PHOTO

Fitch Ratings - London - Fitch Ratings has affirmed Saudi Arabia's Long-Term Foreign-Currency (LTFC) Issuer Default Rating (IDR) at 'A+' with a Stable Outlook.

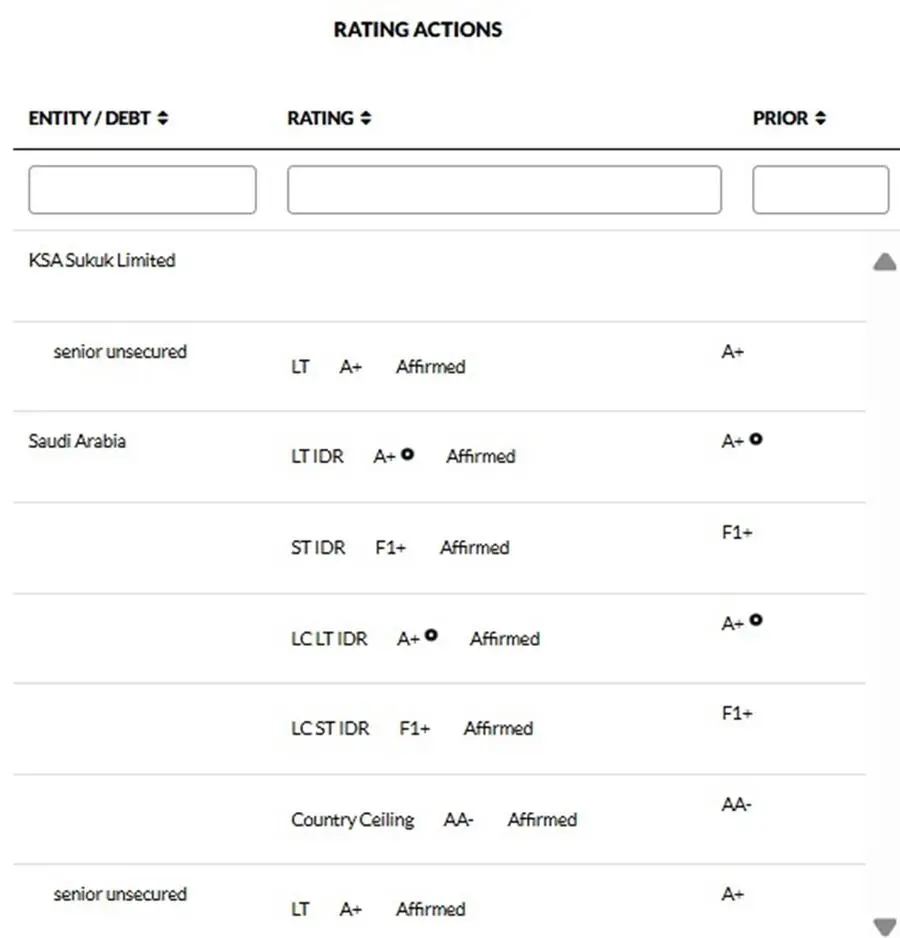

A full list of rating actions is at the end of this rating action commentary.

Key Rating Drivers

Balance Sheet Strength: Saudi Arabia's ratings reflect its strong fiscal and external balance sheets, with government debt/GDP and sovereign net foreign assets (SNFA) considerably stronger than both the 'A' and 'AA' medians, and significant fiscal buffers in the form of deposits and other public sector assets. Oil dependence, World Bank governance indicators and vulnerability to geopolitical shocks have improved but remain weaknesses. Deep and broad social and economic reforms implemented under Vision 2030 are diversifying economic activity, albeit at meaningful cost to the balance sheets.

Strong External Finances: Reserves are forecast to remain large relative to peers', equivalent to an average of 12.8 months of current external payments in 2025 ('A' median 1.8 months), easing to 11.3 months by 2027. SNFA will remain a clear credit strength at 35.3% of GDP in 2027 ('A' median 3.1%). However, large external borrowing across the public and private sectors and a greater orientation toward domestic rather than external investment will continue the multiyear decline in the net external position and move the economy to a net external debtor of 3.4% of GDP by 2027 ('A' median: 6.1%).

Current Account Deficits: Fitch expects a current account deficit (CAD) of 2.9% of GDP for 2025, reflecting lower oil export revenues (due to lower prices; average Brent is forecast at USD70/b from USD79.5/b in 2024) and a continuation of import growth driven by high domestic project spending. Overall exports will increase due to continued double-digit growth in non-oil exports, but this will be outpaced by the associated rise in imports of goods, services and labour.

The deficit will widen to 4.2% of GDP in 2026, reflecting Fitch's forecast that oil prices will fall (to USD65/b) and demand for imports and associated services and labour remain robust due to project execution. Greater domestic orientation of public funds and continued external borrowing will result in financial account surpluses that broadly offset the CAD.

Widening Budget Deficit: Fitch forecasts a budget deficit of 4% of GDP in 2025, driven by lower oil revenues reflecting lower oil prices and a significantly smaller dividend from Saudi Aramco. Non-oil revenues will be supported by the buoyancy of the non-oil economy and improved tax collection. Growth in current spending should be contained, and we expect capex to fall in line with ongoing project recalibration. We forecast a small deterioration in the deficit, to 4.1%, for 2026, in line with Fitch's projection for lower oil prices. We expect the deficit to narrow to 3.6% in 2027 due to rising non-oil revenue, higher oil production and spending growth below nominal GDP growth.

Public Debt Rising but Low: Fiscal deficits will keep debt/GDP rising. Fitch projects debt/GDP at 29.7% of GDP at end-2025 (well below the peer median of 57.3%) and 35.1% at end-2027. The sovereign is adjusting capex to support the fiscal position, although execution of the large project pipeline and new infrastructure projects will constrain the pace for substantial cuts. Saudi Arabia has announced new non-oil tax measures this year. We are not expecting major changes to its non-oil tax policy, although there is a record of adjustments if there are revenue shortfalls.

Strong Growth: We forecast headline GDP growth to rise to 4.3% in 2025 and 4.7% in 2026 before slowing to 3.6% in 2027, driven by increases in oil production. Non-oil growth will remain buoyant, averaging 4.5% over the period, backed by reforms, capex and high spending by government-related entities. Higher oil output will benefit downstream processing industries.

Diversifying Economy: GDP has been rebased and re-estimated, with the level of 2024 headline GDP revised up by 14%, almost entirely due to a 28% increase in the non-oil private sector (now 56% of GDP). Reforms and associated public and GRE funding under Vision 2030 continue to support diversification, with new reforms in 2025 including opening land ownership to non-Saudis and the implementation of a new investment law. Nonetheless, the resilience of non-oil growth to a period of lower government and GRE spending remains to be tested.

Resilience Despite High Geopolitical Risk: Fitch considers that geopolitical risks in the Middle East remain high, and a resumption of military activity is possible. However, the conflict in June between Israel and the US on one side, and Iran on the other, did not have a discernible impact on the robust level of economic activity in Saudi Arabia. Fitch considers Saudi Arabia's oil exports vulnerable to disruption to the Strait of Hormuz, but this did not occur despite the military hostilities. Broader changes in the region have lessened elements of geopolitical risk.

Strong Banks: Banking sector metrics remain strong; at end-1Q25 the capital adequacy ratio was 19.3% and non-performing loans 1.2% (the lowest since 2016). Profitability is high given robust credit growth and high net interest margins. The central bank has tightened macro-prudential policies in the face of rapid credit growth. As credit growth continues to outpace deposit growth, banks continue to step up external borrowing, causing a rapid deterioration in the sector's net foreign asset position, although it is small relative to total sector assets, at 2.7%.

ESG - Governance: Saudi Arabia has an ESG Relevance Score (RS) of '5' for Political Stability and Rights and '5[+]' for the Rule of Law, Institutional and Regulatory Quality and Control of Corruption. These scores reflect the high weight that the World Bank Governance Indicators (WBGI) have in our proprietary Sovereign Rating Model (SRM). Saudi Arabia has a medium WBGI ranking in the 54th percentile, with low scores for Voice and Accountability, and Political Stability and Absence of Violence constraining the average.

RATING SENSITIVITIES

Factors that Could, Individually or Collectively, Lead to Negative Rating Action/Downgrade

-Public Finances: Deterioration in the overall public finance position, reflected in government debt/GDP trending firmly above our forecasts or marked drawdowns of government assets, including government deposits at the central bank

-Public Finances: Significant increases in contingent liabilities that undermine the strength of the public-sector balance sheet and offsetting improvements in narrower government measures, for example due to a sustained rise in government-related entity debt, particularly if this might not result in productive investments in the economy

-Structural Features: A major escalation of geopolitical tensions that affects key economic infrastructure and activities over an extended period

Factors that Could, Individually or Collectively, Lead to Positive Rating Action/Upgrade

-Public Finances: Fiscal reforms that increase the budget's resilience to oil price volatility, for example greater non-oil revenue generation or lower expenditure, while also maintaining the strength of the wider public-sector balance sheet

-Structural Features: A continuation of economic reform that supports strong growth of the non-oil economy

-Public/External Finances: A sustained period of oil prices markedly above our current forecasts that would allow an improvement in the sovereign and external balance sheets

Sovereign Rating Model (SRM) and Qualitative Overlay (QO)

Fitch's proprietary SRM assigns Saudi Arabia a score equivalent to a rating of 'A' on the LTFC IDR scale.

Fitch's sovereign rating committee adjusted the output from the SRM to arrive at the LTFC IDR by applying its QO, relative to SRM data and output, as follows:

- Public Finances: +1 notch, to reflect large public sector assets, including government deposits held with the central bank and state pension funds, that could be mobilised to support government funding

Fitch's SRM is the agency's proprietary multiple regression rating model that employs 18 variables based on three-year centred averages, including one year of forecasts, to produce a score equivalent to a LTFC IDR. Fitch's QO is a forward-looking qualitative framework designed to allow for adjustment to the SRM output to assign the LTFC IDR, reflecting factors within our criteria that are not fully quantifiable and/or not fully reflected in the SRM.

Country Ceiling

The Country Ceiling for Saudi Arabia is 'AA-', one notch above the LTFC IDR. This reflects moderate constraints and incentives, relative to the IDR, against capital or exchange controls being imposed that would prevent or significantly impede the private sector from converting local currency into foreign currencies and transferring the proceeds to non-resident creditors to service debt payments.

Fitch's Country Ceiling Model produced a starting point uplift of +1 notch above the IDR. Fitch's rating committee did not apply a qualitative adjustment to the model result.

REFERENCES FOR SUBSTANTIALLY MATERIAL SOURCE CITED AS KEY DRIVER OF RATING

The principal sources of information used in the analysis are described in the Applicable Criteria.

ESG Considerations

Saudi Arabia has an ESG Relevance Score of '5' for Political Stability and Rights as WBGI have the highest weight in Fitch's SRM and are therefore highly relevant to the rating and a key rating driver with a high weight. As Saudi Arabia has a percentile rank below 50 for the respective Governance Indicator, this has a negative impact on the credit profile.

Saudi Arabia has an ESG Relevance Score of '5[+]' for Rule of Law, Institutional & Regulatory Quality and Control of Corruption as WBGI have the highest weight in Fitch's SRM and are therefore highly relevant to the rating and are a key rating driver with a high weight. As Saudi Arabia has a percentile rank above 50 for the respective Governance Indicators, this has a positive impact on the credit profile.

Saudi Arabia has an ESG Relevance Score of '4' for Human Rights and Political Freedoms as the Voice and Accountability pillar of the WBGI is relevant to the rating and a rating driver. As Saudi Arabia has a percentile rank below 50 for the respective Governance Indicator, this has a negative impact on the credit profile.

Saudi Arabia has an ESG Relevance Score of '4[+]' for Creditor Rights as willingness to service and repay debt is relevant to the rating and is a rating driver for Saudi Arabia, as for all sovereigns. As Saudi Arabia has a record of 20+ years without a restructuring of public debt, which is captured in our SRM variable, this has a positive impact on the credit profile.

The highest level of ESG credit relevance is a score of '3', unless otherwise disclosed in this section. A score of '3' means ESG issues are credit neutral or have only a minimal credit impact on the entity, either due to their nature or the way in which they are being managed by the entity. Fitch's ESG Relevance Scores are not inputs in the rating process; they are an observation on the relevance and materiality of ESG factors in the rating decision. For more information on Fitch's ESG Relevance Scores, visit www.fitchratings.com/topics/esg/products#esg-relevance-scores.

VIEW ADDITIONAL RATING DETAILS

Additional information is available on www.fitchratings.com

FITCH RATINGS ANALYSTS

Paul Gamble

Senior Director

Primary Rating Analyst

paul.gamble@fitchratings.com

Fitch Ratings Ltd

30 North Colonnade, Canary Wharf London E14 5GN

Cedric Julien Berry

Director

Secondary Rating Analyst

cedric.berry@fitchratings.com