PHOTO

Abu Dhabi: – The Federal Tax Authority (“FTA”) has called again for registrants to benefit from Cabinet Decision No. 49 of 2021 on Amending Provisions of Cabinet Decision No. 40 of 2017 on the Administrative Penalties for Violation of Tax Laws in the UAE. The Decision came into effect on June 28, 2021, and includes reductions on administrative penalties to help taxpayers meet their obligations.

The FTA asserted that the Cabinet Decision would boost the UAE’s global business competitiveness by establishing a tax legislation environment that encourages self-compliance and offers significant support to the national economy. The Decision outlines 16 types of administrative penalties that have either been reduced or had the method of calculation amended. The amendments include administrative violations related to the application of Federal Law No. 7 of 2017 on Tax Procedures, Federal Decree-Law No. 7 of 2017 on Excise Tax, and Federal Decree-Law No. 8 of 2017 on Value Added Tax.

As part of its ongoing awareness-raising efforts, the FTA launched an awareness campaign last May. The FTA’s representatives communicated with the business sector to introduce the mechanism for implementing the new Decision, the facilities it offers registrants, how to benefit from these facilities, and the conditions required to benefit from the redetermination of administrative penalties imposed on registrants to equal 30% of the total unpaid penalties.

In a press statement issued today, the FTA outlined a set of conditions that need to be met in order to benefit from the redetermination of penalties. First, the administrative penalty must have been imposed under Cabinet Decision No. 40 of 2017 before June 28, 2021, and that the administrative penalty due were not settled in full until June 27, 2021. Furthermore, the registrant should settle all due payable tax by December 31, 2021, and settle 30% of the total unsettled administrative penalties imposed before June 28, 2021, no later than December 31, 2021.

The FTA indicated that, should the registrant meet all these conditions, the administrative penalties will be redetermined to equal 30% of the total unpaid penalties that will appear on the FTA’s electronic system after December 31, 2021.

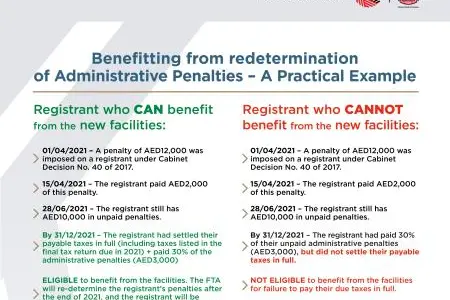

Example on How to Benefit from the New Facilities

To help registrants benefit from the new Decision, the FTA presented a practical example featuring two cases: one where the registrant qualifies for redetermination, and another where they don’t.

The first case (a qualified registrant for redetermination):

- A penalty of AED12,000 was imposed on a registrant on April 1, 2021, under Cabinet Decision No. 40 of 2017.

- The registrant paid AED2,000 of this penalty on April 15, 2021.

- The registrant still has AED10,000 in unpaid penalties on 28 June 2021.

- By December 31, 2021, the registrant had settled their payable taxes in full, including taxes listed in the final tax return due in 2021. The registrant also had paid 30% of the administrative penalties (i.e. AED3,000) before December 31, 2021.

- In this case, the registrant is eligible to benefit from the redetermination, and the FTA will re-determine their penalties after the end of 2021. The registrant will be exempted from paying the remaining AED7,000 in administrative penalties.

The second case (a registrant not qualified for redetermination ):

- A penalty of AED12,000 was imposed on a registrant on April 1, 2021, under Cabinet Decision No. 40 of 2017.

- The registrant paid AED2,000 of this fine on April 15, 2021.

- The registrant still has AED10,000 in unpaid penalties on 28 June 2021.

- By December 31, 2021, the registrant had paid 30% of the unpaid administrative penalties (AED3,000), but did not settled their payable taxes in full.

- In this case, the registrant is not eligible to benefit from the Decision for failure to pay their due taxes in full.

The FTA urged registrants to use the “Payment Adjustment Type” feature when settling their due payments on the FTA’s e-Services portal. The feature allows taxpayers to allocate the amounts based on their payment preferences. The options available are either to pay tax first, or administrative penalties first, or by oldest liability. In order to benefit from the redetermination of penalties, registrants should re-consider the accurate selection of these options in order to achieve the intended payment allocation results.

Registrants are highly encouraged to ensure that the tax return or the voluntary disclosure is submitted before making the payment. If the registrant made the payment before filing the tax return or submitting the voluntary disclosure, and they had outstanding administrative penalties in their account, the system will settle the payable administrative penalties first, since there is no outstanding payable tax in their account at the time of making the payment.

The FTA also clarified that it is essential for taxable persons to pay their due payable tax before the due date to avoid any late payment penalties. In the same regard, the FTA clarified that bank transfers can take two or three working days to process the payment; hence, the period must be taken into consideration to ensure that FTA receives the payment before the due date.

The FTA issued two public clarifications on Cabinet Decision No. 49 of 2021, which is available on FTA’s website. The first public clarification details the amendments to administrative penalties and violations related to the application of Federal Law No. 7 of 2017 on Tax Procedures, in order to ensure certainty regarding the application of the amended penalties. The second public clarification details information about the mechanism used to re-determine certain administrative penalties that were imposed before June 28, 2021.

-End-

The Federal Tax Authority was established by Federal Decree-Law No. (13) of 2016 to help diversify the national economy and increase non-oil revenues in the UAE through the management and collection of federal taxes based on international best practices and standards, as well as to provide all means of support to enable taxpayers to comply with the tax laws and procedures. Since its inception in 2017, the FTA has been committed to cooperating with the competent authorities to establish a comprehensive and balanced system to make the UAE one of the first countries in the world to implement a fully electronic tax system that encourages voluntary compliance, with simple procedures based on the highest standards of transparency and accuracy – beginning from registration, to the submission of tax returns, to the payment of due taxes through the Authority’s website: www.tax.gov.ae

© Press Release 2021

Disclaimer: The contents of this press release was provided from an external third party provider. This website is not responsible for, and does not control, such external content. This content is provided on an “as is” and “as available” basis and has not been edited in any way. Neither this website nor our affiliates guarantee the accuracy of or endorse the views or opinions expressed in this press release.

The press release is provided for informational purposes only. The content does not provide tax, legal or investment advice or opinion regarding the suitability, value or profitability of any particular security, portfolio or investment strategy. Neither this website nor our affiliates shall be liable for any errors or inaccuracies in the content, or for any actions taken by you in reliance thereon. You expressly agree that your use of the information within this article is at your sole risk.

To the fullest extent permitted by applicable law, this website, its parent company, its subsidiaries, its affiliates and the respective shareholders, directors, officers, employees, agents, advertisers, content providers and licensors will not be liable (jointly or severally) to you for any direct, indirect, consequential, special, incidental, punitive or exemplary damages, including without limitation, lost profits, lost savings and lost revenues, whether in negligence, tort, contract or any other theory of liability, even if the parties have been advised of the possibility or could have foreseen any such damages.