The sukuk market has grown considerably over the past decade, with several reasons driving the increased demand for global shariah-compliant bonds. Notably among these growth drivers is the global sukuk market’s track record of delivering strong risk-adjusted returns relative to other emerging market bonds, particularly during the COVID-19 crisis.

However, while many signs point to continued sukuk market growth, shariah-compliant investment product offerings are sparse, resulting in a significant gap between demand and supply.

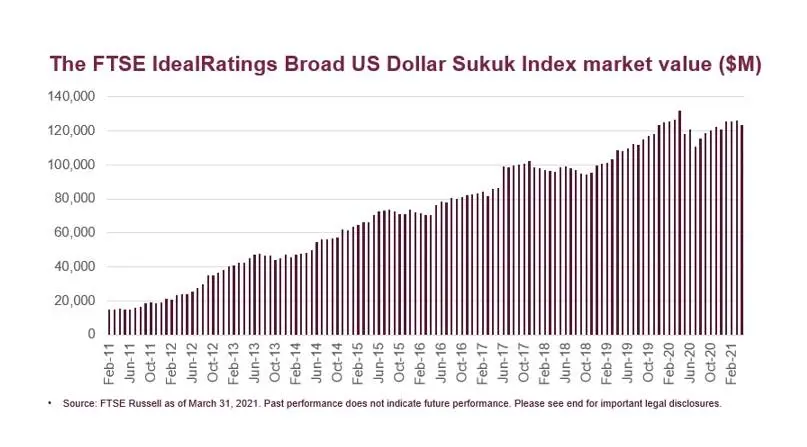

As the GCC region has grown in relevance for emerging market investors in recent years, so too has the sukuk market. Global sukuk market issuances had a record year 2019, with new issuances totalling $145.70 billion. And if we look over the past decade and use our FTSE IdealRatings Broad US Dollar Sukuk Index as a metric, its market value has grown from $15.0 billion in February 2011 to $126 billion in March 2021—representing a CAGR of 23%.

There are several trends that could signal continued growth for sukuk markets. Some GCC economies, Saudi Arabia, for example, are diversifying away from oil dependence and seeking alternative cash generation methods from other private sectors. As government wealth in these countries reaches the hands of the private sector and individuals, shariah-compliant assets could be likely beneficiaries. And more broadly, nearly a quarter of the world’s population identify themselves as Muslim, which could continue to drive shariah-compliant investment product demand.

A history of risk-adjusted outperformance

The sukuk market has also garnered investor attention for its growth potential. As investors hunt for yield in a prolonged low interest rate environment, sukuk exposure can be a potential source of yield that has historically delivered higher risk-adjusted returns relative to the broader EM bond market—even in times of crisis.

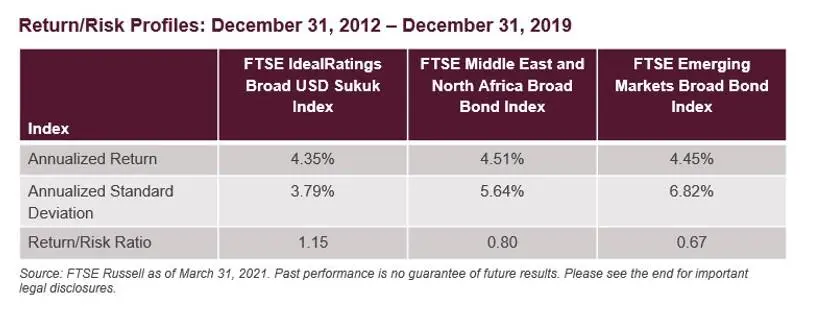

As shown below, prior to the pandemic crisis, the FTSE IdealRatings Broad US Dollar Sukuk Index posted slightly lower returns than both the FTSE Middle East and North Africa Broad Bond Index and the FTSE Emerging Markets Broad Bond Index—but with substantially lower volatility. This resulted in higher risk-adjusted performance for the time period.

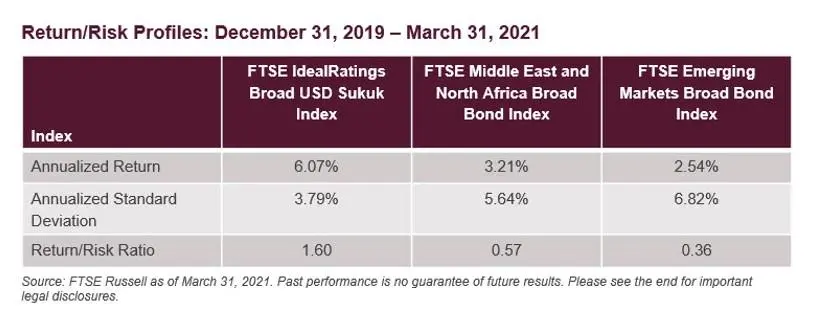

In the ensuing period of crisis, the sukuk market provided further outperformance on a risk-adjusted basis—demonstrating an ability to weather the turbulent markets at the onset of the pandemic.

Growing, but still underserved

Amid these trends, many investment managers and asset owners are facing growing demand to include shariah-compliant products in their offerings. More investors are viewing the global sukuk market as an opportunity to access a potentially high growth market, along with the prospect of additional yield and improved portfolios’ return/risk profiles.

However, there remains a lack of quality shariah-compliant investment products to meet this growing demand. The sector is still relatively immature, and establishing a presence can be difficult, slowing the pace of new product launches. But investors continue to demonstrate their growing interest in this market. According to Refinitiv, an LSEG business, the market for Islamic investment products is growing at an annual rate of 15-20 percent and is expected to reach $3.69 trillion by 2024.

An index for a largely untapped market

As demand grows, it’s important for investors to have an effective benchmark for measuring or passively tracking the sukuk market. At FTSE Russell, we relaunched our flagship FTSE IdealRatings Sukuk Index in 2020 to incorporate IdealRatings shariah screening methodology, ensuring index constituents pass their thresholds for compliance with Shariah law. The new FTSE IdealRatings Broad US Dollar Sukuk Index launched this year expands this constituent universe to include high-yield and non-rated sukuk as well as investment-grade.

Although demand is likely to continue to grow, with shariah funds launching throughout Islamic countries at first, followed by developed regions where there are significant Muslim populations, it’s possible that the gap between supply and demand will start to narrow. As supply grows, the global sukuk market could deepen and mature to become more integrated and homogeneous.

© Opinion 2021

Any opinions expressed in this article are the author’s own

Disclaimer: This article is provided for informational purposes only. The content does not provide tax, legal or investment advice or opinion regarding the suitability, value or profitability of any particular security, portfolio or investment strategy. Read our full disclaimer policy here.