UBS believes that the euro is fundamentally flawed and hurts most of its members and they would be economically better off if they had never joined. But like Hotel California, you can check into the euro any time you like, you can never leave...

The euro does not work, exclaims UBS. "Under the current structure and with the current membership, the Euro does not work. Either the current structure will have to change, or the current membership will have to change," says the Swiss bank in a grim report.

Make no mistake, the crisis impacting the euro and Eurozone countries has the potential of ushering in a new global recession.

Indeed, legendary investor George Soros, who famously bet against the British pound, says the EU crisis could be worse than what was witnessed in 2008:

"This crisis has the potential to be a lot worse than Lehman Brothers. That is why the problem is so serious. You need a crisis to create the political will for Europe to create such an authority, but there is still no understanding as to what the authority will do."

He is also calling for a central authority, eurobonds and an exit mechanism for failing countries.

The hit to confidence from the intensified sovereign strains, which in July/August spread to Italy and even France, poses a major risk to Eurozone growth. The associated concerns about bank funding, potential constraints on the availability of credit and the downturn in the world trade cycle are also sources of concern.

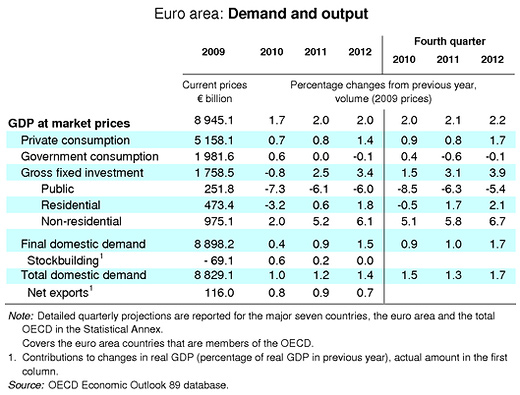

HSBC has slashed its growth rates for the EU, from 2% to 1.6% in 2011. "The bigger downgrade is to 2012, which we lowered to 1.4% in May and which we now forecast at just 0.7%."

"We are not... currently forecasting an outright recession in Germany as there will be some offset from the domestic side, although we have also trimmed our numbers for consumption," notes HSBC. "The countries that we see moving back into recession are Spain and Italy; in both cases we expect the contraction to begin in Q3 led by a slump in industry and exports, while the impact of the austerity measures will continue to bite in Spain and become more aggressive in Italy."

UBS'S Problem With The Euro

UBS argues that the European monetary union was mis-sold to European citizens. The Euro was seen as a foreign exchange integration which allowed trade and tourism to flourish without the drachamas, French francs and deutsche marks being flung about.

" Of course the exchange rate integration was probably the least of the consequences of the Euro. The most important consequence was the integration of monetary policy. The hint was in the name "European Monetary Union". However, politicians sought to ignore that hint. A Euro that had been promoted on the idea of monetary union rather than exchange rate integration would have been far more difficult to sell to the electorate."

The euro would have worked in economies that are homogeneous, not when different economies work at different speeds and in different directions.

"It was the great misfortune of the Euro that the early years of its life saw a monetary policy that was biased towards being too accommodative for some of its members," says UBS. "The consequence of this is that the problems of the monetary union were hidden under the politically expedient cloak of 'this time it's different', and asset bubbles built."

Worse, the euro expanded and added more economies into its fold, increasing the magnitude of the problem.

Hotel California

So if the euro is so dysfunctional, why not leave it, and return to your drachmas and liras? Not so fast.

Popular misconceptions include the idea that a country will be able to stimulate growth by simply leaving the Euro, that a country can be expelled from the Euro by other member states, or that a strong economy could leave the Euro without significant consequences - all of these arguments are wrong, says UBS.

The EU founders did not create a legal provision for members to leave the currency union, simply because it would have been seen as a lack of commitment to the eurozone.

"The existence of an opt-out - however structured - would have raised the possibility of a country exiting," notes UBS. "Making the (currently) impossible possible would make the event (exit) more likely. By failing to specify a technical mechanism for an exit, the costs of exit are significantly raised. The result is Hotel California: "you can check out ... but you can never leave".

A departure could lead to a devaluation of the seceding country's currency by as much as 60% and could lead to civil war scenarios.

"The economic costs of breaking up the Euro are high, and extremely damaging. The political costs of breaking up the Euro, even in part, are too great to quantify in bald cash terms," notes the Swiss bank.

UBS's base case scenario is that the euro will survive as some kind of fiscal confederation, providing automatic stabilisers to economies, not transfers to governments. This is how the US monetary union was resurrected in the 1930s. It is how the UK monetary union, and indeed the German monetary union, have held together.

But what if the disaster scenario happens? How can investors invest if they believe in a break-up, however low the probability? The simple answer is that they cannot.

"Investing for a break-up scenario has not guaranteed winners within the Euro area. The growth consequences are awful in any break-up scenario. The risk of civil disorder questions the rule of law, and as such basic issues such as property rights. Even those countries that avoid internal strife and divisions will likely have to use administrative controls to avoid extreme positions in their markets. The only way to hedge against a Euro break-up scenario is to own no Euro assets at all."

© alifarabia.com 2011