PHOTO

Dubai — The supply of under construction warehouse stock in Dubai’s industrial market stands at just 1.56 million square feet according to Knight Frank's latest report: Dubai & Abu Dhabi Industrial Markets Review, Q3, 2023.

According to Knight Frank, demand is outstripping supply and occupiers are faced with the prospect of leasing more secondary stock, while others are gravitating towards locations in Abu Dhabi, which is benefitting from spillover demand.

Indeed, across t the six primary submarkets tracked by Knight Frank in Abu Dhabi, rents have remained unchanged thus far during H2. Notably, high occupancy levels in KEZAD and Masdar have helped to sustain rents.

Knight Frank also reports a rise in demand in ADAFZ, where space is available for AED 600 per square metre. To cater to burgeoning demand, ADAFZ is developing a new masterplan, Al Falah Free Zone, spanning over 6 square kilometres, which will include both bonded and non-bonded zones.

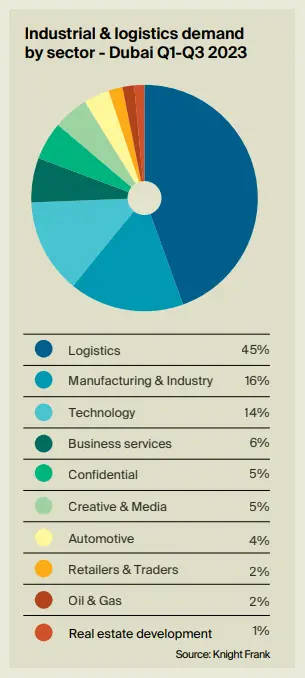

SOURCES OF DEMAND

Dubai recorded 9.9 million square feet of new requirements during Q1-Q3 2023, according to Knight Frank. The logistics sector dominates Dubai's demand, accounting for 44% of new requirements, followed by the manufacturing & industry (16%) and technology sectors (13%).

In Abu Dhabi, new industrial and logistics space requirements grew to 350,000 square metres during the first nine months of 2023, a significant 94% increase on the same period in 2022.

Maxim Talmatchi, Associate Partner, Co-Head of Industrial and Logistics says: “Demand has been strong this year and we have worked with several new market entrants from Asia Pacific, CIS countries, Turkey, and India. Additionally, existing industrial occupiers have also been busy expanding their footprints in Dubai.

This growing pool of demand has prompted both local and international developers to explore opportunities to enter the market with Grade A logistics build-to-rent products. We expect approximately 9-10 million square feet of Grade A logistics warehousing to be delivered in the next 10 years.”

Knight Frank’s report also highlights that while warehouse lease rates in Dubai have remained stable thus far during H2 2023, Grade B rents in JAFZA (AED 25 per square foot) and Dubai Industrial City (AED 32 per square foot) have risen by 25% and 19%, when compared to the same period last year. Similarly, Al Quoz (Grade A), has seen rents climb to 52% above January 2020 levels, marking it as the most expensive warehouse leasing location in Dubai.

Faisal Durrani, Partner – Head of Research, MENA, commented: “The transformation of Al Quoz continues. With lease rates here at AED 58 per square foot, retailers, many of whom are fitness and wellness businesses, cafes and art galleries are continuing to snap up warehouses for use as retail premises, adding to the boho vibe that has become entrenched in this part of the city.

“For industrial occupiers, Al Quoz’s central location between old and new Dubai continues to fuel demand, especially among occupiers from the logistics (last-mile centres) and automotive sectors. The transition of stock from warehousing to retail from this core location will undoubtedly continue driving up rents here, particularly when the wider market for light industrial units has occupancy levels hovering at around 98% and supply is so restricted.”

OUTLOOK

According to Knight Frank, Dubai is experiencing a significant influx of institutional investments from the United States, influenced by the UAE's strategic location, e-commerce growth, and the need for efficient supply chain solutions. Yet, Dubai faces a shortage of prime industrial and logistics land, highlighting the importance of expansion plans by authorities such as DIP and JAFZA.

Knight Frank projects that Dubai's industrial rents will maintain their upward trajectory. The acute supply shortage, combined with Dubai's ambitious D33 Economic Agenda and Vision 2040 Strategy underpins Knight Frank’s outlook.

Adam Wynne, Associate Partner, Co-Head of Industrial & Logistics UAE concluded: “Over the next 12-16 months as the market continues to evolve, we predict that the gap between primary and secondary rents in the industrial and logistics sector will widen. Tenants remain laser-focused on securing best-in-class, internationally specified warehousing and are now willing to pay a premium to occupy such space, which historically was not the case.

“Given the restricted supply entering the market, landlords who are willing to invest capital expenditure to modify or retrofit their aging assets will be able to command a rental premium. In contrast, landlords of secondary assets may be able to maintain occupancies in the short term; however, when the new stock does eventually materialise, older assets will likely experience falling rents and increased voids.”

Knight Frank also highlights a key risk to the market: Heightened investor demand is boosting capital values faster than lease rates, which is compressing yields. Knight Frank forecasts yields will have slipped from about 8.50- 8.75% in H1 to around 8.0-8.25% by the end of 2023.

In addition, interest rate hikes could dampen demand for industrial assets, due to the increased cost of debt. This could slow, or even reverse yield compression.

About Knight Frank:

Knight Frank LLP is the leading independent global property consultancy. Headquartered in London, the Knight Frank network has 487 offices across 53 territories and more than 20,000 people. The Group advises clients ranging from individual owners and buyers to major developers, investors, and corporate tenants. For further information about the Firm, please visit www.knightfrank.com.

In the MENA region, we have strategically positioned offices in key countries such as the United Arab Emirates, Saudi Arabia, Bahrain, Qatar, and Egypt. For the past 13 years, we have been offering integrated residential and commercial real estate services, including transactional support, consultancy, and management.

Understanding the unique intricacies of local markets is at the core of what we do, we blend this understanding with our global resources to provide you with tailored solutions that meet your specific needs. At Knight Frank, excellence, innovation, and a genuine focus on our clients drive everything we do. We are not just consultants; we are trusted partners in property ready to support you on your real estate journey, no matter the scale of your endeavour.

Let's connect socially - find us on LinkedIn, Instagram, and Twitter. For more information and to explore how we can be your partners in property, please visit our website at www.knightfrank.ae

For all Media and PR inquiries, please contact: Roksar Kamal, Press Manager, on Roksar.kamal@me.knightfrank.com

Other highlights:

- The UAE's industrial and logistics market is flourishing, driven by strong demand from several sectors, including automotive, e-commerce (logistics), ‘click and mortar’ retailers, manufacturing, and technology.

- Tenants remain laser-focused on securing best-in-class, internationally specified warehousing and are now willing to pay a premium to occupy such space. This is likely to lead to a widening gap between primary and secondary rents over the next 12 months.

- The Comprehensive Economic Partnership Agreement (CEPA) has boosted trade and investment between the UAE and India, making it cheaper for UAE-based industrial companies to import and export goods, and easier for them to invest in India.