PHOTO

Ratings agency Moody's on Thursday improved its outlook on Qatar's banking system from negative to stable, and also said that recent rate rises by central banks in Saudi Arabia and the United Arab Emirates would led to increased profitability for the two Gulf states’ lenders.

Moody's said in a note on Qatar's banking system that its improved outlook for Qatar's banks reflected "the resilience of the country's economy and banking system to the ongoing regional dispute", as well as its recent change to the outlook for Qatar's sovereign rating, also from negative to stable, although the rating itself remained unchanged at Aa3.

Moody's said in the note that Qatar's real gross domestic product (GDP) growth is likely to improve this year, with GDP estimated to grow to 2.8 percent between 2018-2022, up from 1.6 percent last year.

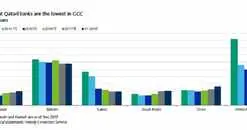

Yet, although problem loans also grew in the first half of 2018 to 2 percent of gross loans - up from 1.6 percent last year - and this could grow to between 2.2-2.5 percent of gross loans next year, due to ongoing issues in the construction and contracting sectors, the level of problem loans in the country’s banking system remains among the lowest in the region.

In a press release accompanying the report, Nitish Bhojnagarwala, a vice president and senior credit officer at Moody's, said: "The Qatari economy has rebalanced as supply chain disruptions recovered rapidly following the blockade from other Gulf states and Egypt.

"Likewise, the banking system rebalanced its funding profile with the reduced liquidity from GCC sources offset by inflows from government and related entities," he added.

In a separate note on the Saudi banking sector, Moody's said that a decision on September 26 by the Saudi Arabian Monetary Authority to raise interest rates by one quarter of a percent to 2.25 percent, shadowing the United States Federal Reserve's move given the riyal's peg to the U.S. dollar, was likely to increase gross yields enjoyed by Saudi banks as they re-priced variable rate assets. It said gross yield (the amount of interest income earned as a portion of average interest-bearing assets) had already increased to 3.8 percent in the first half of 2018 - up from 3.4 percent last year and 3.2 percent in 2016. This is due to the difference in the amount of interest income banks can generate and their own (lower) cost of funding.

However, the agency also warned that higher interest rates will weigh on the borrowing costs of both corporate and household lenders, especially those that are already highly leveraged. It said that it expects problem loans in Saudi to increase to 2.5 percent over the next six to 12 months, up from 2 percent by the end of June.

Banks in the United Arab Emirates are also likely to become more profitable for many of the same reasons as Saudi banks, with a recent interest rate rise (as a result of its pegged currency) set to translate into higher gross yields and increased government spending in the country likely to "support economic growth and lending opportunities".

It said the banks that will benefit the most will be those, such as Emirates NBD, First Abu Dhabi Bank, and Abu Dhabi Commercial Bank, are those with higher levels of corporate loans, as they are easier to re-price.

Despite this, the agency earlier last week had placed all ratings it held on Commercial Bank of Dubai on review for a potential downgrade, citing a "material increase in problem loans" in its corporate and mid-corporate portfolio. It had said that problem loans increased to 8 percent of its total loan book under the new IFRS 9 accounting regime, as compared to 6.1 percent (under IAS39 accounting rules) last year.

Further reading:

- Bank merger: Abu Dhabi deal could be “more positive for UNB”: analyst

- Hitting the right note: First Abu Dhabi Bank developing sound-based payment system

- Barwa, IBQ bank merger good for Qatar market, analysts say

- UAE banks to record higher profitability and liquidity through 2018: Report

- Gulf banks' problem loans may be higher than reported, says S&P

(Writing by Michael Fahy; Editing by Shane McGinley)

Our Standards: The Thomson Reuters Trust Principles

Disclaimer: This article is provided for informational purposes only. The content does not provide tax, legal or investment advice or opinion regarding the suitability, value or profitability of any particular security, portfolio or investment strategy. Read our full disclaimer policy here.

© ZAWYA 2018