Dubai: Leading global professional services firm Alvarez & Marsal (A&M) today released its latest UAE Banking Pulse for Q1 2019,which shows that the UAE banks are generating healthy earnings despite tougher economic conditions. The fundamental theme in the three-month period ending March 2019 is a surge in profitability, underpinned by increase in loans and advances, and a stabilised yield on credit.

After steady growth over the last 18 months, this trend was reversed in Q1 2019. The report finds that overall operating income has risen significantly from Q4 2018 driven by non-interest income, off-setting decrease in interest income. Decrease in cost-to-income-ratio (C/I) is in line with seasonal trends, driven by decreased quarterly costs and increasing quarterly revenues (lower costs compared to Q1’18 reflect the impact of cost cutting).

Alvarez & Marsal’s UAE Banking Pulse compares the data of the nine largest listed banks in the UAE, looking at the first quarter of 2019 (Q1 2019) against the previous quarter (Q4 2018).

The prevailing trends identified for Q1 2019 were as follows:

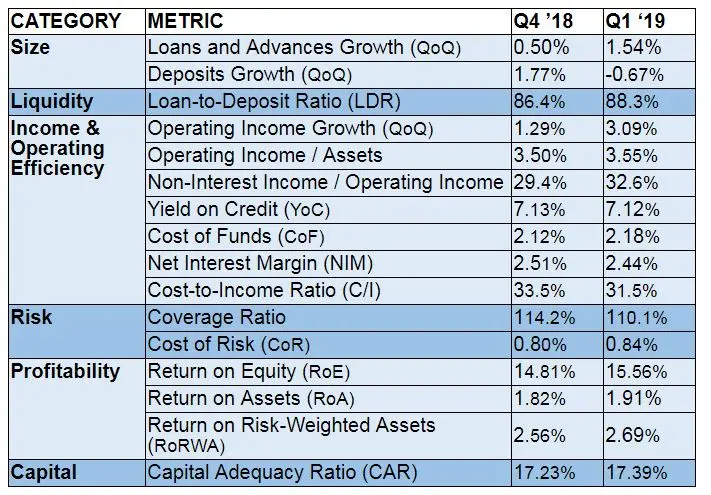

1. Loans and advances for the top nine banks grew at a faster rate (1.54 percent) than deposits, which was negative (-0.67 percent) after six consecutive periods of increase. Overall loans to deposit ratio (LDR) increased to 88.3 percent with eight of top nine banks in the LDR “green zone” of between 80 and 100 percent. Liquidity is expected to continue to be stable in 2019.

2. Operating income growth increased significantly on the back of a rise in non-interest income following increased lending activity

3. A downward trend of Net Interest Margin (NIM) continued in the quarter due to an increase in cost of funds, stabilised yield on credit, and rise in LDR. Six of the top nine banks witnessed a decrease in NIMs. Liquidity has tightened based on a decrease in deposits and an increase in cost of funds

4. Seven of the top nine bank’ cost-to-income (C/I) ratio decreased from 33.5 percent to 31.5 percent, reversing last quarter’s increase. This was due to the surge in operating income, combined with some banks reducing sales and general administrative costs. After a quadruple rise in 2018, the overall C/I ratio decreased.

5. The upward trend in cost of risk continues from Q4 2018. The climb is driven by a corresponding increase in net loan loss provisions, although four banks decreased their cost of risk. Coverage ratio continuing the downward trend.

6. Return on equity (RoE) maintained high levels despite the increase in cost of funds and a fringe increase in operating income. This resulted at the expense of stabilised yield on credit and increased adequacy ratio (CAR). Six out of nine banks exhibited an increase in RoE.

Alvarez & Marsal’s report uses independently sourced published market data and 16 different metrics to assess the banks’ key performance areas, including size, liquidity, income, operating efficiency, risk, profitability and capital.

The country’s nine largest listed banks analysed in A&M’s UAE Banking Pulse are First Abu Dhabi Bank (FAB), Emirates NBD (ENBD), Abu Dhabi Commercial Bank (ADCB), Dubai Islamic Bank (DIB), Mashreq Bank (Mashreq), Abu Dhabi Islamic Bank (ADIB), Commercial Bank of Dubai (CBD), National Bank of Ras Al-Khaimah (RAK) and the National Bank of Fujairah (NBF).

OVERVIEW

The table below sets out the key metrics:

Source: Financial statements, investor presentations, A&M analysis

A&M Managing Director and Middle East Office Co-Head in the firm’s Strategic Performance Improvement Practice, Dr. Saeeda Jaffar, was the lead author of the report. It was co-authored by A&M Head of Financial Services Asad Ahmed, along with Neil Hayward, Managing Director and Middle East Co-Head, who specialises in turnaround and restructuring.

Dr. Jaffar commented: “Overall the profitability for the UAE banks has increased. This stems from increased operating income, reduced costs and increased balance sheet leveraging, offset by an increase in cost of risk. This very much reflects the funding cost pressures that continue to impact the banks amid increased competition for deposits and tighter liquidity, consequently leading to lower net interest margins in Q1 2019.”

“Whilst it is possible that liquidity could tighten in the coming months, we continue to maintain a balanced view towards the sector, with a focus on asset quality and improving profitability. The tightening could also help banks readjust business models now shaped by new financing-cost realities,” she concluded.

© Press Release 2019Disclaimer: The contents of this press release was provided from an external third party provider. This website is not responsible for, and does not control, such external content. This content is provided on an “as is” and “as available” basis and has not been edited in any way. Neither this website nor our affiliates guarantee the accuracy of or endorse the views or opinions expressed in this press release.

The press release is provided for informational purposes only. The content does not provide tax, legal or investment advice or opinion regarding the suitability, value or profitability of any particular security, portfolio or investment strategy. Neither this website nor our affiliates shall be liable for any errors or inaccuracies in the content, or for any actions taken by you in reliance thereon. You expressly agree that your use of the information within this article is at your sole risk.

To the fullest extent permitted by applicable law, this website, its parent company, its subsidiaries, its affiliates and the respective shareholders, directors, officers, employees, agents, advertisers, content providers and licensors will not be liable (jointly or severally) to you for any direct, indirect, consequential, special, incidental, punitive or exemplary damages, including without limitation, lost profits, lost savings and lost revenues, whether in negligence, tort, contract or any other theory of liability, even if the parties have been advised of the possibility or could have foreseen any such damages.