Global ad market has stabilised; prospects for 2010 and beyond improving

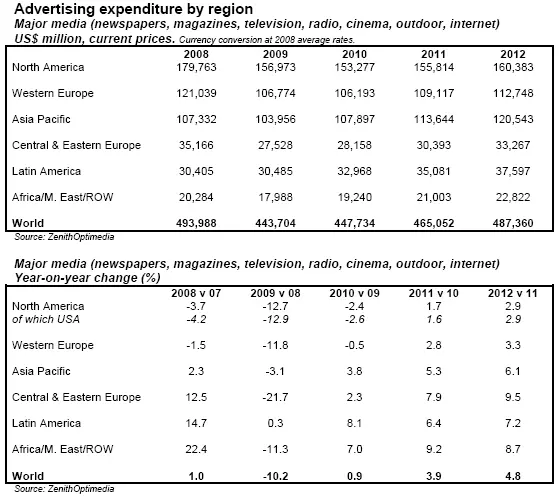

The worst recession since the Great Depression has caused an advertising downturn unprecedented in modern times. We estimate that global ad expenditure will have dropped 10.2% over the course of 2009.

Press Release

December 8, 2009

08 December 2009 After the worst decline in ad expenditure in modern times (-10.2%) in 2009, the world's ad market has now stabilised and will grow 0.9% in 2010. This is our first upgrade to 2010 for 18 months. As is usual after a downturn, the market will improve steadily over the next three years, reaching normal 5% growth in 2012. Paid-search to grow 15% in 2009, driving 9% growth in overall internet advertising. Internet's share of ad expenditure to rise from 12.4% in 2009 to 16.2% in 2012

The worst recession since the Great Depression has caused an advertising downturn unprecedented in modern times. We estimate that global ad expenditure will have dropped 10.2% over the course of 2009. It is normal for ad expenditure to exaggerate general economic trends: when the economy shrinks, ad expenditure shrinks faster, and by more. The corollary to this is that when recovery is complete, we can expect the ad market to outperform the economy as a whole.

The recovery will take some time. After reaching its lowest point during the last two recessions, the global ad market recovered progressively over the course of the next three years, and we expect the current downturn to follow this pattern. However, we have raised our forecasts for growth in 2010 by 0.4 percentage points to 0.9%. This is our first upgrade to 2010 since we published our forecasts in June 2008, just before the full extent of the financial crisis became clear and the advertising downturn began. We expect the recovery to strengthen steadily as corporate and consumer confidence continue to improve, with 3.9% growth in 2011 and 4.8% growth in 2012.

In some markets new regulations have exacerbated the downturn, or are likely to hinder recovery. In France the public television channels (which attract more than a third of all viewing) began to phase out their advertising at the beginning of 2009, and will be completely ad-free by 2011. In Spain the government plans to remove all advertising from the public channels (which attract more than a fifth of viewing) at the beginning of 2010, and in China the government will reduce the numbers of ads all channels are permitted to broadcast, again from the beginning of 2010. Reducing the supply of television ads will probably raise the price of the remaining airtime, but not by enough to compensate for the lower volume.

The pain inflicted by the ad downturn has been distributed across the globe very unevenly. All the developed markets (in North America, Western Europe and Japan) have suffered substantial losses, and we expect decline to continue in these markets in 2010 as economic growth remains slow and uncertain. We forecast ad expenditure to shrink 2.4% in North America, 0.5% in Western Europe and 3.2% in Japan, before mild growth returns in 2011.

Plenty of markets in the developing world - particularly in Asia Pacific and Latin America - have continued to grow this year, however, and are already picking up speed after a slowdown in the first half of 2009. We expect these regions to return to healthy growth in 2010. Many developing markets in Central & Eastern Europe and the rest of the world have suffered large shocks to their economies and ad markets. We think these shocks are one-off adjustments rather than deep-seated problems, and expect healthy growth next year here too. 27 developing markets have continued to grow during 2009, 12 of them at double-digit rates, and we forecast the number of growing ad markets - out of the 79 we cover - to increase to 63 next year. In 2010 we forecast ad expenditure to grow 8.4% in Asia Pacific (excluding Japan), 8.1% in Latin America, 2.3% in Central & Eastern Europe and 7.0% in the rest of the world.