PHOTO

Fitch Ratings - London: Fitch Ratings has affirmed Qatar's Long-Term Foreign-Currency (LTFC) Issuer Default Rating (IDR) at 'AA' with a Stable Outlook.

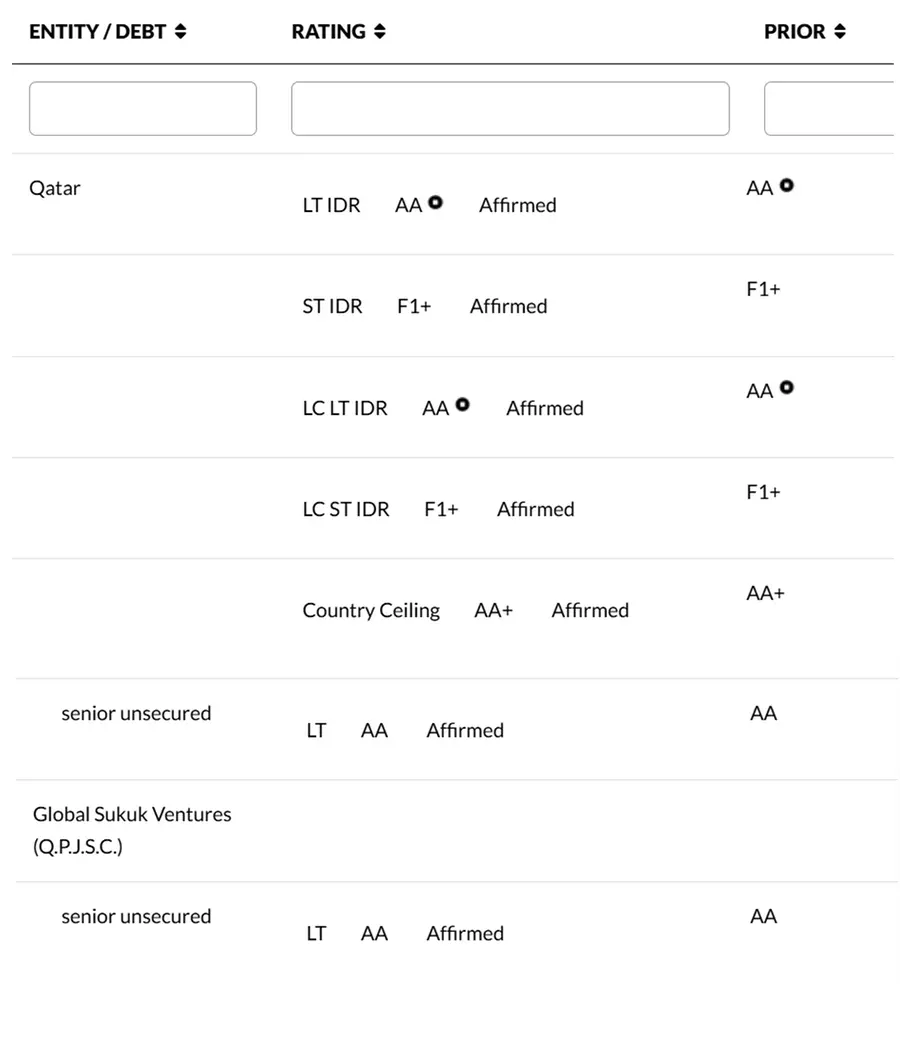

A full list of rating actions is at the end of this Rating Action Commentary.

The 'AA' rating reflects GDP per capita among the world's highest, large sovereign assets, our expectation that additional gas production will strengthen public finances further and a relatively flexible public finance structure. Rating weaknesses include heavy hydrocarbon dependence and below-average scores on some measures of governance, higher government debt/GDP than oil-dependent highly rated peers and substantial contingent liabilities.

Qatar's Stable Outlook reflects our expectation that its strong balance sheet and credible prospects for a significant rise in liquefied natural gas (LNG) production mitigate the impact of the Iran war. We assume a resumption of gas production once traffic in the Strait of Hormuz normalises. Our baseline scenario is that the closure will last less than a month.

KEY RATING DRIVERS

Temporary Halt to Energy Production: The effective closure of the Strait of Hormuz prevents nearly all exports of oil and gas from Qatar, with the exception of the Dolphin pipeline to the UAE (10% of hydrocarbon exports). Storage is at capacity and production at the LNG complex at Ras Laffan, which handles most of Qatar's liquefaction, has been suspended following an attack. The extent of the damage is currently being assessed. We expect the facility to remain closed for the duration of the conflict and to take several weeks to ramp up production once traffic in the strait resumes.

High Uncertainties Around Conflict Baseline: Our baseline is that the conflict will last less than a month and the Strait will be closed over this time. We assume there will not be major damage to hydrocarbon infrastructure and that Brent will average USD70 per barrel (b) for 2026. There is significant uncertainty about the regional security situation once the conflict ends.

Surge in Production Ahead: Fitch expects Qatar Energy (QE) to continue with its plans to expand LNG production capacity to 126 million tonnes per year (mtpa) by end-2027 from 77mtpa in 2025, and has announced further expansion to 142mtpa by end-2030. Our baseline assumes logistical challenges due to the war will delay the completion of the first phase of the North Field expansion, with the first new LNG trains only starting operations in 2027, compared with our previous expectations for late 2026.

We assume QE and its foreign partners will continue to invest in expanding production after the war. If the Strait remains closed longer than our baseline, or regional security conditions are worse, project completion is likely to be delayed further.

Small Surplus in 2026: Under this scenario, we project the general government budget surplus (including investment income) to narrow in 2026 to 0.3% of GDP, from 2.8% in 2025, reflecting a mix of lower hydrocarbon revenue and higher spending in order to mitigate the impact of weak tourism, travel and risk perception on the non-oil economy as well as military spending. Funding needs (general government budget, excluding Qatar Investment Authority's (QIA) estimated investment income) will reach 3.8% of GDP.

Under our baseline scenario, we project the general government budget surplus to rise in 2027, to 4.1% of GDP and over 7% by 2030 as LNG production increases. We project the budget balance excluding investment income to be in surplus from 2027 and Qatar to transfer most its surpluses to QIA for investment abroad.

Debt to Rise: We expect Qatar to cover its funding needs in 2026 through a mix of central bank overdrafts, domestic and global market sources and drawdown on the Ministry of Finance's deposits in the banking sector. We project debt to rise to 54% of GDP in 2026, above the forecast 'AA' median of 49.3%, before edging down due to strong nominal GDP growth.

Foreign Assets Backstop Funding: We estimate that sovereign net foreign assets (SNFA)/GDP rose to 227% (494 billion) in 2025 (QIA assets are not reported). In an adverse scenario of a much longer closure of the Strait or significant capital outflows, Qatar may call on some of QIA's assets as a backstop. A large share of QIA's assets can be liquidated at short notice. SNFA will rise due to fiscal surpluses until the end of the decade, although they remain vulnerable to financial market fluctuations. We project SNFA at USD532 billion (229% of GDP) at end-2027, assuming no stock market appreciation. This is well above the 'AA' median of 45.3% for 2025.

Gas Production to Boost Growth: We assume a contraction in economic growth in 2026 based on lower energy production and a significant slow-down in non-oil activity, in particular transport and tourism. North Field projects will support both hydrocarbon and non-hydrocarbon growth over 2027-2030, and we project GDP growth of over 10% in 2027.

Net External Creditor: We estimate that Qatar's economy is a net external creditor at 17% of GDP at end-2025 (total net asset positions are much stronger given our estimate of QIA's equity holdings). This position will strengthen in the medium term with lower borrowing and more foreign investment exports. We project the current account to remain in surplus in 2026 at 6.5% of GDP, returning to above 11% from 2027.

Banks Represent Contingent Liability: Qatar's banking sector is large, with assets of 273% of GDP and net foreign liabilities of over USD120 billion (55% of GDP) in 2025. Qatar remains vulnerable to a reversal of capital flows, with most of those liabilities short term. We have not seen evidence of material outflows since the onset of the war, and external funding has been resilient during previous shocks. In case of a surge in outflows, Qatar is likely to support the banking sector with FX liquidity, possibly by repatriating some of QIA's assets.

ESG - Governance: Qatar has an ESG Relevance Score (RS) of '5[+]' for both Political Stability and Rights and for the Rule of Law, Institutional and Regulatory Quality and Control of Corruption. Theses scores reflect the high weight that the World Bank Governance Indicators (WBGI) have in our proprietary Sovereign Rating Model. Qatar has a medium WBGI ranking at the 69th percentile.

RATING SENSITIVITIES

Factors that Could, Individually or Collectively, Lead to Negative Rating Action/Downgrade

- Public and External Finances: A prolonged disruption to production and transport of hydrocarbons that leads to a large deterioration of the sovereign balance sheet

- Structural features: Persistently higher geopolitical tensions that damage economic and financial stability

- Public and External Finances: A deterioration in Qatar's sovereign balance sheet, for example, due to renewed increases in net external debt, pressure on non-resident funding for banks or crystallisation of contingent liabilities

Factors that Could, Individually or Collectively, Lead to Positive Rating Action/Upgrade

- Structural Features: Improvement in structural factors such as reduction in hydrocarbon dependence and a strengthening in governance, and a significant reduction in geopolitical risk while maintaining strong fiscal and external balance sheets

SOVEREIGN RATING MODEL (SRM) AND QUALITATIVE OVERLAY (QO)

Fitch's proprietary SRM assigns Qatar a score equivalent to a rating of 'AA-' on the LTFC IDR scale.

Fitch's sovereign rating committee adjusted the output from the SRM to arrive at the final LTFC IDR by applying its QO, relative to SRM data and output, as follows:

- Public Finances: +1 notch, to reflect that compared to the SRM score, Qatar has large usable public sector assets, a flexible spending structure and a declining fiscal breakeven oil price.

Fitch's SRM is the agency's proprietary multiple regression rating model that employs 18 variables based on three-year centred averages, including one year of forecasts, to produce a score equivalent to a LTFC IDR. Fitch's QO is a forward-looking qualitative framework designed to allow for adjustment to the SRM output to assign the final rating, reflecting factors within our criteria that are not fully quantifiable and/or not fully reflected in the SRM.

DEBT INSTRUMENTS: KEY RATING DRIVERS

Senior Unsecured Debt Equalised: The senior unsecured long-term debt ratings are equalised with the applicable LT IDR, as Fitch assumes recoveries will be 'average' when the sovereign's LT IDR is 'BB-' and above. No Recovery Ratings are assigned at this rating level.

COUNTRY CEILING

The Country Ceiling for Qatar is 'AA+', one notch above the LTFC IDR. This reflects moderate constraints and incentives, relative to the IDR, against capital or exchange controls being imposed that would prevent or significantly impede the private sector from converting local currency into FC and transferring the proceeds to non-resident creditors to service debt payments.

Fitch's Country Ceiling Model produced a starting point uplift of +1 notch above the IDR. Fitch's rating committee did not apply a qualitative adjustment to the model result.

REFERENCES FOR SUBSTANTIALLY MATERIAL SOURCE CITED AS KEY DRIVER OF RATING

The principal sources of information used in the analysis are described in the Applicable Criteria.

The following limitations were identified and addressed:

QIA's assets are not officially reported by the government.

Fitch estimates these assets by compounding the government's transfers into QIA, using assumptions about returns and asset allocations that are informed by discussions with QIA. Fitch benchmarks government transfers into QIA against the balance of payments.

Fitch considered the data used sufficient for rating purposes because it expects that the margin of error related to the estimates would not be material to the rating analysis.

CLIMATE VULNERABILITY SIGNALS

The results of our Climate.VS screener did not indicate an elevated risk for Qatar.

ESG CONSIDERATIONS

Qatar has an ESG Relevance Score of '5[+]' for Political Stability and Rights as World Bank Governance Indicators have the highest weight in Fitch's Sovereign Rating Model and is therefore highly relevant to the rating and a key rating driver with a high weight. As Qatar has a percentile rank above 50 for the respective Governance Indicator, this has a positive impact on the credit profile.

Qatar has an ESG Relevance Score of '5[+]' for Rule of Law, Inst. & Reg. Quality and Control of Corruption as World Bank Governance Indicators have the highest weight in Fitch's Sovereign Rating Model and is therefore highly relevant to the rating and a key rating driver with a high weight. As Qatar has a percentile rank above 50 for the respective Governance Indicator, this has a positive impact on the credit profile.

Qatar has an ESG Relevance Score of '4' for Human Rights and Political Freedoms as the Voice and Accountability pillar of the World Bank Governance Indicators is relevant to the rating and a rating driver. As Qatar has a percentile rank below 50 for the respective Governance Indicator, this has a negative impact on the credit profile.

Qatar has an ESG Relevance Score of '4[+]' for Creditor Rights as willingness to service and repay debt is relevant to the rating and a rating driver, as for all sovereigns. As Qatar has track record of 20+ years without a restructuring of public debt and captured in our SRM variable, this has a positive impact on the credit profile.

The highest level of ESG credit relevance is a score of '3', unless otherwise disclosed in this section. A score of '3' means ESG issues are credit neutral or have only a minimal credit impact on the entity, either due to their nature or the way in which they are being managed by the entity. Fitch's ESG Relevance Scores are not inputs in the rating process; they are an observation on the relevance and materiality of ESG factors in the rating decision. For more information on Fitch's ESG Relevance Scores, visit www.fitchratings.com/topics/esg/products#esg-relevance-scores

VIEW ADDITIONAL RATING DETAILS

Additional information is available on www.fitchratings.com

PARTICIPATION STATUS

The rated entity (and/or its agents) or, in the case of structured finance, one or more of the transaction parties participated in the rating process except that the following issuer(s), if any, did not participate in the rating process, or provide additional information, beyond the issuer’s available public disclosure.

APPLICABLE CRITERIA

- Country Ceiling Criteria (pub. 24 Jul 2023)

- Sovereign Rating Criteria (pub. 15 Sep 2025)(including rating assumption sensitivity)

- Sukuk Rating Criteria (pub. 14 Oct 2025)

APPLICABLE MODELS

Numbers in parentheses accompanying applicable model(s) contain hyperlinks to criteria providing description of model(s).

· Country Ceiling Model, v2.0.3 (1)

- Debt Dynamics Model, v1.3.3 (1)

- Macro-Prudential Indicator Model, v1.5.0 (1)

- Sovereign Climate Risk Model, v1.0.0 (1)

- Sovereign Rating Model, v3.14.4 (1)

ADDITIONAL DISCLOSURES

- Dodd-Frank Rating Information Disclosure Form

- Solicitation Status

- Endorsement Policy

ENDORSEMENT STATUS

| Global Sukuk Ventures (Q.P.J.S.C.) | UK Issued, EU Endorsed |

| Qatar | UK Issued, EU Endorsed |

DISCLAIMER & DISCLOSURES

All Fitch Ratings (Fitch) credit ratings are subject to certain limitations and disclaimers. Please read these limitations and disclaimers by following this link: https://www.fitchratings.com/understandingcreditratings. In addition, the following https://www.fitchratings.com/rating-definitions-document details Fitch's rating definitions for each rating s

READ MORE

SOLICITATION STATUS

The ratings above were solicited and assigned or maintained by Fitch at the request of the rated entity/issuer or a related third party. Any exceptions follow below.

Fitch's solicitation status policy can be found atwww.fitchratings.com/ethics.

ENDORSEMENT POLICY

Fitch’s international credit ratings produced outside the EU or the UK, as the case may be, are endorsed for use by regulated entities within the EU or the UK, respectively, for regulatory purposes, pursuant to the terms of the EU CRA Regulation or the UK Credit Rating Agencies (Amendment etc.) (EU Exit) Regulations 2019, as the case may be. Fitch’s approach to endorsement in the EU and the UK can be found on Fitch’s Regulatory Affairs page on Fitch’s website. The endorsement status of international credit ratings is provided within the entity summary page for each rated entity and in the transaction detail pages for structured finance transactions on the Fitch website. These disclosures are updated on a daily basis.

Confidentiality Notice: The information contained in this e-mail and any attachment(s) is confidential and for the use of the addressee(s) only. If you are not the intended recipient of this e-mail, do not duplicate or redistribute it by any means. Please delete this e-mail and any attachment(s) and notify us immediately. Unauthorized use, reliance, disclosure or copying of the contents of this e-mail and any attachment(s), or any similar action, is strictly prohibited. Fitch Ratings reserves the right, to the extent permitted by applicable law, to retain, monitor and intercept e-mail messages both to and from its systems.