Sunday, Mar 14, 2010

By Tariq Al-Rifai

Of DOW JONES INDEXES

DUBAI (Zawya Dow Jones)--A lot has been said about sukuk recently. Like other financial instruments, sukuk have had to weather the storm and were not immune to the financial crisis. There were a few high-profile scares in 2009. Most notably the TID Global Sukuk 1, a $100 million sukuk issued by Kuwait-based The Investment Dar (TID.KW), and Nakheel Development Limited a $3.5 billion sukuk issued by Dubai-based developer Nakheel. The near default of the Nakheel sukuk in particular created an enormous ripple effect throughout Dubai and the rest of the world. Eventually, Nakheel agreed to repay sukuk holders as planned with help from the government of the United Arab Emirates.

This bad news seemed to over shadow the good news. The good news in my opinion is the great growth potential this industry holds in the near and longer term.

Sukuk have not been around as long as some may believe. Even though modern Islamic finance took off in the mid-1970s, the sukuk industry didn't get started until the 1990s. The Malaysian government and Malaysian corporations were the first to adopt sukuk structures as an alternative to conventional bonds, driven mainly by the country's need to finance its vast infrastructure projects. Once established in Malaysia, sukuk found their way to the Middle East and started to take root. The government of Bahrain was one of the first in the region to issue sukuk and promote their use.

By 2000, sukuk were already a multibillion dollar industry and growing fast. According to Zawya.com total sukuk issued worldwide at the end of December 2009 amounted to $114.7 billion, nearly half of this is from Malaysian issuers. Last year may not have been a vintage for debt issuers around the world, but it was a good year for sukuk issuers. In 2009, there were over $24.4 billion in new sukuk issues, $13.2 billion of which came from Malaysia according to Zawya.com.

STORM CLOUDS

One of the major problems of sukuk is their short-term focus. There has never been a 30-year sukuk even a 15-year sukuk is very unusual. Most sukuk have three to five-year maturities, which don't play well among global debt buyers as they seek long-term paper to hold. There have been a few exceptions, mainly from Malaysia where sukuk are primarily denominated in Malaysian Ringgit and have longer maturities.

This short-term mentality is what got issuers in trouble, the classic mismatch of short-term money financing medium-term projects. Middle East issuers believed that there was little appetite for long-term sukuk. Therefore, they issued sukuk with three to five-year maturities even though the projects they were financing may not mature during that time. The solution was to refinance when the sukuk reached maturity. After all, there has been a lot of demand for sukuk issues and they were usually oversubscribed.

This worked well until financial markets shut down in late 2008. Sukuk issues that were maturing had no place to go. They were stuck. Once financial markets opened up again issuers realized that refinancing, if possible, would cost them a lot more than they had expected.

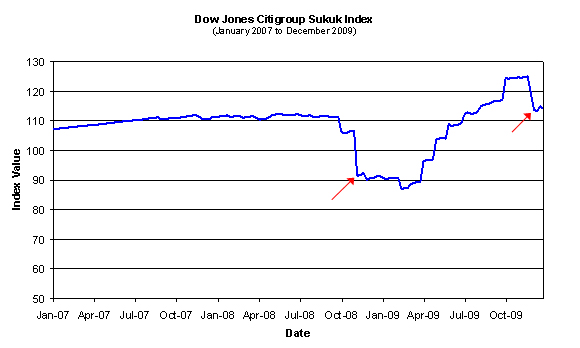

The chart below shows the performance of the Dow Jones Citigroup Sukuk Index over the past three years. As you can see, the two dips in the market were the result of the global financial crisis followed by Nakheel's close shave with default.

What helped sukuk issues in 2009 was strong Middle East demand. Nearly all issues last year were in local currencies instead of the U.S. dollar and purchasers were local as well. Saudi Arabian-based Saudi Hollandi Bank (1040.SA), for example, recently issued a 725 million Saudi Riyal ($193 million) sukuk with strong demand. It's important to note however, that sukuk issued in Saudi Riyals, Kuwait Dinar and U.A.E. dirham tend not to be rated as local investors will forgo ratings in return for higher returns. These sukuk are not included in the Dow Jones Citigroup Sukuk Index as issues included in the index need to be rated and denominated in U.S. dollars.

GUIDELINES

Many industry insiders believed that statements issued in late 2007 by the President of the Accounting & Auditing Organization for Islamic Financial Institutions, or AAOIFI, would kill or at least slow the rapid growth in the sukuk market. The statements contended that the financial engineers behind the sukuk were not adhering to the proper sukuk structures as required by Shariah law. This included guaranteeing the principal and the returns of the sukuk and providing inadequate ownership rights for the sukuk holders. In essence, the assertion was that sukuk structures were too similar to conventional bonds, which render the sukuk as merely another form of an interest-bearing loan. According to AAOIFI, this would need to change going forward as it would no longer approve those sukuk structures.

In my view, these new structure guidelines will benefit the industry over the long-run as sukuk are inherently different from conventional bonds, mainly in that sukuk are not debt as commonly defined, they offer investors beneficial ownership in assets and receive their returns on use of the assets. This key difference needs to be highlighted in order to attract new buyers and issuers. These new buyers and issuers will choose sukuk over conventional bonds because they see the differences and they are more inline with their objectives than conventional bonds. After all, sukuk are an alternative mode of financing.

I strongly believe that more and more sukuk issues will continue to hit the market in the coming years. As we saw in 2009, the sukuk industry managed to grow in a tough environment. Today, both investors and Middle Eastern governments support sukuk investment. Many governments in the region are increasingly issuing more sukuk and reducing their issuance of conventional bonds. They are also encouraging government-backed companies to issue sukuk over bonds. Investors across the globe are showing more interest in sukuk and this trend is unlikely to change.

For a glimpse of what's in store for the sukuk industry, just look at the recent $500 million GE Capital sukuk. It is the first sukuk issued by a major U.S. company and is paving the way for multinationals to follow.

(Tariq Al-Rifai is an Islamic finance expert and director of Islamic Market Indexes for Dow Jones Indexes. He can be reached at tariq.alrifai@dowjones.com, or +9714-446-1670.)

Opinions expressed are those of the author, and not of Dow Jones Newswires, or Dow Jones Indexes.

This column is published for information only, and it neither constitutes, nor is to be construed as, an offer to buy or sell investments. The information and opinions expressed herein are based on sources the author believes to be reliable, but he cannot represent that they are accurate or complete. Any information herein is given in good faith, but is subject to change without notice. No liability is accepted whatsoever by Dow Jones Indexes, employees and associated companies for any direct or consequential loss arising from this article.

Copyright (c) 2010 Dow Jones & Co.

(END) Dow Jones Newswires

14-03-10 0632GMT