Saudi budget faces plunging oil prices, declining reserves and an increase in military spending.

Nada Rifai, ZAWYA

August 27, 2015

PHOTO

27 August 2015 Saudi Arabia faces a rising fiscal challenge with a growing budget deficit amid plunging oil prices, declining reserves and an increase in military spending.

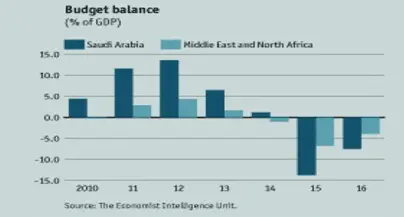

The International Monetary Fund forecasts that the kingdom, the world's largest oil exporter, will record a budget deficit as high as USD 150 billion this year, which is around 20% of the economic output of 2015, as the government maintains strong spending despite the reduction in oil revenues.

The Economist Intelligence Unit (EIU), however, expects the fiscal deficit to reach 13.3% of GDP--the largest shortfall since 1987-- inflated by the rising costs of the Saudi-led air campaign in Yemen.

'In my opinion the kingdom has never been under a threat so severe due to falling oil prices,' Fereydoun Barkeshli, senior analyst, oil and gas, at the International Institute for Energy Studies (IIES), told Zawya by email.

He said the 2015 government budget was based on international crude oil of USD 96 per barrel.

Oil prices have plunged to 6-1/2 year lows on concerns over market oversupply and China's slowing economy. Saudi Arabia and other members of the Organisation of the Petroleum Exporting Countries (OPEC) have decided not to cut oil output to shore up prices, focusing instead on defending market share and forcing cuts from higher cost producers such as shale drillers.

The Saudi government, which depends on oil exports for around 80 to 90 percent of its revenues, has been reluctant to reduce its role in driving economic growth.