PHOTO

Ivory Coast and Kenya took advantage of demand for higher-yielding credit last week as the pace of public issuance from African sovereigns begins to pick up after a relatively slow start to the year.

Only Benin in January and Republic of the Congo on February 11 had issued in the public markets ahead of last week's two deals. Cameroon has also issued an international bond, but through a private placement. It tapped that note for an additional US$100m last week to take the outstanding size to US$850m.

Bankers had hoped for more public deals to have already priced, but timelines can easily drift. Still, with investors keen on riskier assets in spite of some broader market unease caused by AI developments, the door is open for African issuers as both Ivory Coast and Kenya showed.

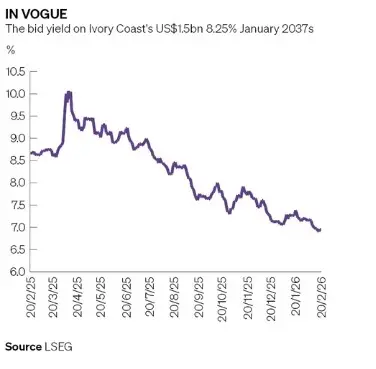

Ivory Coast (Ba2/BB/BB) went first with a US$1.3bn February 2041 amortising bond on Wednesday, which has a weighted-average life of 14 years.

"Along with Benin and Nigeria, they are the most well liked" of the sub-Saharan Africa sovereigns, said a lead banker. That was evident in the deal, which saw orders peak at more than US$5.85bn after books opened at the 7.75% area.

That enabled the leads to drive down pricing to a final yield of 7.125%. As a result of the pricing squeeze, final demand was just over US$3.3bn.

Still, the new issue came 12.5bp–20bp inside fair value, according to the banker. "It was a pretty solid repricing" of the curve, he said.

BNP Paribas, Citigroup, Deutsche Bank, JP Morgan, SMBC, Societe Generale and Standard Chartered were the bookrunners.

The deal was the sovereign's first since a one-notch upgrade from Fitch in December, which meant it has full Double B ratings from all three main rating agencies.

"They want to rerate their curve and move closer to South Africa," said the banker. South Africa (Ba2/BB/BB–) has a US$750m 6.25% March 2041 bond bid at 6.72%, according to LSEG.

"Investors were told beforehand that they would be price sensitive," said Thys Louw, portfolio manager at Ninety One. "They only issued US$1.3bn so wanted to price as tight as they could. But for a BB credit it still carried a decent amount of risk premium relative to the underlying credit."

With a presidential election behind it, held in October, and the high gold price offsetting a slump in cocoa prices, Ivory Coast is in a relatively good position politically and economically.

Moreover, investors have confidence in the credit. "They have a track record of sound management over a number of years. That's worth more than any commodity price," said the banker.

Trouble in Senegal

The main short-term risk is related more to what's going on in Senegal, which is trying to stave off a debt default. The sovereign has a €1bn 4.75% 2028 bond issue that starts amortising from next month.

Media reports last week, including from Reuters, said the government has raised enough financing in tax revenues and on the regional market to make the payment. But even if it does, it has other debt repayments due, with a spike in June and July.

Senegal is in talks with the IMF over a new programme after the multilateral froze the last one when the government unearthed billions of dollars of hidden debts run up by the previous administration.

A new programme is crucial to unlocking other funds, but any full-blown crisis could have a knock-on effect on Ivory Coast, a fellow member of the West African Economic and Monetary Union. "They share pooled resources and [Ivory Coast's] banks would have exposure to Senegalese sovereign paper. So there are second-order effects that could be felt," said the banker.

Turning point

Kenya (B/B–) returned for its fourth US dollar transaction since the start of 2024. In February that year it issued a US$1.5bn bond and launched a tender offer to tackle a US$2bn maturity due in June, a refinancing that at one point looked touch and go.

The deal proved to be a turning point, and since then Kenya has become a much more secure issuer. It has adopted the same new issue plus tender offer model for all its deals since, including this latest one on Thursday, as it continues to bring down its average cost of funding and push out any big maturities.

Refinancings for its foreign currency bonds for the rest of the decade total just over US$1bn, before spiking up from 2030 onwards.

Indeed, the US dollar market has become an important avenue of funding for Kenya because domestic rates are still relatively expensive even though they have come down markedly over the past year.

Kenya priced a US$900m February 2034 bond, with a weighted-average life of seven years, at 8.1% and US$1.35bn February 2039 tranche, with an average life of 12 years, at 8.95%.

Both tranches offered a double-digit premium over Kenya's curve, though that was still considered tight given the sovereign's ratings. Initial price thoughts were 8.375% area and 9.25%.

The new deal will go towards buying back an amount of up to US$150m including accrued interest of Kenya's 7.25% due 2028s and up to US$350m including accrued interest of its 8% due 2032s.

"The country has a very solid external balance story to present to investors, with a narrowing current account deficit over the last five years and an increase of FX reserves to all-time highs of US$12.4bn in December," said Giulia Pellegrini, a lead portfolio manager for EM debt at Allianz Global Investors.

Pellegrini also highlighted Kenya's solid economic growth and the inflation rate being under control.

"The Achilles' heel of the Kenyan story, in our view, remains the fiscal picture, with recent news of slippage in the current fiscal year," she said. "While the government's medium-term plans include meaningful fiscal consolidation, with limited revenue measures and a reliance on spending reductions, there is room for potential disappointment, as revenue outturns have been lower than planned in recent years."

Citigroup and Standard Bank were the bookrunners.

Source: IFR