PHOTO

The Saudi fintech market is witnessing unprecedented growth and in recent years begun to rival neighboring economies Egypt and the U.A.E. in startup investments, according to a report by the U.S.-Saudi Business Council.

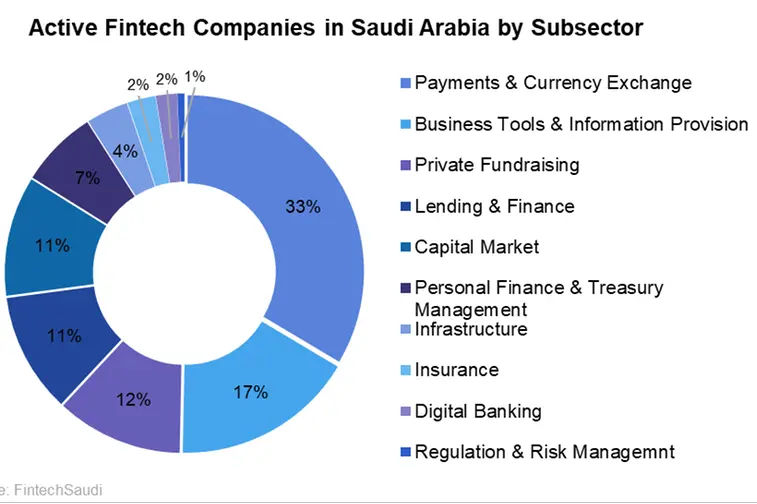

Saudi Arabia has one of the MENA region’s most developed and well-capitalized financial service sectors encompassing new technologies, which improve or automate financial services such as payments, lending, insurance, data management, and capital market services.

Through August 2022, the Kingdom witnessed a 79 percent YoY increase in the number of operating fintech firms. Of the 147 active fintech companies operating in Saudi Arabia, only 10 were operating in 2018. This rapid expansion is due to liberalized business regulations, an active investment environment, and well-developed technology infrastructure.

While the fintech private sector continues to grow, 2022 marked another record level of investment for Saudi fintech companies. Between September 2021 and August 2022, the fintech sector in the Kingdom saw SAR1.5 billion ($402.2 million) in total investments. Meanwhile, venture capital funding in Saudi Arabia surged more than threefold to SAR2.2 billion ($584 million) in H1 2022, surpassing the full-year total for 2021 as the Kingdom continues to invest in technology and digital transformation. Consequently, Saudi Arabia was ranked ninth globally for venture capital availability in IMD’s Global Competitiveness 2022 report, rising from 12th in the previous year.

“In the first half of 2022, fintech accounted for the highest number of total investment deals. Fintech companies attracted investments from leading domestic and international firms such as Sequoia, 500 Global, and Mastercard. Well-developed technology infrastructure such as widely accessible 5G and cloud services, a high domestic demand for financial services, and continued government support have all supported ongoing growth” said Albara’a Alwazir, Director of Economic Research at the U.S.-Saudi Business Council.

Saudi Arabia is aiming to reach a SAR13.3 billion ($3.6 billion) direct GDP contribution by 2030, up from SAR1.2 billion ($317 million) in 2021. The fintech sector will account for 18,200 direct jobs and reach 525 active fintech companies by 2030. Fintech is a key pillar of not only the financial services industry’s future, but as a cross-cutting enabler of numerous Vision 2030 initiatives such as raising private sector GDP, boosting small and medium enterprises (SMEs), attracting foreign investment, developing the digital economy, and enhancing the ease of doing business.

By 2025, Saudi Arabia aims to meet several benchmarks that include raising the number of active fintech players to at least 230 companies, reaching 70 percent non-cash transactions, and boosting fintech’s GDP contribution to SAR4.5 billion ($1.2 billion).

In addition to record rises in licensed fintech companies, the Saudi Cabinet approved the licensing of three local digital banks. The first involves the conversion of STC Pay into a digital bank with SAR2.5 billion ($667 million) in capital. The second involves Abdul Rahman bin Saad Al-Rashed and Sons Company, which established Saudi Digital Bank with SAR1.5 billion ($400 million) in capitalization. Most recently, D360 bank was licensed and became the third digital bank operating in Saudi Arabia. The PIF joined key investors in backing D360 Bank. These developments will introduce advantages that will provide payments services, consumer microfinance, and insurance brokerage services without requiring a physical business. The recent slate of digital bank licensing in Saudi Arabia brings the total number of licensed banks to 35 which includes 11 Saudi traditional banks, three Saudi digital banks, and 21 foreign banks. SAMA’s new Open Banking Policy is also expected to further boost competitiveness in the Saudi fintech sector as new financial products and business models may be developed as a result of open accessibility to consumer financial data.

Demand for a variety of financial services among Saudi residents is particularly high, including banking, insurance, investment, asset management, and shariah-compliant financing. The high level of smartphone penetration and banked youth population enabled a relatively rapid transition to a burgeoning digital economy. Use of card and electronic payments in Saudi Arabia have surged in recent years, rising steadily since 2016 with a further acceleration due to the COVID-19 pandemic. Saudi consumer habits have also adapted quickly to the digital economic transition. A 2022 Mastercard report found that 89 percent of people in Saudi Arabia have used at least one emerging payment method in the last year.