PHOTO

The six members of the Gulf Cooperation Council will need around $300 billion in sovereign funding between 2018 and 2021, down from $450 billion between 2015 and 2017, as the oil price improves and governments push ahead with revenue-generating programmes such as the introduction of value-added tax (VAT), according to the latest forecast issued on Wednesday by S&P Global Ratings. (Click Read the full report here.)

The cumulative deficits of the six GCC states (Saudi Arabia, the United Arab Emirates, Qatar, Kuwait, Oman and Bahrain) are forecast to be around $75 billion in 2019 (5.5 percent of total GCC gross domestic product), which is well below the high point of 2016 when deficits hit $190 billion and accounted for 16 percent of GCC GDP, the report added.

S&P Global Ratings said the shrinking deficits are due to two factors: oil and fiscal policies, such as the introduction of VAT in Saudi Arabia and the UAE. “The oil price has almost trebled from the $29 per barrel (/bbl) trough and is currently $80/bbl; that said, we assume the oil price will decline to $55/bbl by 2021,” the report said, adding that the lower oil price towards the end of the decade will mean the deficit reductions won’t be as sharp as some governments would like.

Below are some of the key findings from the latest S&P Global Ratings report:

Funding chest: It is estimated that total funding needed between 2015 and 2017 was $450 billion (12 percent of total GCC GDP). With $300 billion needed between now and 2021 (5 percent of GCC GDP), this brings the total funding needed among the six GCC members to $750 billion between 2015 and 2021.

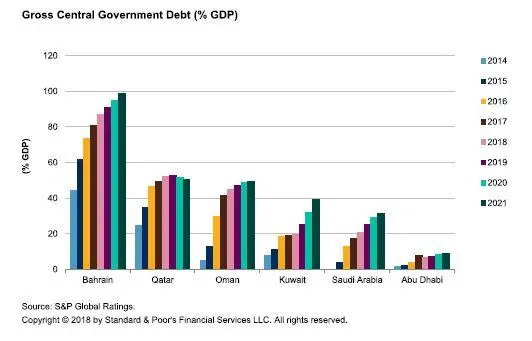

GDP impact: Saudi Arabia accounts for nearly half of the $300 billion total funding needed, but the figures differ when it comes to the proportion the individual members’ deficit represents of overall GDP. In Saudi Arabia, the UAE and Oman the deficits account for around five percent of GDP, while Kuwait’s deficit accounts for 13 percent of its GDP.

Debt law: Kuwait’s parliament has not passed a new debt law since October 2017 and it is expected to introduce a new one next year. However, if this does not happen it will hinder the country’s ability to issue new debt and address its rising deficit.

Private sector squeeze: A major factor for GCC governments’ ability to raise debt is the cost of doing so and the receptiveness of international and local markets. Investors’ perceptions of regional GCC geopolitical risks, such as the Qatar boycott, the recent backlash against Saudi Arabia and tensions with Iran, have elevated concerns. If sovereigns are forced to depend on local lenders instead of international markets this could have a consequence for the health of the overall economy. “A sharply increased reliance on domestic debt financing could result in the crowding-out of the private sector and hamper overall economic growth,” the report warned.

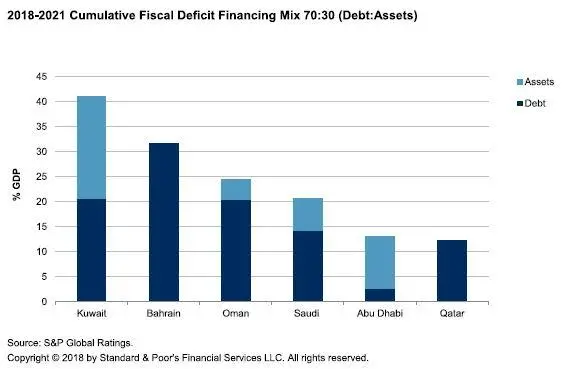

Funding split: When it comes to funding the $300 billion needed, it is forecast that 70 percent of this will come from debt issuance and 30 percent from asset drawdowns. However, again this will vary from country to country, with Bahrain and Qatar financing their deficits through debt, the UAE and Kuwait drawing down on their assets, while Saudi Arabia and Oman will show a 70:30 split in favour of debt.

Cost of debt: One determining factor in the debt-asset ratio is the cost of debt issuance. “We note that global liquidity is becoming scarcer and more expensive, while regional banking sector liquidity remains adequate,” the report said. This would be of particular concern to Bahrain as 23 percent of its government revenue is spent servicing its interest payments on debts and it is forecast to get half of the funding it needs from debt issuance.

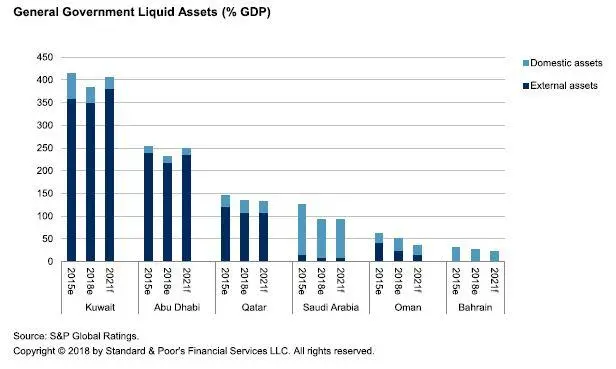

Shrinking assets: The drawing down of assets to fund deficits will have a long-term impact, with the report forecasting that Saudi Arabia's net assets will represent 65 percent of GDP by 2021, down from 71 percent in 2018. The amount of liquid assets countries have on their balance sheets also plays an impact on their sovereign rating, which in term determines how easy it is for them to raise funding. Countries whose assets represent less than 100 percent of GDP, such as Bahrain, Oman, and Saudi Arabia, felt the impact of the oil price fluctuations a lot more, while Kuwait, the UAE and Qatar are forecast to maintain liquid assets above 100 percent of GDP. “No region illustrates the support that large government liquid assets can provide to a sovereign rating better than the GCC,” the report said.

Islamic opportunity: The report said the scale of the funding requirement could open up the market for regional sovereign sukuk issuance, but S&P Global Ratings believes this also faces some challenges: “Work has been carried out by GCC governments over the past few years to establish the necessary legal frameworks for sukuk issuance programs in domestic and external markets. However, the complexity and slow speed to market of Islamic products continue to inhibit the industry's widespread growth, in our view.”

Click here to read the full S&P Global Ratings GCC Sovereigns report

(Graphs: Click on images below to enlarge)

Further reading:

• Government deposits in UAE-based banks to all-time high of $778bln

• Oil prices extend falls on well supplied market Iran sanction waivers

• MENA region will not escape impact of global trade war, says economist

• UAE's GDP to grow by 4.2% in 2019 and 2.8% this year - central bank governor

• Tough targets: Bahrain govt's fiscal reforms are overly ambitious - report

• Update: Gulf economies set to recover in 2018, but debt pile a concern - IMF

• Oil markets could witness modest surplus into early 2019 - Goldman Sachs

(Writing by Shane McGinley; Editing by Imogen Lillywhite)

(shane.mcginley@refinitiv.com)

Our Standards: The Thomson Reuters Trust Principles

Disclaimer: This article is provided for informational purposes only. The content does not provide tax, legal or investment advice or opinion regarding the suitability, value or profitability of any particular security, portfolio or investment strategy. Read our full disclaimer policy here.

© ZAWYA 2018