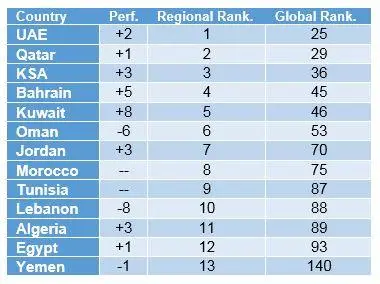

Geneva, Switzerland – For the 4th consecutive year, the UAE proved to be most competitive economy in the Arab region, according to The Global Competitiveness Report 2019, published today by the World Economic Forum. Having improved its positin with two points compared to last year, the UAE ranks 25th globally.

The UAE performance whitnessed an improvement in 52 out of 103 indicators organized into 12 pillars, calculated in the report. Additionally, the country ranked among the top 5 performing economies in 19 indicators, and among the top 20 worldwide in 57 indicators, i.e. more than half of the indicators included in the report this year.

Overall,the Arab world has caught up significantly on ICT adoption and many countries have built sound infrastructure. Most of the countries in the region whitnessed an importovement except for The Sultanate of Oman, Lebanon and Yemen. However, greater investments in human capital, are needed to transform the countries in the region into more innovative and creative economies.

The United Arab Emirates (25th) lead the regional ranking, followed by Qatar (29th) and Saudi Arabia (36th); Kuwait is the most improved in the region (46th, up eight) while Lebanon, Oman and Yemen lose some ground.

Ten years on from the global financial crisis, the global economy remains locked in a cycle of low or flat productivity growth despite the injection of more than $10 trillion by central banks. While these unprecedented measures were successful in averting a deeper recession, they are not enough on their own to catalyse the allocation of resources towards productivity-enhancing investments in the private and public sectors. The Global Competitiveness Report 2019, published today points to the path forward.

Launched in 1979, the report provides an annual assessment of the drivers of productivity and long-term economic growth. The assessment is based on the Global Competitiveness Index (GCI), which maps the competitiveness landscape of 141 economies through 103 indicators organized into 12 pillars. These pillars are: Institutions, Infrastructure; ICT adoption; Macroeconomic stability; Health; Skills; Product market; Labour market; Financial system; Market size; Business dynamism; and Innovation capability. For each indicator, the Index uses a scale from 0 to 100 and the final score shows how close an economy is to the ideal state or “frontier” of competitiveness.

This year, the Report finds that, as monetary policies begin to run out of steam, it is crucial for economies to boost research and development, enhance the skills base of the current and future workforce, develop new infrastructure and integrate new technologies, among other measures.

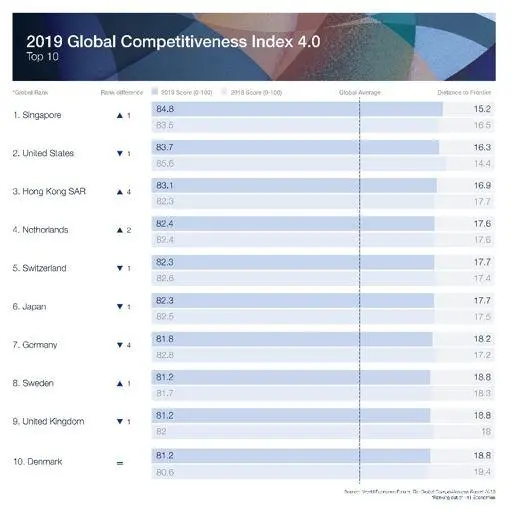

With a score of 84.8 (+1.3), Singapore is the world’s most competitive economy in 2019. The United States remains the most competitive large economy in the world, coming in at second place. Hong Kong SAR (3rd), Netherlands (4th) and Switzerland (5th) round up the top five. The average across the 141 economies covered is 61 points, almost 40 points to the frontier. This global competitiveness gap is of even more concern as the global economy faces the prospect of a downturn. The changing geopolitical context and rising trade tensions are fuelling uncertainty and could precipitate a slowdown. However, some of this year’s better performers in the GCI appear to be benefiting from the trade feud through trade diversion, including Singapore (1st) and Viet Nam (67th), the most improved country in this year’s Index.

“The Global Competitiveness Index 4.0 provides a compass for thriving in the new economy where innovation becomes the key factor of competitiveness. The report shows that those countries which integrate into their economic policies an emphasis on infrastructure, skills, research and development and support those left behind are more successful compared to those that focus only on traditional factors of growth.” said Klaus Schwab, Founder and Executive Chairman of the World Economic Forum.

The Report documents emerging areas of promising policies, reforms and incentives to build more sustainable and inclusive economies. To manage the transition to a greener economy, the Report recommends four key areas of action: engage in openness and international collaboration, update carbon taxes and subsidies, create incentives for R&D, and implement green public procurement. To foster shared prosperity, the Report recommends four additional areas of action: increase equality of opportunity, foster fair competition, update tax systems and their composition as well as social protection measures, and foster competitiveness-enhancing investments.

Regional and country highlights

G20 economies in the top 10 include the United States (2nd), Japan (6th), Germany (7th) and the United Kingdom (9th) while Argentina (83rd, down two places) is the lowest ranked among G20 countries.

The United States (2nd overall) is the leader in Europe and North America. The United States remains an innovation powerhouse, ranking 1st on the Business dynamism pillar and 2nd on Innovation capability. It is followed by the Netherlands (4th), Switzerland (5th), Germany (7th), Sweden (8th), the United Kingdom (9th) and Denmark (10th). Among other large economies in the region, Canada is 14th, France 15th, Spain 23rd and Italy 30th. The most improved country is Croatia (63rd).

The presence of many competitive countries in East Asia and the Pacific makes this region the most competitive in the world, followed closely by Europe and North America. In Asia Pacific, Singapore leads the regional and the global ranking thanks to a top-10 performance in seven of the 12 GCI pillars, including Infrastructure (95.4), Health (100), Labour market (81.2), Financial system (91.3), quality of public institutions (80.4) and it takes advantage of being the most open economy in the world. It is followed by Hong Kong SAR (3rd), Japan (6th), and Korea (13th). China is 28th (the highest ranked among the BRICS) while the most improved country in the region this year (Viet Nam) is 67th. The ranking reveals how heterogenous the regional competitiveness landscape is. Although the region is home to some of the most technologically advanced economies in the world, the average scores of the innovative capability (54.0) and business dynamism (66.1) are relatively low, lagging behind Europe and North America.

In Latin America and the Caribbean, Chile (70.5, 33rd) is the most competitive economy thanks to a stable macroeconomic context (1st, with 32 other economies) and open markets (68.0, 10th). It is followed by Mexico (48th), Uruguay (54th), and Colombia (57th). Brazil, despite being the most improved economy in the region is 71st; while Venezuela (133rd, down six places) and Haiti (138th) close the regional ranking. The region has made important improvements in many areas, yet it still lags behind in terms of institutional quality (the average regional score is 47.1) and innovation capability (34.3), the two lowest regional performances.

Eurasia’s competitiveness ranking sees the Russian Federation (43rd) on top, followed by Kazakhstan (55th) and Azerbaijan (58th), both improving their performance. Focusing on Financial development (52.0), and Innovation capability (35.5) would help the region to achieve a higher competitiveness performance and advance the process towards structural change.

In South Asia, India, in 68th position, loses ground in the rankings despite a relatively stable score, mostly due to faster improvements of several countries previously ranked lower. It is followed by Sri Lanka (the most improved country in the region at 84th), Bangladesh (105th), Nepal (108th) and Pakistan (110th).

Led by Mauritius (52nd), sub-Saharan Africa is overall the least competitive region, with 25 of the 34 economies assessed this year scoring below 50. South Africa, the second most competitive in the region, improves to the 60th position, while Namibia (94th), Rwanda (100th), Uganda (115th) and Guinea (122nd) all improve significantly. Among the other large economies in the region, Kenya (95th) and Nigeria (116th) also improve their performances, but lose some positions, overtaken by faster climbers. On a positive note, of the 25 countries that improved their Health score by two points or more, 14 are from sub-Saharan Africa, making strides to close the gaps in healthy life expectancy.

Global trends and highlights

In addition to providing an annual assessment of economies’ long-term health, the Report also highlights five trends in the global economy and their implications for economic policymakers

- The last ten years saw global leaders take rapid action to mitigate the worst of the financial crisis: but this alone has not been enough to boost productivity growth.

- With monetary policy running out of steam, policymakers must revisit and expand their toolkit to include a range of fiscal policy tools, reforms and public incentives

- ICT adoption and promoting technology integration is important but policymakers must in parallel invest in developing skills if they want to provide opportunity for all in the era of the Fourth Industrial Revolution.

- Competitiveness is still key for improving living standards, but policymakers must look at the speed, direction and quality of growth together at the dawn of the 2020s.

- It is possible for an economy to be growing, inclusive and environmentally sustainable – but more visionary leadership is needed to place all economies on such a win-win-win trajectory.

The report’s data also shows growing inequalities in the global economy.

- Market concentration: The report finds that business leaders in the United States, China, Germany, France and the United Kingdom believe that market power for leading firms has intensified over the past 10 years.

- Skills gap: Only the United States among G7 economies features in the top 10 on the ease of finding skilled employees. It is, in fact, the best economy in the world in this category. Of the others, the United Kingdom comes next (12th) followed by Germany (19th), Canada (20th), France (41st), Japan (54th) and Italy (63rd). China comes 40th.

- Technology governance: Asked how the legal frameworks in their country are adapting to digital business models, only four G20 economies make it into the top twenty. These are; the United States (1st), Germany (9th), Saudi Arabia (11th) and the United Kingdom(15th). China comes 24th in this category.

“What is of greatest concern today is the reduced ability of governments and central banks to use monetary policy to stimulate economic growth. This makes it all the more important that competitiveness-enhancing polices are adopted that are able to boost productivity, encourage social mobility and reduce income inequality,” said Saadia Zahidi, Head of the Centre for the New Economy and Society at the World Economic Forum.

About the new Global Competitiveness Index 4.0

Building on four decades of experience in benchmarking competitiveness, the World Economic Forum’s Global Competitiveness Index 4.0 is a composite indicator that assesses the set of factors that determine an economy’s level of productivity – widely considered as the most important determinant of long-term growth.

Platform for Shaping the Future of the New Economy and Society

The Global Competitiveness Report is a flagship publication of the World Economic Forum’s Platform for Shaping the Future of the New Economy and Society. The Platform provides the opportunity to advancing prosperous, inclusive and equitable economies and societies. It focuses on co-creating a new vision in three interconnected areas: growth and competitiveness; education, skills and work; and equality and inclusion. Working together, stakeholders deepen their understanding of complex issues, shape new models and standards and drive scalable, collaborative action for systemic change.

Over 100 of the world’s leading companies and 100 international, civil society and academic organizations currently work through the Platform to promote new approaches to competitiveness in the Fourth Industrial Revolution economy; deploy education and skills for tomorrow’s workforce; build a new pro-worker and pro-business agenda for jobs; and integrate equality and inclusion into the new economy, aiming to reach 1 billion people with improved economic opportunities.

Learn about the World Economic Forum’s impact: https://www.weforum.org/our-impact

View the best Forum Flickr photos at http://wef.ch/pix

Become a fan of the Forum on Facebook at http://wef.ch/facebook

Follow the Forum on Twitter at http://wef.ch/twitter

Read the Forum blog at http://wef.ch/agenda

View upcoming Forum events at http://wef.ch/events

Subscribe to Forum news releases at http://wef.ch/news

The World Economic Forum, committed to improving the state of the world, is the International Organization for Public-Private Cooperation.

The Forum engages the foremost political, business and other leaders of society to shape global, regional and industry agendas. (www.weforum.org).

© Press Release 2019Disclaimer: The contents of this press release was provided from an external third party provider. This website is not responsible for, and does not control, such external content. This content is provided on an “as is” and “as available” basis and has not been edited in any way. Neither this website nor our affiliates guarantee the accuracy of or endorse the views or opinions expressed in this press release.

The press release is provided for informational purposes only. The content does not provide tax, legal or investment advice or opinion regarding the suitability, value or profitability of any particular security, portfolio or investment strategy. Neither this website nor our affiliates shall be liable for any errors or inaccuracies in the content, or for any actions taken by you in reliance thereon. You expressly agree that your use of the information within this article is at your sole risk.

To the fullest extent permitted by applicable law, this website, its parent company, its subsidiaries, its affiliates and the respective shareholders, directors, officers, employees, agents, advertisers, content providers and licensors will not be liable (jointly or severally) to you for any direct, indirect, consequential, special, incidental, punitive or exemplary damages, including without limitation, lost profits, lost savings and lost revenues, whether in negligence, tort, contract or any other theory of liability, even if the parties have been advised of the possibility or could have foreseen any such damages.