Steady Performance Despite the Political and Economic Troubles Still Facing Lebanon and the Region

The un-audited financial results of the four largest listed Lebanese banks -- BLOM, Audi, Byblos, and Bank of Beirut (BoB) -- show that they have maintained their steady performance in 2017, despite the exceptional conditions still facing Lebanon and the region. Aggregate operational, non-exceptional net profit of the four banks increased to $1,323.06 million in 2017, growing by 1.8% from 2016.

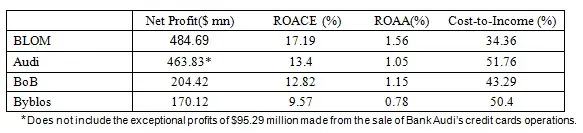

On an individual basis, BLOM Bank attained the highest level of operational, non-exceptional net profit of $484.69 million at end 2017, growing by 4.72% from 2016. Bank Audi came second with net profit at $463.83 million, down by 1.33%; whereas Bank of Beirut came third with net profit at $204.42 million, up by 1.51%. Byblos Bank’s net profit ranked fourth, rising by 2.9% to $170.12 million.

The profit performance of the four banks can also be seen by looking at profitability ratios, namely the rate of return on average common equity (ROACE) and on average assets (ROAA), which measure the productivity to generate earnings from equity and assets. BLOM Bank recorded the highest ROACE at 17.19% and the highest ROAA at 1.56%. The three other banks followed, with Bank Audi’s ROACE at 13.40% and ROAA at 1.05%; Bank of Beirut’s ROACE at 12.82% and ROAA at 1.15%; and Byblos Bank’s ROACE at 9.57% and ROAA at 0.78%. BLOM Bank’s effective performance can be attributed to its highly managerial and operational efficiency. This is demonstrated by BLOM Bank’s cost-to-income ratio of 34.36%, the lowest of all four, followed by 43.29% for Bank of Beirut, 50.4% for Byblos bank, and 51.76% for Bank Audi.

Growth was not limited to profits only, since it was also registered in most key balance sheet items. For Audi, its assets stood at $43.75 billion, falling by 1.16% from end 2016, and its loan portfolio was to $16.32 billion, decreasing by 5.25%, while its shareholder’s equity rose by 13.23% to $4.18 billion. BLOM reported $32.54 billion in assets, growing by 10.25%, and its loan portfolio grew by 5.22% to $7.54 billion, while its shareholder’s equity rose by 2.49% to $3.00 billion, despite the recalling of preferred shares 2011. BLOM Bank’s balance sheet aggregates naturally benefited from its acquisition and merger of the assets and liabilities of the three HSBC Lebanon branches on 17/6/2017. Assets at Byblos reached $22.66 billion, growing at 9.12%, and its loan portfolio increased by 5.21% to $5.45 billion, while its shareholder’s equity increased to $1.88 billion at a rate of 4.18%. As to Bank of Beirut, its assets rose by 6.78% to $18.37 billion, with its loan portfolio increasing by 19.24% to $5.69 billion, while its shareholder’s equity rose by 1.86% to $2.35 billion

Once again, these results show the top four listed Lebanese banks’ ability to sustain good growth and financial strength through excellent management and a conservative business model. As a result, they reconfirm the Lebanese banking sector’s position as the leading financial pillar in the country and the backbone of the economy.

© Press Release 2018