PHOTO

The economic recovery in the GCC states will accelerate in 2022 as the third wave of the pandemic recedes. However, a steady recovery is not expected if the GCC population remains susceptible to the virus and its mutations, the Institute of International Finance (IIF) said in a research report.

The IIF expects the GCC to grow 1.7 percent in 2021 and 4.2 percent in 2022. High-frequency indicators, including PMI and

credit to the private sector, point to strong private sector recover in Saudi Arabia and Qatar, it said.

"Hydrocarbon real GDP growth is projected at 5 percent in 2022 on the assumption that the OPEC+ production cuts end by mid-2022. Risks are broadly balanced. On the upside, faster vaccination rates and further progress in reforms could boost

non-hydrocarbon growth in 2022," Garbis Iradian, IIF Chief Economist, MENA, and Samuel LaRussa, a senior research analyst, stated in a report.

A slow vaccine rollout or new restrictions by the GCC states in response to an increase in coronavirus cases could trigger downside risks.

The IIF expects that central banks in the Gulf states will leave their policy rates unchanged through end-2022 as they track US rates in the context of the peg to the US dollar.

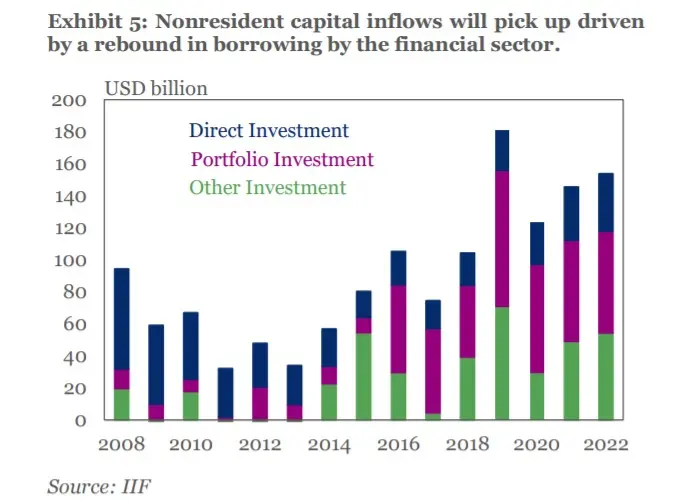

According to available data from the IIF, non-resident capital inflows will rise from $123 billion in 2020 to $148 billion in 2021.

The GCC states have raised a combined $95 billion in the international market so far. The region's Eurobond issuance peaked at $111bn in 2020 and was dominated by sovereign and quasi-sovereign issuances, IIF said.

The global association of the financial industry projects average CPI inflation to increase from around 1 percent in 2020 to 2.3 percent in 2021, driven by higher food and gasoline prices.

The aggregated fiscal deficit could narrow from 8.5 percent of GDP in 2020 to around 1.0 percent in 2021, considering that brent oil prices will average at $67/bbl and by exercising modest fiscal consolidation, the IIF said.

It expects a surge in regional hydrocarbon revenue from $221 billion in 2020 to $326 billion in 2021.

The announced plans for fiscal adjustment in the coming years in Saudi Arabia, the UAE, Oman, and Qatar will put the fiscal position on sound footing over the medium-term even if oil prices resume their decline beyond 2021. However, stronger adjustment is needed in Bahrain to achieve fiscal sustainability, IIF noted.

Strong initial capital and liquidity positions will help the banking system to be resilient despite COVID-19.

According to IIF data, Tier 1 capital ratios exceeded 15 percent in the GCC states. NPLs to total loans were between 2 and 3 percent in Saudi Arabia, Qatar, and Kuwait, and 4 to 8 percent in Oman, Bahrain, and the UAE.

"Central banks in the region extended the deferred payment program until the end of June to support private sector financing. Once the forbearance is lifted, we could see a modest deterioration in asset quality,” the IIF economists noted.

“Profitability challenges in the low-interest rate environment may also limit banks’ ability or willingness to expand private sector credit at the same pace as in 2020,” they said.

(Reporting by Seban Scaria; editing by Daniel Luiz)

( seban.scaria@refinitiv.com )

Disclaimer: This article is provided for informational purposes only. The content does not provide tax, legal or investment advice or opinion regarding the suitability, value or profitability of any particular security, portfolio or investment strategy. Read our full disclaimer policy here.

© ZAWYA 2021