Total Operating Income | 12,576 | 13,416 | (6%) | 12,205 | 3% | 3,187 | 3,202 | 4,317 | 0% | (26%) | 3,106 | 3% | |

| Operating Expenses | (3,871) | (3,696) | 5% | (3,696) | 5% | (990) | (1,015) | (1,155) | (3%) | (14%) | (1,155) | (14%) | |

| Operating Profit | 8,705 | 9,720 | (10%) | 8,509 | 2% | 2,197 | 2,187 | 3,162 | 0% | (31%) | 1,951 | 13% | |

| Impairment Allowance | (444) | 166 | (367%) | 166 | (367%) | (78) | (121) | 239 | (35%) | (133%) | 239 | (133%) | |

| Net Profit Before Tax | 8,261 | 9,886 | (16%) | 8,675 | (5%) | 2,119 | 2,066 | 3,402 | 3% | (38%) | 2,191 | (3%) | |

| Tax | (1,291) | (869) | 49% | (869) | 49% | (329) | (357) | (225) | (8%) | 46% | (225) | 46% | |

| Net Profit after Tax | 6,970 | 9,017 | (23%) | 7,806 | (11%) | 1,790 | 1,708 | 3,177 | 5% | (44%) | 1,966 | (9%) | |

| Non-Controlling Interest | (131) | (100) | 30% | (100) | 30% | (39) | (23) | (34) | 66% | 16% | (34) | 16% | |

| Profit attributable to Owners of the Parent | 6,840 | 8,917 | (23%) | 7,706 | (11%) | 1,751 | 1,685 | 3,143 | 4% | (44%) | 1,932 | (9%) | |

| EPS (AED) | 33.0 | 43.7 | (24%) | 37.6 | (12%) | 8.4 | 8.2 | 15.4 | 4% | (45%) | 9.3 | (10%) | |

| Key Metrics (%) | 12M’25 | 12M’24 | Δbps YoY | 12M’24(1) | Δbps YoY (1) | 4Q’25 | 3Q’25 | 4Q’24 | Δbps QoQ | Δbps YoY | 4Q’24(1) | Δbps YoY(1) | |

| Cost to Income Ratio | 31% | 28% | 323 | 30% | 50 | 31% | 32% | 27% | (66) | 431 | 37% | (612) | |

| Return on Assets | 2.3% | 3.5% | (125) | 3.0% | (75) | 2.3% | 2.4% | 5.0% | (3) | (261) | 3.0% | (66) | |

| Return on Equity | 20% | 29% | (943) | 25.0% | (542) | 20% | 20% | 41% | 18 | (2,086) | 24.8% | (482) |

- Adjusted for one-off gain of AED 1,211mn from strategic partial sale of IDFAA

- Net Interest Income impacted by 175bps rate since H2 2024, with 50bps rate cut in 4Q’25 alone resulting in 3% year-on-year decline; partially offset by double-digit loan and investments growth with NIM of 3.1% in 2025.

- Non-Interest Income rose 16%(1) year-on-year in 2025 to AED 4.4 billion driven by 53% year-on-year growth in investment income and 30% (1) year-on-year growth in other income; overall contributing 35% of Total Operating Income.

- Continued double-digit expansion in loans and advances and non-interest income resulted in 3% year-on-year increase in Total Operating Income (excluding one-off) to AED 12.6 billion in 2025.

- We continued to invest significantly in digital platforms, Gen-AI-led initiatives and strategic business expansion, Operating expenses grew by just 5% year-on-year, reflecting cost discipline and the first effects of efficiency gains resulting from increase scalability due to digitalisation.

- With double-digit growth in loans and investments, Impairment allowances remained low at AED 444 million in 2025 (cost of credit of 27bps), driven by strong asset quality, quality underwriting and a benign macroeconomic environment in the key UAE market.

- Income tax expense of AED 1.3 billion in 2025, up by 49% year-on-year, impacted the net profit after tax, which saw a decline of 23% to reach AED 7.0 billion (decline of 11% year-on-year, excluding one-off), with a strong ROE of 20%.

| Balance Sheet Highlights (AED mn) | Dec’25 | Dec’24 | ΔYoY% | Dec’25 | Sep'25 | Dec’24 | ΔQoQ% | ΔYoY% |

| Loan to Customers | 164,349 | 124,758 | 32% | 164,349 | 143,085 | 124,758 | 15% | 32% |

| Loans to Banks | 65,721 | 52,272 | 26% | 65,721 | 65,380 | 52,272 | 1% | 26% |

| Investments | 50,624 | 36,422 | 39% | 50,624 | 47,789 | 36,422 | 6% | 39% |

| Cash & Due from Central Bank | 33,532 | 40,593 | (17%) | 33,532 | 31,402 | 40,593 | 7% | (17%) |

| Other Assets | 20,224 | 13,258 | 53% | 20,224 | 17,658 | 13,258 | 15% | 53% |

| Investments in Properties | 184 | 152 | 21% | 184 | 150 | 152 | 23% | 21% |

| Total Assets | 334,634 | 267,453 | 25% | 334,634 | 305,464 | 267,453 | 10% | 25% |

| Customer Deposits | 204,895 | 160,940 | 27% | 204,895 | 187,167 | 160,940 | 9% | 27% |

| Balances due to banks | 38,922 | 43,374 | (10%) | 38,922 | 41,123 | 43,374 | (5%) | (10%) |

| Loans and Sukuk | 15,310 | 3,903 | 292% | 15,310 | 6,267 | 3,903 | 144% | 292% |

| Other Liabilities | 27,793 | 19,381 | 43% | 27,793 | 26,438 | 19,381 | 5% | 43% |

| Repo | 7,136 | 2,076 | 244% | 7,136 | 5,546 | 2,076 | 29% | 244% |

| Minority Interest | 1,202 | 1,067 | 13% | 1,202 | 1,153 | 1,067 | 4% | 13% |

| Total Equity | 39,374 | 36,713 | 7% | 39,374 | 37,771 | 36,713 | 4% | 7% |

| Total Equity & Liabilities | 334,634 | 267,453 | 25% | 334,634 | 305,464 | 267,453 | 10% | 25% |

| Key Metrics (%) | Dec’25 | Dec’24 | Δbps YoY | Dec’25 | Sep'25 | Dec’24 | Δbps QoQ | Δbps YoY |

| CAR (Capital Adequacy Ratio - Basel III) | 14.5% | 17.5% | (298) | 14.5% | 16.8% | 17.5% | (225) | (298) |

| CET1 (Common Equity Tier 1) ratio | 12.3% | 14.5% | (220) | 12.3% | 14.2% | 14.5% | (194) | (220) |

| Tier 1 Ratio | 13.4% | 16.0% | (260) | 13.4% | 15.5% | 16.0% | (208) | (260) |

- Total Assets increased 25% year-on-year to reach AED 335 billion, driven by 32% increase in loans to customers and 39% increase in the investment portfolio.

- The growth in the balance sheet is supported by continued momentum across segments - wholesale banking grew by 30% year-on-year to AED 190 billion, and the retail banking segment grew by 13% year-on-year to AED 36 billion.

- Customer Deposits increased 27% year-on-year to reach AED 205 billion with CASA growth of 20% year-on-year to AED 128 billion, with CASA mix of 62%.

- NPL Ratio remained the lowest in the industry at 1.0%, highlighting the strong quality of the loan book.

- The Bank maintained strong capital metrics, with a Capital Adequacy Ratio of 14.5%, a CET1 ratio of 12.3% and a Tier 1 ratio of 13.4%, all comfortably well-above regulatory requirements. The reduction in the Capital Adequacy Ratio from 17.5% to 14.5% reflects strong high-double-digit growth in loans and advances during the year.

Looking Ahead

2025 marked a defining year in Mashreq’s evolution, with the Bank delivering strong financial and operational outcomes while advancing its global footprint and reinforcing its institutional standing. This performance was achieved against a complex backdrop of softer interest rates, heightened regulatory requirements and global macro uncertainty, underscoring Mashreq’s ability to execute with discipline, resilience and strategic clarity.

Looking to 2026, Mashreq enters the year with clear momentum and a sharpened strategic focus. The Bank is positioned to accelerate innovation-led growth through continued investment in advanced digital platforms, artificial intelligence and data-driven capabilities, strengthening scalability, decisioning and client experience across businesses. Expansion of digital propositions, deeper cross-border connectivity and continued focus on financial inclusion will further enhance Mashreq’s ability to serve clients seamlessly across markets.

Mashreq will continue to selectively strengthen its international presence along key UAE- and GCC-linked corridors, reinforcing its role as a globally connected banking partner supporting trade flows, capital mobility and institutional client activity.

Supported by strong capitalisation, healthy efficiency metrics and a diversified revenue base, Mashreq is well positioned to deliver sustained growth and long-term value, while continuing to build a resilient, future-ready institution that remains relevant across economic cycles and evolving client needs.

Financial Year 2025 Awards

Mashreq received multiple prestigious awards in 2025 across the Middle East and globally, reaffirming the Bank’s leadership and excellence in the industry:

- The Banker

- Bank of the Year – UAE

- The Banker – Top 1000 World Banks

- Best Performing Bank in the UAE (third consecutive year)

- #1 in the Middle East for Return to Capital (third consecutive year)

- #1 in the Middle East for Return on Assets (second consecutive year)

- Number 1 listed bank in the Middle East by S&P Market Intelligence

- Forbes Middle East - Most Sustainable Projects in the Middle East

- Gartner Eye on Innovation Award

- Innovation in Financial Operations – Cypher

- Euromoney Transaction Banking Awards

- The Middle East’s Best Cash Management Bank

- Euromoney Real Estate Awards

- Best Bank for Real Estate in the Middle East

- Euromoney Financial Institutions Awards

- #1 Trade Finance provider in Africa and leader in the Middle East

- Euromoney Cash Management Survey

- Ranked #1 by clients across the Middle East

- Euromoney Trade Finance Survey

- Best Trade Finance Bank in ME

- Euromoney Awards for Excellence

- The Middle East’s Best Bank for Large Corporates

- The Middle East’s Best Digital Bank for Large Corporates

- The Middle East’s Best Bank for Homeowners

- The Digital Banker – Global Islamic Finance Awards

- Best Islamic Digital Bank - Middle East

- Euromoney Private Banking Award

- United Arab Emirates’ Best for Family Office Services

For media enquiries, please contact Public Relations

Email: Media@mashreq.com

For investor relations enquiries, please contact: Investor Relations

Email: InvestorRelations@mashreq.com

Disclaimer

This document has been prepared by Mashreq Bank PSC (“Mashreq”) solely for informational purposes. The views, statements, and data presented herein do not represent a public offer or invitation to subscribe to, purchase, or sell any financial instruments or securities. Furthermore, this document should not be construed as investment advice or a recommendation regarding any financial product. It is not intended for distribution in any jurisdiction where such dissemination would violate applicable laws or regulations.

The content in this communication is intended to provide general insights into Mashreq’s operations, performance, and strategic direction. While care has been taken in preparing the material, it may include data derived from third-party sources, which have not been independently validated. No warranty or representation is made as to the accuracy or completeness of the information, and it should not be relied upon as the sole basis for making investment decisions. Readers are encouraged to seek their own independent financial, legal, or tax advice tailored to their specific circumstances.

This document may contain projections or forward-looking statements reflecting current views of Mashreq’s management concerning future events, financial conditions, or performance. These statements are inherently subject to known and unknown risks and uncertainties, including economic developments, interest rate movements, regulatory shifts, geopolitical events, and other factors beyond the Bank’s control.

Consequently, actual results may differ significantly from those anticipated. Mashreq does not undertake any obligation to update or revise forward-looking statements to reflect future events or changes in expectations, except as required by applicable laws.

Mashreq Bank PSC

P.O. Box 1250

Dubai, United Arab Emirates