Measured in local currency, Chinese equities were February's star performers. But China's eventual aspirations are far more ambitious than just topping the charts in a single month, and promoting its domestic equity market is a linchpin of this grand strategy.

Global equities continued to rise in February with the MSCI World Total Return Net in United States dollar terms up 3 percent and the MSCI Emerging Markets Total Return Net in dollars up only 0.2 percent, despite the fact that Chinese equities rose 15 percent in local currency, making China the best play globally in February.

With equity momentum easing in emerging markets and forward-looking macro numbers still not turning, should investors be on the defensive? Our view is still that investors should still play equity markets defensively. Many signs indicate that the business cycle is turning, but this may take several months. Be patient.

While our overall stance is defensive there are still opportunities in this part of the business cycle, both in relative and absolute terms. In our monthly equity presentation from February 26 we highlight three markets (South Korea, Australia and Hong Kong) and five industries (Retailing, Pharmaceuticals, Software & Services, Telecommunication and Media) as segments of the equity market that tend to do well when the economy is operating below its recent trend and is still slowing (current phase of the business cycle).

The single stock names highlighted below are objectively selected based on being in the top five on market capitalisation. In essence treat these stocks as indications of names to find in these equity segments and not as investment recommendations.

Looking at global equities from a helicopter perspective, valuation is still not an issue. As of February, global equities are valued just above their average valuation level since 1995. Investors should worry less about valuation and worry more about the trajectory of monetary policy and macro. Monetary policy is shifting gear. The European Central Bank has delayed policy normalisation and is now contemplating (T)LTRO (Targeted Long Term Refinincing Options, a form of cheap debt used as a stimulus) as a means to provide credit to the system.

The Fed has made a historic U-turn and vice chairman Richard Clarida recently said that yield cap as an instrument is on the table. We are going deeper into the rabbit hole in terms of monetary policy. On the margin here it is likely positive for equities but in the longer term the outcome is more uncertain.

The Chinese equity dream

In many ways China wants what the US has - a global reserve currency, strong financial markets, a large military, the biggest economy in the world, etc. China has come a long way in the past couple of decades and is now a real challenge to the US.

Even on a conceptual level, China is copying the US narrative and historic path. Xi Jinping talks about the Chinese dream and for that to succeed, the country needs broad inclusion in the upswing. In the last century, the US managed that through spreading the gospel of equity ownership and by preaching the wonders of the equity market. Now China is likely to pursue the same route.

The government knows that leverage in society is high and linked to housing. Using the equity market, the government will likely try to contain leverage in the housing sector and instead direct resources and support towards the equity market. If the Chinese population adopts equity ownership of corporate China then wealth will spread like a butterfly to all corners of the Chinese society.

The Chinese government also announced in November 2018 that the Shanghai Stock Exchange is approved for their version of ChiNext (a NASDAQ-style board for Chinese technology on the Shenzhen Stock Exchange). We expect measures and support for Chinese equities will continue to rise in importance for China’s government as a vehicle to continue growing the economy.

Assisting the Chinese efforts to create the Chinese equity dream, MSCI has announced that Chinese A-shares will see their inclusion factor in the MSCI Emerging Markets Index rise from the current level of 5 percent, up to 20 percent in three stages, with each stage (May/Aug/Nov 2019) involving a 5 percent rise.

This is big news that means that China is clearly pursuing open market reforms faster than initially calculated for by global investors. Deeper integration in global financial markets obviously reconfigures the global financial system, which creates new and deeper feedback loops. From China’s perspective, this is the necessary road to an eventual floating currency, which is the end destination if China truly wants to become the leading country in the world.

(Source: Banxia Fund, Saxo Bank)

Click image to enlarge

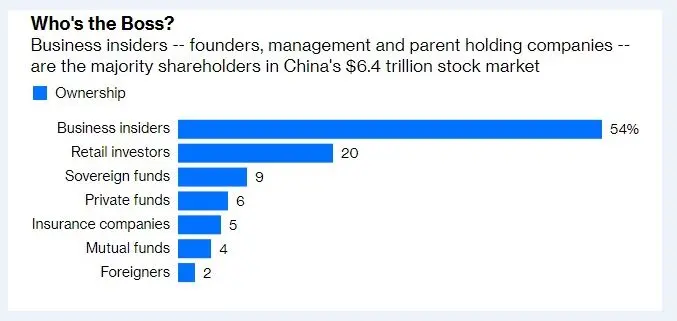

The bigger question is now whether the rising inclusion factor in the MSCI Emerging Markets Index leads to a rally in Chinese equities. It’s almost impossible to answer this question as price setting is a function of buyers and sellers. Foreigners own 2 percent of the total market capitalisation and 6.7 percent of the free-float market capitalisation, according to the People’s Bank of China.

The share of foreign ownership will now rise and if not driven by active investors, then surely by passive ETFs. But this inflow is in itself not enough to raise equity valuation or prices because there are sellers (likely domestic Chinese people) on the other side and depending on their liquidity needs it may not lead to anything.

Equity markets rise long-term due to rising corporate earnings. Everything else is just mean-reverting noise.

Any opinions expressed in this article are the author's own.

Disclaimer: This article is provided for informational purposes only. The content does not provide tax, legal or investment advice or opinion regarding the suitability, value or profitability of any particular security, portfolio or investment strategy. Read our full disclaimer policy here.