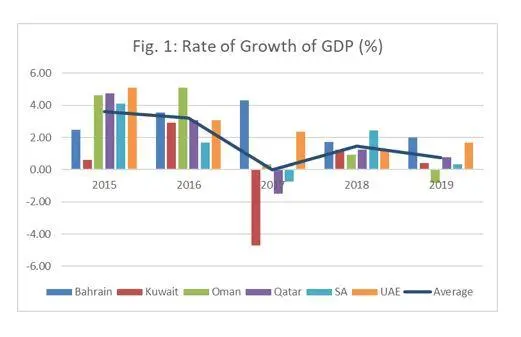

The impact of COVID-19 has been far-reaching and devastating in virtually all countries of the world. The countries in the GCC are no exception. Every country in the GCC has simultaneously experienced negative growth rate in 2020 and this has not happened ever before. The most number of countries that experienced negative growth rates at the same time was in 2009 in the aftermath of the Great Recession. These countries were Kuwait, Saudi Arabia (SA) and the UAE. For, at least, 25 years, the average rate of growth of GDP has never been negative for the GCC as a group till 2020. This should be sufficient to convey the fact that the impact of the COVID pandemic has been unprecedented. The timing of the COVID pandemic was especially unfortunate since the economies of the GCC had already been experiencing sluggish growth prior to the pandemic. After an average rate of growth of 3.6 percent in 2015, the GCC economies had perceptibly slowed down, as seen in Figure 1.

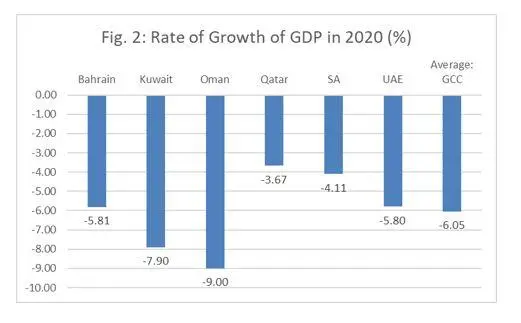

The line graph in Figure 1 shows the average rate of growth of GCC countries and the trend was clearly in the downward direction. Thus, the pandemic delievered a blow just when GCC economies were striving to recover from slow growth rates. Figure 2 shows how damaging the impact of the COVID pandemic has been.

Spread of COVID19

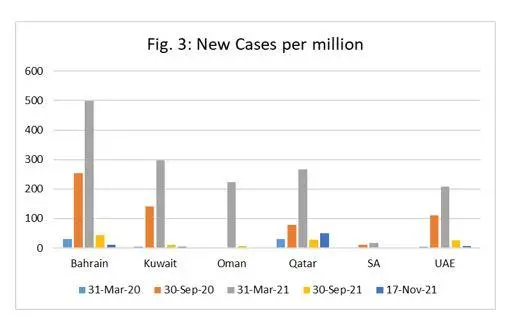

The reason for this massive decline in growth rates is not far to seek. The spread of COVID cases was very rapid all through 2020 and it is only after March 2021 that new cases have started to come down as seen in Figure 3.

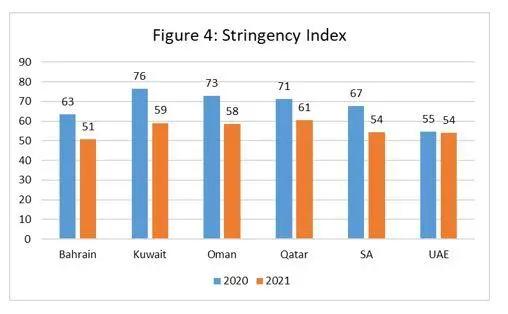

This was also the time that GCC countries imposed strict measures to control the spread of the disease. These measures, while they controlled the spread of the disease, unfortunately hurt the economies as well. The Stringency Index, developed by the Oxford University’s Blavatnik School of Government, tracks government measures that aim to stop the spread of the disease. The index values range from 0 to 100 with higher values indicating stronger government measures. Figure 4 shows the average values of the Stringency Index in the GCC countries during 2020 and 2021.

The average values do not show the full extent of the restrictive measures. For instance, the highest index value for Kuwait was 100 for some time. The highest values for other countries were 94 for Oman and Saudi Arabia, 90 for the UAE, 86 for Qatar and 79 for Bahrain. Figure 4 also shows that all governments have eased restrictions in 2021.

The Process of Recovery

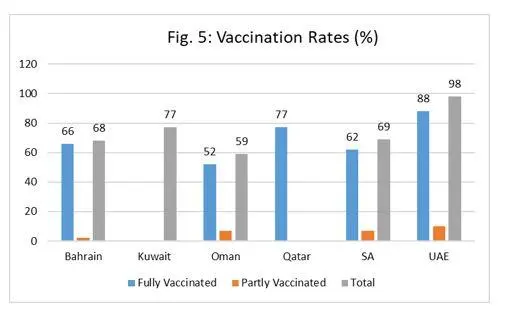

Rapid progress in vaccination rates has helped the GCC governments to open up and permit the resumption of economic activities. Figure 5 shows the progress of vaccinations.

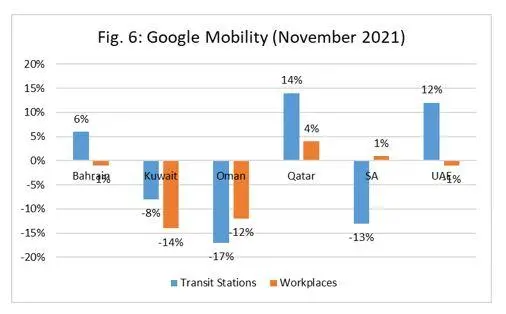

The progress in the UAE has been exemplary and this has allowed normal economic life to begin in full swing. An indication of how much normality has returned can be gleaned from the Google Mobility reports which compare current levels of activity in designated places (such as, grocery stores, parks, transit stations, workplaces, etc) with normal period activity before the onset of the pandemic. The percentage difference between current level of activity and activity in the pre-pandemic normal period is reported in Figure 6.

Qatar and UAE show the clearest signs of return to normality. In both the countries, the transport sector is running ahead of the levels reached just prior to the onset of the pandemic while as far as economic activity (as shown by workplaces) is concerned, UAE is almost at normal with Qatar exceeding levels achieved earlier.

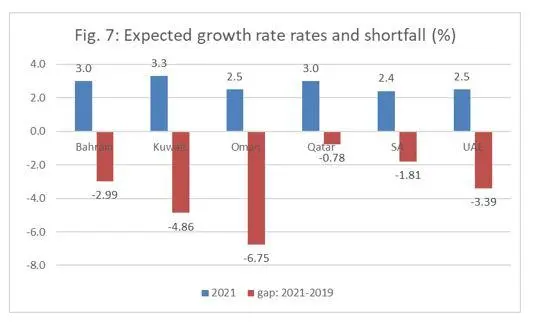

The battle against the pandenic was waged not only by restrictive measures. This was supported by timely stimulus packages that were implemented by all the countries. The stimulus packages were as high as 2.5 percent of the total GDP of GCC countries. The combination of the emergency health related packages and the stimulus packages has given hope that there might be a welcome return to positive growth rate in 2021. It should, however, be remembered that positive growth rate after a sharp fall in the previous year does not wipe out the signficant losses suffered. Figure 7 shows the expected growth rates for the next year. It also shows the gap or the shortfall between the expected GDP for 2021 relative to the level in 2019.

All GCC countries expect positive growth rates in 2021. However, despite this encouraging sign, it should be remembered that the lost output of 2020 will not be compensated for, as seen by the gap.

Conclusion

The future looks more hopeful than it has seemed in the recent past. Of course, bearing in mind that the COVID disease has struck back just when it seemed to have been vanquished, countries in the GCC need to remain vigilant. Once it is clear that that COVID is no more a threat, then GCC countries will have to turn their attention towards reforms that will sustain long-term growth, a process that was disrupted during the last two years.

© Opinion 2021Any opinions expressed in this article are the author’s own

Disclaimer: This article is provided for informational purposes only. The content does not provide tax, legal or investment advice or opinion regarding the suitability, value or profitability of any particular security, portfolio or investment strategy. Read our full disclaimer policy here.