PHOTO

(A correction to the headline was made, replacing "Tuesday" by "Wednesday").

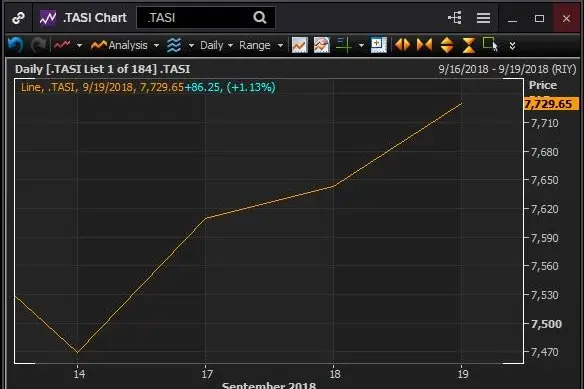

The Saudi market gained 1.13 percent on Wednesday, strengthening for the third consecutive session this week. It is now 0.69 percent higher for the week so far, despite falling 1.6 percent on Sunday.

Tadawul’s performance has been weak in September, dropping 2.8 percent so far this month.

Sentiment across global markets has been negatively affected by trade tensions, with mounting fears of a full blown trade war between the United States and China. Many investors have remained cautious or decided to stay on the sidelines until they see more clarity as to where the crisis is heading.

Weakness in emerging markets (EM) has weighed on sentiment in Saudi Arabia, with the MSCI Emerging Markets index down 3.43 percent so far in September. But an adjustment in oil prices on tightening supply has helped push the Saudi index higher, as investors priced in new U.S. sanctions on Iran, starting November.

A rebound in some of the stocks that incurred losses in the first half of the month has also boosted the index.

“Tadawul had witnessed considerable weakness in the first half of September, declining more than 6 percent. Accordingly, some support and pull back is not surprising,” Nishit Lakhotia, Head of Research at SICO, told Zawya by email.

“Tadawul is still close to 10 percent lower than its 52-week high and the actual flow-driven trigger from MSCI and FTSE will impact the markets in less than six months from now.

“So it is an opportune time to shop and pick the beta plays from the flow-driven rally,” Lakhotia argued.

The Saudi index is still up 6.91 percent in the year to date, and the surge can be mostly attributed to hopes from investors that index complier MSCI will include Riyadh in its benchmark emerging market index, which is expected to attract billions of dollars from foreign funds to the market - both passive and active funds. In June, MSCI said it would upgrade the kingdom to emerging market status in phases from mid-2019.

“It will also be interesting to see if the domestic institutional discretionary portfolio managers have stopped selling and started buying this week or not. They have been significant net sellers since July, this was last seen only in early 2016,” Lakhotia added.

Saudi Basic Industries Corporation (SABIC), Tadawul’s biggest share by market capitalisation and the world's fourth-biggest chemical firm, has added 1.53 percent so far this week and was one of the key factors pushing the index higher. But for September, SABIC has traded 5.23 percent lower.

SABIC and Switzerland's Clariant announced on Tuesday that they would merge their high-performance materials businesses. Sabic bought a 24.9 percent stake in Clariant in January this year.

“SABIC also had declined in line with the broader market’s weakness and of course there may be concerns relating to the Aramco PIF valuation on the SABIC deal,” SICO’s Lakhotia said.

“However, this is again a key beneficiary of the MSCI and FTSE inclusion and hence can witness some pullback on the back of this theme in the near term.”

The Saudi banking sector gave a big push to the index during the year, adding 5.96 percent year to date, according to data from Thomson Reuters Eikon. The banks were down 3.06 percent in September so far.

“Saudi banks’ profitability should remain good, aided by rising interest rates and controlled provisioning,” Shabbir Malik, a banking analyst at EFG-Hermes told Zawya.

“Loan growth remains weak, and we believe its pick-up would hinge on a meaningful rise in capex spending by the government. Overall, the banking system appears to be in good shape with adequate liquidity and capital buffers,” Malik added.

Elsewhere in the region, Dubai’s index dropped 0.08 percent on Wednesday, Abu Dhabi’s index added 0.16 percent, Qatar’s index retreated 0.18 percent, Kuwait’s index retreated 0.21 percent while Bahrain’s index edged up 0.08 percent and Oman’s index retreated 0.24 percent. Egypt’s market finished 3.79 percent lower.

(Reporting by Gerard Aoun; Editing by Michael Fahy)

(gerard.aoun@thomsonreuters.com).

Our Standards: The Thomson Reuters Trust Principles

Disclaimer: This article is provided for informational purposes only. The content does not provide tax, legal or investment advice or opinion regarding the suitability, value or profitability of any particular security, portfolio or investment strategy. Read our full disclaimer policy here.

© ZAWYA 2018