PHOTO

Global merger and acquisition activity has slumped since the start of the latest war in the Middle East and senior bankers said a number of deals have been paused. But they are optimistic that dealmaking will bounce back as corporates have become more accustomed to geopolitical bumps. Bankers said corporate bosses are also assessing changing deal structures to reduce risks.

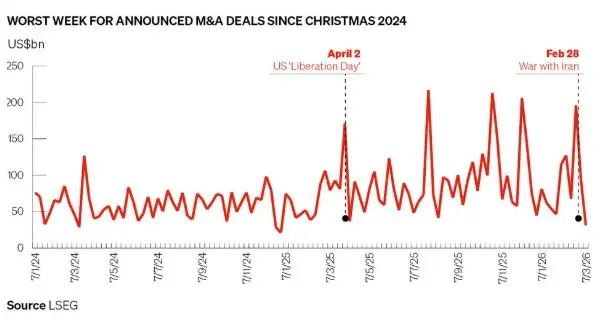

The US/Israel war with Iran started on February 28. M&A activity had been buoyant through February and in the week commencing February 22 the volume of global announced M&A hit US$196bn, the fourth best week since the start of 2024. In the week of March 1 volume fell to US$94.2bn – still a decent level – but in the week of March 8 it slumped to US$31.1bn, down 84% from the week before the war and the lowest weekly tally since Christmas week in 2024, according to LSEG data.

For the period March 1–18 2026, announced M&A activity totalled US$167.3bn, down 31% from the same period in the previous year and down 17% from the average of the previous five years for the same period, the data showed.

M&A data can be notoriously lumpy, but several top M&A bankers told IFR that deals had been paused, though not pulled. One said his firm had planned to announce a few deals this month, but had delayed those announcements.

Bankers said deal pipelines are still full, but how many and when deals land will clearly depend on the duration and scale of the war and its impact on energy prices and inflation – and that is far from clear.

Several said the lesson of past crises is not to halt work and to try to keep processes on the move.

“You don’t advise clients to stop, park the car in the garage and lock it up. You keep driving and pump the brakes as needed,” said Andrew Woeber, global head of M&A at Barclays.

Amending deals

Bankers said there are options to amend deals or introduce elements to get them over the line in more volatile times.

Financing is a key issue. One banker said buyers might seek more flexible financings, which could include adding floating-rate notes, shorter durations or increased currency and/or interest rate hedges – perhaps the hedge exposure increases to 70%, rather than 30%, for instance.

“It may cost a little more, but it can be a case of managing risks with a slightly different attitude,” he said.

Buyers may also opt to put in more equity so if bumps emerge there’s more cushion to ride them out. These measures can affect returns, but a return on investment of 9% rather than 11% may be acceptable if the payoff is reduced risk.

Bankers said, as ever, specific deal or client situations will dictate whether to pause or not.

Aside from financing appetite, deals could now require extra due diligence to address how supply chains might be affected by a prolonged war or energy market disruption.

One option on deals is the use of contingent value rights, or CVRs, and Barclays’ Woeber said the more frequent use of CVRs is an example of a creative solution to address uncertainty. They are not common, and there have typically only been one to three deals using them each year, but there were an estimated 30 last year as geopolitical risks elevated.

A CVR is a contractual right given to shareholders of a target company, promising additional cash or stock if specific future milestones are met after a deal closes, and can be useful to bridge valuation gaps, especially in volatile times. Milestones can include regulatory approvals, revenue targets or clinical trial success for drug companies. Pfizer included CVRs in its acquisition of Metsera in November, based on achieving three clinical and regulatory milestones, which could lift the purchase price to about US$10bn from US$7.6bn.

The new normal?

M&A bankers said although deals will get scrapped if there is a prolonged war and/or elevated energy prices, there could be some offset as opportunities emerge from market dislocations, such as after the global financial crisis, and even after US president Donald Trump announced sudden import tariffs on April 2 2025.

In the five weeks before "liberation day", global announced M&A averaged US$106bn per week, but in the five weeks after that, weekly activity fell to US$66bn on average, LSEG data showed.

But one banker said while the tariff announcements scuttled deals, there were later opportunities when European and Asian firms looked at US acquisitions as they reworked their supply chains.

Bankers also said that some CEOs, rather than seeing the tricky times as a reason to avoid deals, think instead it is more important to push forward. Whether that is raising money in order to be liquid amid the turmoil, or buying struggling rivals to increase the chance of being one of the survivors. “Scale is going to matter more than ever,” one senior banker said.

Another banker agreed on the importance of scale, and said despite the geopolitical headwinds, other supportive factors are likely to keep dealflow alive, including an “abundance” of finance from public and private sources, inflation that has been tamer than expected, interest rates that remain moderate, and better engagement with regulators.

Corporate chiefs also appear to have more appetite to ride through bumps and persist with a deal than before the Covid-19 crisis. Many bosses and boards now regard heightened geopolitical risk as normalised and are keen to push through if they can manage and mitigate the biggest risks, several bankers said. They noted that deal activity snapped back from liberation day far quicker and stronger than many had expected.

“Companies really see a strategic imperative to be bigger and global and they need growth,” one banker said. “I think a lot of these transactions will survive the market disruption and volatility, and get done.”

Source: IFR