PHOTO

A number of low-rated African sovereigns have issued at high yields in the US dollar markets this year to ease pressure on their domestic curves, highlighting the difficult balancing act these countries face in managing their liquidity needs.

Republic of the Congo, Cameroon and Kenya have all borrowed in US dollars, either in the public or private markets, as domestic and regional markets have become marked by higher rates. These deals have helped diversify avenues of funding and were well timed, especially as opportunities to issue can come and go quickly – as the past two weeks have illustrated following the outbreak of war in the Middle East.

However, such deals also underline that emerging market countries with relatively underdeveloped local capital markets can become vulnerable to exchange rate risk on their liabilities. Even countries whose currencies are pegged to the euro, such as Cameroon, may not necessarily be immune to FX shocks in a time of crisis. These deals also increase countries' sensitivity to global financial market volatility, especially given the elevated yields they have to pay.

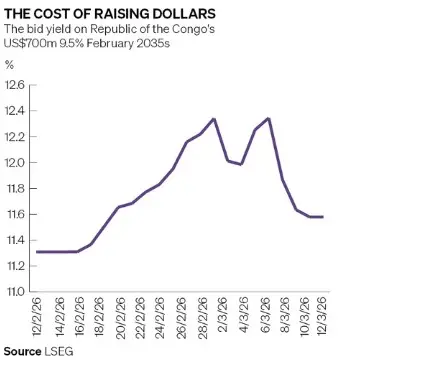

In February, in its first public issuance in US dollars, Republic of the Congo (Caa2/CCC+/CCC+) priced a US$700m 9.50% February 2035 amortising note at a yield of 11.625%.

The deal came just three months after the sovereign had privately placed a 9.875% November 2032 amortising bond at a yield of 13.70%, which was tapped a month later at 12.95%.

Part of the reason for the public issuance was to fund a tender offer for up to US$350m on the November 2032s, which had US$930m outstanding following the tap.

In late January, Cameroon (B–/B) privately placed a US$750m 8.875% January 2033 amortising bond at a yield of 10.125%. It was tapped for another US$100m three weeks later at 9.70%.

Worked well

Kenya (B/B–) issues at lower yield levels, pricing last month a US$900m February 2034 amortising bond at 8.10% and US$1.35bn February 2039 amortising tranche at 8.95%, with proceeds partially going towards a tender offer.

Thys Louw, an EM portfolio manager at Ninety One, said from a debt strategy point of the view the deal worked well in diversifying Kenya's "sources of liquidity and reducing pressure on domestic banks". It also delivered size and helped lengthen Kenya's curve.

However, with its public debt-to-GDP ratio at about 70% of GDP, according to the IMF, and interest costs eating up a big proportion of the annual budget, debt sustainability remains a big challenge for Kenya.

Risk appetite

That these sovereigns are able to issue in the US dollar market is a reflection of greater risk appetite. "Financing conditions are substantially better than a year ago for lower-rated credits," said Yvette Babb, EM portfolio manager at William Blair Investment Management.

At the same time, though, these deals underscore a tightening in funding conditions in domestic and regional markets as governments come to increasingly rely on them.

The weighted-average interest rate on Cameroon treasury bills, for example, increased from 2.67% to 6.65% between 2020 and 2025, according to a presentation last month to investors by finance minister Louis-Paul Motaze and reported by local media.

New face

In an IMF report published earlier this month titled "The New Face of African Debt", authors Amadou Sy and Athene Laws wrote: "The median country in sub-Saharan Africa issued domestic debt at an average of 8.8% interest in 2024. For many countries, this makes borrowing at home more expensive [than in US dollars]."

The IMF economists are not arguing against the importance of domestic markets – far from it. But for what should be countries' bread-and-butter source of funding, these high costs can have pernicious effects — especially in regions where local pools of capital aren't especially deep and financing structures aren't well developed.

"When domestic borrowing is a deliberate, well-planned component of a country’s financial toolkit, it can support resilience and sustainable growth. In contrast, countries that turn to domestic debt mainly as a crisis response — after losing access to external markets — often find themselves in a more vulnerable position," the IMF economists wrote.

Depressed prices

Senegal is having to rely on the regional West African Economic and Monetary Union market for liquidity and funding, even to service its foreign currency bonds, with its international debt trading at depressed prices.

The key for countries is to try and find a balance in their funding strategies and stabilise the state of their debt. But understanding the need to do so is one thing; being able to do so is another as countries are finding to their cost.

"I think we have unfortunately seen a few examples of Eurobonds being used as tactical short-term funding instruments, which can be very costly in the long term," said a banker. "Using long-term dollar debt to bridge short-term local market liquidity constraints is often the worst time to approach new offshore investors."

He was especially critical of the Congo and Cameroon private placements. "The proliferation of private placements has exacerbated this trend – with the promise of faster execution [but] little consideration seemingly given to the sometimes sizeable incremental cost."

Babb said that given the growing demand for higher-yielding assets, public issuance would be more cost-efficient than a private placement. At the same time, "in some pockets of African credit, spreads seemed elevated and the private placements cleared the way for these countries to come to the international markets".

"They faced limited choices to meet their payments," she said.

Cameroon needed a deal done in a short timeframe and the private route was the most expedient. Congo needed funds to refinance upcoming domestic debt but domestic liquidity had become tight, pushing up yields.

One avenue that sovereigns, such as Congo and Angola, are considering, to lower their debt burdens and enhance their economies, is debt-for-nature swaps, or some variation of the structure. But such deals are not a panacea.

"To work well you need outstanding bonds trading at a significant discount for the repurchase, and low rates for the new guaranteed debt. This achieves the necessary deleveraging and debt service benefit that are touted," said the banker. "The problem with these [deals] is they take so long to structure, the underlying conditions can be considerably different at issuance, and that efficiency can be lost."

Additional reporting by Burhan Khadbai