Large-scale projects spread across sectors - from real estate and infrastructure to petrochemicals - have ensured a high demand for base metals such as steel and copper in the GCC, says a new Standard Chartered report.

Emirates 24|7

September 28, 2009

28 September 2009 Large-scale projects spread across sectors - from real estate and infrastructure to petrochemicals - have ensured a high demand for base metals such as steel and copper in the GCC, says a new Standard Chartered report.

Terming the demand for base metals as crucial for the global commodities market, the report said the GCC is "an important pillar" in the long-term structural bull story for metals.

"Projects in the GCC merit attention due to their nature as metals-intensive schemes, and the fact that they are bankrolled by substantial state reserves. As a result, they are less sensitive to the downturn in private sector activity. The various projects encompass infrastructure, construction and petrochemical industries, all large users of steel and base metals," analysts David Barclay and Shady Shaher wrote in their report. "While GCC econ-omies are slowing, governments are employing countercyclical fiscal policies in which infrastructure investment is at the forefront. As well as helping to pick up some of the slack in their economies, it should also improve productivity over the medium term, leading to more sustainable rates of growth in the future."

Although their impact on global demand pales in comparison with China, GCC metals demand growth rates were among the world's highest in 2004-08, Barclay and Shaher pointed out.

The analysts, who wrote in detail about the GCC's investment plans over the next few years, said, "the projects will play an important role in the expansion of raw materials' consumption growth within emerging markets. This should help support prices during a period of anaemic demand growth from the OECD countries."

GCC projects are especially driving demand for steel and copper, said the report. In what was earlier an attempt to meet its own rising demand for aluminium, the region's oil producers set up several aluminium smelting units. However, the region is now on its way to become a powerhouse for aluminium production and will meet 20 per cent of the global demand by 2020. (It currently meets five per cent). During the past several years, most GCC investment was directed at the real estate sector. This trend is expected to continue in the coming years.

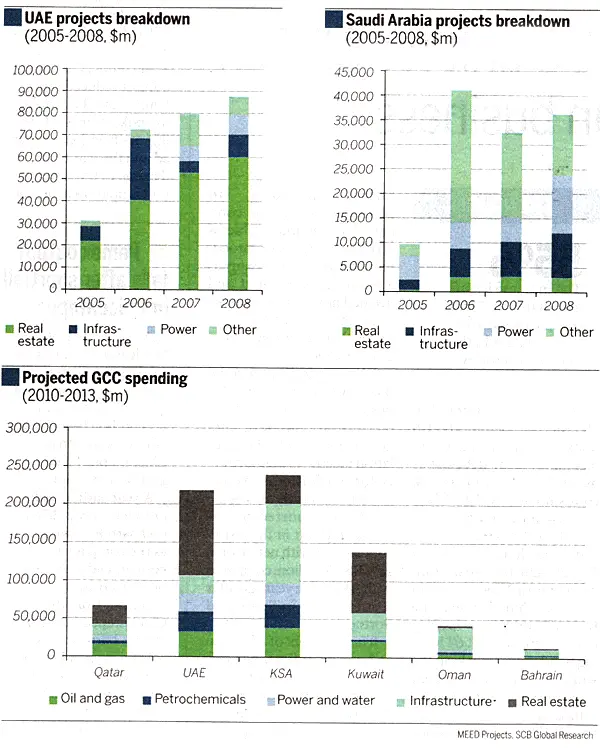

Real estate main mover As for as the planned projects from 2010 to 2013 in the GCC, it appears that real estate will continue to dominate, said the analysts. "Real estate accounts for $250 billion [Dh918bn] of planned projects, or more than one-third of the total $717bn for all categories in the region," they wrote.

This is particularly the case in the UAE, with $110bn of planned real estate projects. However, given the downturn in the real estate sector, many of these projects will be put on hold or delayed, pending a pickup in market demand, they said.

"We estimate that 70 per cent of the value of awarded contracts in 2008 in the UAE was in real estate. That year was dominated by ample liquidity and excessive moves in real estate prices. Given that the housing market is undergoing a correction, there is an opportunity for the UAE to refocus its investment on productive sectors of the economy - such as ports, education, petrochemicals, financial services, and tourism - that are likely to have a more sustained impact on the economy."

Infrastructure schemes The Standard Chartered analysts estimate that infrastructure projects in the GCC will reach $205bn by 2013, with Saudi Arabia having the lion's share at $105bn. Infrastructure projects (including hospitals, roads, railways, and airports) in the GCC are almost exclusively government driven, and largely fall under the government's fiscal expansionary spending outlays and wider socio-economic programmes.

"In Dubai, for example, the state budget has set aside close to 40 per cent for expansion and development of the transportation network. In Saudi Arabia, the government's decision to take over a number of key infrastructure projects that ran into funding problems has resulted in these projects moving ahead very rapidly," said the analysts. "We believe GCC governments will continue to support projects deemed beneficial to the wider social and economic interests of the state. Thus, infrastructure projects are likely to underpin regional demand for both base metals and steel, despite potential weakness in private sector real estate."

Barclay and Shaher said Dubai Metro, Abu Dhabi Metro (on the cards), Qatar's Mesaieed Port, Saudi Arabia's Haramain High-Speed Rail Network and Kuwait City Metro (planned) are the prominent infrastructure projects in the region.

Power and water projects Power and water projects in the GCC are largely carried out by quasi-government entities, and these projects are seen as a high priority, as the additional capacity is urgently required to address the region's growing young population, said the report.

"Demographic trends are a key structural driver in the GCC. The Saudi Ministry of Planning and Economy forecasts the population will reach 33 million by 2020, requiring increased power and water projects to cater for this and for urban/industrial expansion," it said.

Annual GCC electricity demand is expected to grow by 10 per cent and desalination demand by eight per cent until 2015 (World Nuclear Association). The GCC intends to spend close to $70bn in the next four years to expand existing facilities and create new capacity, the analysts reported. "Saudi Arabia alone is planning to add close to 14,560MW of power capacity and we estimate the kingdom will spend close to $27.7bn over the next three years building power and water projects. Despite pressing ahead with many of the planned projects, the global economic slowdown will reduce the pressure on countries to bring power online quickly," the analysts wrote.

The report cited Abu Dhabi's Shuweihat 2 Plant; Saudi Arabia's Marafiq-Jubail plant and the Rabigh independent power project; Qatar's Ras Girtas power project; Kuwait's Subiya power plant; and Bahrain Addur independent water and power project as prominent projects.

Fuelling commodities market Other projects that will be of significance to metals demand include those in the oil and gas and petrochemicals sectors, with $117bn and $67bn, respectively, in planned projects across the region until 2013. Saudi Arabia is planning close to $22.8bn in refinery-related spending in the sector.

"The decline in oil prices has dented expansion plans, with $29bn worth of projects put on hold. However, the sector continues to be relatively well-placed, as the windfalls of the past few years have kept state companies strong enough to pursue expansion and development works. Also, many of the region's oil firms are using the economic downturn to re-tender projects, from which they are able to extract substantial savings. The Abu Dhabi Company for Onshore Operations (Adco) awarded contracts for the Sahil, Asab and Shah (SAS) fields totalling $3.5bn in January, resulting in estimated savings of $1bn compared with earlier estimates," said the report.

The petrochemical sector is also expected to benefit from increased stability and capacity in the downstream sector. "We estimate that planned petrochemical projects will reach $67bn by 2013, with Saudi Arabia and the UAE leading with $30.4bn and $ 26.5bn, respectively," said the analysts.

"We believe governments will continue to support projects in the sector, given they have majority stakes in the major producers and because of the impact on employment. In the case of one Saudi producer alone, 85 per cent of the estimated 17,000 staff are Saudi nationals."

The report highlighted Abu Dhabi's SAS oilfield development, Saudi Arabia's Jubail petrochemicals complex, Saudi Aramco - Khursaniyah gas plant, Qatar QP/ExxonMobil - Ras Laffan olefins complex and Kuwait's Clean Fuel Project 2020.

Project funding Project finance for many of the large-scale projects in the GCC will continue to be challenged by tighter global liquidity conditions, Barclay and Shaher acknowledged.

"The Middle East was the world's largest project finance market only a couple of years ago. Of the major announced projects, Bahrain's Addur was the only project to raise funding ($ 2.1bn) in H1 2009. Signs of a slow recovery in the project finance market have begun to appear in the second half. In July, Saudi Arabia's ACWA Power completed financing for its $2.5bn Rabigh independent power project, with funding that includes a $1.9bn debt tranche committed for 20 years," said the report.

Activity on the bond front is also picking up, with very strong interest for bond offerings by state-affiliated Gulf entities. "Dolphin Energy successfully refinanced a $1.25bn bond issue, above initial guidance of a $750m tranche; Qatar's Ras Laffan LNG Company's $2.23bn bond generated orders of $17.5bn," said the report.

"Investors in the region are starting to appreciate the attractiveness of bonds as fund-raising instruments, and with bank liquidity tight both globally and regionally, have become a more feasible option for many of the large-scale project managers."

"Governments also appear to be willing to step in should funding on commercial terms prove difficult. Abu Dhabi's Shuweihat 2 power project is looking to raise $1.1bn for its $3.2bn project, and while 12 banks already have credit approval for the loan, the Abu Dhabi Water and Electricity Authority has said it will look at nationalising the project should commercial fundraising not be completed. In Saudi Arabia, the government is stepping in to fund a $ 7bn land bridge project. In April, it cancelled private sector involvement in the Ras Al Zour power plant and appointed a government entity.

In February 2008, the government converted the stalled Haramain rail link between Makkah and Madinah from a build-operate-transfer model to a public procurement scheme."

Impact on demand Copper wire-rod and related product demand in the GCC countries increased by an average of 19 per cent from 2004-08. Galvanised steel imports by the UAE rose by 72 per cent year-on-year in 2008 and by an average of 37 per cent from 2005-08.

Steel long product demand experienced a 41 per cent compound annual growth rate in the GCC between 2005 and 2008.