With the exception of hotels, other sectors of the Jeddah market have moved into the early downturn stage of their cycle over the past six months.

Capital Business

July 26, 2009

July 2009 With the exception of hotels, other sectors of the Jeddah market have moved into the early downturn stage of their cycle over the past six months. Rents have stalled and are falling in effective terms in the office and retail markets. Sale prices have declined 6% to 10% at the upper end of the residential market over the past six months. Jeddah has recently launched its vision to guide the growth of the city over the next 20 years. This vision includes ambitious plans for the regeneration of older areas of the city and major new investment in its urban infrastructure.

Jeddah scored relatively poorly in our recent MENA Investor Sentiment Survey, with investors ranking the city below others in the region on a range of criteria including infrastructure, environmental / sustainability and real estate market transparency. However, this consensus may be lagging behind events on the ground in Jeddah. As our City Profile reveals, Jeddah is implementing a number of major regeneration initiatives and is aggressively investing to upgrade its urban infrastructure.

At the heart of many of these initiatives is the Jeddah Development and Urban Regeneration Company (JDURC). Founded in 2006, this company has a mandate to create public private partnerships (PPPs) and facilitate the regulatory process for redevelopment initiatives.

Two of the boldest initiatives currently being undertaken by JDURC involve the redevelopment of the Khozama and Ruwais areas of the city. Joint ventures have been created with private developers and investors to clear and rebuild these currently run-down areas. Royal decrees have been issued to enable expropriation of existing buildings, many of which comprise "unplanned settlements". JDURC's strategy is to relocate people from these areas to new and affordable communities to the east of Jeddah.

These districts will be planned with new roads, services and infrastructure being provided before sites are made available for private sector development.

A different form of initiative is the City Centre Development Corporation (CCDC), a consortium involving Jeddah Amana and private developers led by the Urban Development Company (UDC).

The CCDC has been created to rehabilitate the Jeddah Central and Historic districts. This redevelopment strategy includes a new planning framework and the voluntary involvement of landowners in the area.

These initiatives are being aligned with a broader strategy of improving the city's transportation infrastructure, including:

Expansion of the capacity of the Jeddah Islamic Port.

Several new overpasses around Jeddah in order to free up points of congestion on the road system.

Planned light rail system linking the city centre and the airport.

The new high speed Makkah-Madinah railway which is expected to commence construction in the next year.

The western terminus for the Saudi Arabia "landbridge" rail project which will enable logistics connections across the country from Jeddah to Riyadh and Damman.

Perhaps the most visible infrastructure investment will be in the redevelopment of Jeddah's international airport, which will create capacity for up to 25 million passengers per annum. The airport authority (GACA) is working with Aéroports de Paris International to deliver this project by 2012 or 2013. A key component of GACA's vision is the development of a major airport city, along the lines of Schiphol in the Netherlands. Master developers will be selected to undertake a range of projects including business parks, retail, residential, hospitality and recreational areas.

The city is also aware of the need to improve Jeddah's public spaces and there are initiatives underway to improve popular areas such as the Corniche and Tahlia Street, as well as cover the central canal to provide public space.

The regional governor and mayor have recently crystallised all of this activity with the official launch of Jeddah's 20-year vision in May. The reality is that various public and private interests are now responding to the challenges being posed to Jeddah by the force of centralisation to Riyadh, the emergence of SAGIA's new economic cities and the increased attraction of other GCC cities.

Some of these initiatives may not secure all of their ambitious aims, while others will thrive.

However for participants in the real estate market, Jeddah will be one of the world's most interesting cities over the next 20 years.

Economic Commentary Cuts in oil output and subdued non-oil growth mean that Saudi Arabia's economy is set to contract 1% in 2009. According to forecasts from the IMF, real gross domestic product (GDP) will resume growth of around 3% in 2010. The fall in oil revenues has been the result of the 14% reduction in oil output this year, as OPEC members attempt to support global prices.

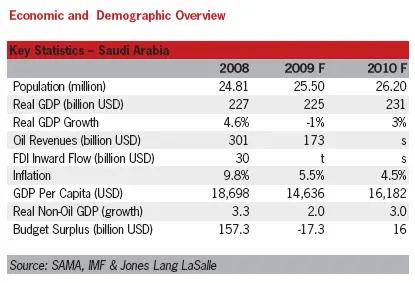

While the oil sector is producing less wealth in 2009, the non-oil private sector continues to grow, albeit more slowly. This sector is forecast to grow by 2% this year and 3% next year.

SAMA, the central bank, cut its reverse repo rate by 25 basis points to 0.5% in mid-April. Banks' nonstatutory deposits with SAMA have risen sharply since the intensification of the global financial crisis in the third quarter of last year, reaching $20 billion by the end of February. Bank lending to the private sector rose for the first time in three months in February. Though the increase was minimal (only 0.2%), it suggests a greater willingness among banks to lend again, even if the bulk of the new lending was for less than one year.

The banks' reluctance to lend reflects more than simple liquidity issues. Banks have become increasingly selective about whom they provide funds. This is particularly the case since their access to US dollar funding remains constrained following the retreat of international banks from the Saudi corporate market.

While lending to the private sector remains constrained, figures from MEED Projects indicate that public investment growth is compensating for the slowdown in private investment. The total value of new public sector contracts awarded across Saudi Arabia between October 2008 and April 2009 amounted to over $137 billion, eclipsing the $62 billion worth of projects cancelled or put on hold during the same period. The number of projects on hold appears to have stabilised in recent months.

The government is holding good on its commitment to increase capital spending sharply over the medium term. Oil and gas projects have featured heavily in recent contract awards, as have electricity, water, education and infrastructure projects.

Demographic Commentary Jeddah's population is estimated at around 3.4 million, accounting for some 14% of the national total. Over the period 2004-2008, this grew by a Compound Annual Growth Rate (CAGR) of 2.3%.

There are an estimated 1.6 million expatriates in Jeddah, comprising 47% of the total population, the highest ratio of expatriates in the Kingdom.

Property Market Drivers A young and growing population, as well as increasing numbers of both domestic tourists and expatriates, are driving the Jeddah residential and retail markets. Jeddah offers a much "easier" environment for foreigners to settle in, with more properties for both rental and sale to expatriates than any other city in the Kingdom, especially in the low to mid-income apartment sectors.

The municipality has recently released a 20-year vision as its official plan to guide the future expansion of the city. Three of the main pillars of this vision are:

Construction of new urban infrastructure.

The redevelopment and regeneration of older innercity neighbourhoods.

The gradual resettlement of almost 900,000 people from "unplanned settlements" to affordable housing.

Other aspects of this vision include upgrading the Corniche area to provide improved amenities and attract luxury residential development.

The growing number of Hajj and Umra pilgrims visiting Jeddah has been the prime driver for a major redevelopment of the King Abdul Aziz International Airport and the construction of new hotel projects in the city.

Property Clock The Jeddah market is currently experiencing something of a slowdown, with all sectors except for hotels moving into the early downturn stage of the property cycle over the past six months. Most sectors have seen increased levels of new supply enter the market at a time of subdued demand resulting from the global economic slowdown, the adjustment in oil prices from their cyclical peak, and tight credit conditions.

The retail sector is adjusting to the wave of new mall openings in 2007-2009, which will still take some time to absorb, and there are also signs that the supply of new office space has exceeded current levels of demand. The residential sector has also been negatively impacted by reduced consumer confidence and limited credit availability.

Hotels are the one sector still experiencing an upswing, with further growth in room rates and occupancies being recorded over the past six months, as much of the planned new supply has not yet entered the market.

Office market Supply Following almost a decade without any significant additional new office development, over 300,000 sq m is scheduled for completion before the end of 2010.

Unlike Riyadh, Jeddah has no well-defined central business district, with the central area of Balad lacking a significant supply of modern office space. Traffic congestion and a lack of parking in the downtown area have dispersed new office space to a handful of clusters scattered across the city.

Much of the new supply is in owner-occupier buildings for banks such as Al Jazeera or local groups such as SEDCO, as both these sectors and the government prefer to own their own space. Most of the new multi-tenant supply available for lease is in mixed-use buildings that have retail space on the lower and mezzanine levels. There is one notable example of a Class A multi-tenant building that has been delivered this year: Jameel Square on Tahlia Street.

Two of the large office projects currently under construction (the Headquarters and Zahran buildings) are being developed for strata ownership. While local businesses in Jeddah have demonstrated an appetite for owner occupation, these projects will test whether this preference extends to strata tenure. Jeddah Gate is also seeking to launch its office tower with pre-sales on this basis.

The predominant direction of office development has been towards the north of the city, with more than 50% of the new supply in 2009-2011 on the north Corniche, Malak Road, or Amir Sultan.

A number of the major long-term redevelopment plans recently launched by the city aim to create opportunities for new office development in the traditional centre of Jeddah. The Khozama project being master developed by Dar Al Arkan will create new infrastructure and provide sites for commercial development. The CCDC's Central District program will enable landowners to join in a consortium to redevelop the old CBD and port area. To the north of the city, GACA is starting the tender process for its Airport City scheme, which will offer the opportunity to develop a major new business park.

Demand Demand in the Jeddah leasing market has been driven by smaller requirements for multi-tenant buildings rather than large single-tenant deals over the past six months.

Most tenant interest has been focused on the betterquality new projects coming to the market, including Jameel Square and Jeddah 101. Demand is concentrated in the finance, professional services, and real estate and construction sectors. Recent deal announcements include:

Saudi Arabian Lubricant Oil Co. (Petromin), which leased 3,000 sq m of office space in the Aya Mall.

Phillips, which took around 1,500 sq m in Jameel Square.

Intermarkets (part of WPP Ad Agency) and Aayan Holdings, which have both taken office space in the Le Chatu project.

Iwan and Sadia, which have each taken one floor of around 600 sq m in Jeddah 101.

Performance Vacancy levels are increasing in line with the number of new buildings being completed.

Generally speaking, the good-quality projects are leasing but others are struggling. Signs of saturation are emerging in some areas such as Amir Sultan, where a couple of proposed projects have now stalled. Tahlia Street recorded the lowest vacancy rate at 5%, while vacancies in prime buildings in other areas such as Malak Road stood at around 10%, an increase from 8% earlier in the year.

Office rents currently range between SR 400 to SR 1,200 per sq m, depending on location but also style of building. The average is SR 730, which has remained largely unchanged over the last six months. As vacancies increase, we expect to see landlords offering longer grace (rent-free) periods to attract new tenants.

In the sales market, strata buildings have been marketing units at between SR 9,000 per sq m and SR 13,000 per sq m, although some unique units are asking somewhat higher values. There have been relatively few deals to test the actual transaction level in the strata market.

Market Outlook Demand has been moderate so far in 2009 and has failed to keep pace with the steady supply of new office buildings entering the market. With rents flat and lenders cautious, we do not expect many more building launches, but it will take the market some time to absorb what has just been delivered.

As the market becomes increasingly competitive, the successful buildings will be those that offer better-than-average parking, convenient access and higher-quality facilities than have so far been experienced in the Jeddah market.

Residential market Supply Jeddah has a current stock of around 807,000 residential units. The pipeline of announced projects could deliver an additional 30,000 units over the next five years but completions have not been keeping up with announcements. We estimate that only around 5,000 units are under construction by private sector developers, of which 60% are apartments. The majority of this supply will be delivered through stand-alone buildings (not communities) or middle income villas in the east and south of Jeddah.

During the go-ahead days of 2007-2008, a number of luxury tower developments were launched, particularly on the Corniche. While some of these are proceeding, there have been numerous cancellations or delays in this luxury high-rise category. Sama Dubai, Damac and Diamond Tower are examples of projects with little evidence of construction. Kinan announced the postponement of its Andalucia Towers project on the Corniche last quarter.

More attention is now being focused on the midmarket sector. A good example of this trend is Ewaan, a new joint venture between the Islamic Development Bank, SEDCO and the Public Pension Agency (PPA). They have a 1.1 million sq m site north of Jeddah where they are planning to develop 2,500 houses and apartments. Kinan and Saudi Binladin recently announced a joint venture for a similar development called Asfan. They plan to develop 2,500 units, typically priced below SR 800,000.

As part of its drive to redevelop inner-city districts and reduce the number of people living in unplanned accommodation, the city has created public private partnership (PPP) vehicles for the Khozama and Ruwais districts. As part of this process, the city has agreed to sponsor the development of affordable housing alternatives to the east of Jeddah. However, development of these projects may take some time to start.

The high end of the villa market is being driven by the construction of several projects in the Muhammadiya and Bassateen districts. These projects are typically developed on a site-by-site basis with villas costing between SR 1.1 million and SR 6 million.

Demand Demand has generally reduced in 2009 compared to last year, with projects taking longer to sell and less speculation occurring (with off-plan sales no longer allowed without specific approval).

Average monthly incomes are lower in Jeddah than in Riyadh. With land in Jeddah being more expensive, the market has accepted apartment accommodation. With a large supply of apartment buildings, the residential investment sector is the largest in the Kingdom. Demand for luxury high-rise apartments is being driven by a combination of speculators and end user demand from Saudi expatriates who split their time between Jeddah and overseas cities.

Affordability is the big challenge in translating midmarket demand into volumes. With land prices in Jeddah so high, it has been hard for the market to meet the demand for affordable and mid-range housing. As a result, most of the new mid-market developments are located in the peripheral areas north of the airport. The proposed mortgage law (once approved) will help improve affordability and thereby boost the demand for middle income housing.

Performance Apartment rents have been generally flat in 2009.

Annual rents for two-bed apartments range from SR 12,000 to SR 25,000 depending upon the location and the age of the building.

New residential units in waterfront locations, such as on the north Corniche, still command the highest selling prices, though prices in this sector have declined by 5% to 10% over the past six months. Sale prices in other locations (Al Hamra, Rawdah, Shatee, Nadah, Muhammadiya and Basteen) generally range between SR 5,000 and SR 8,000 per sq m. Apartments in Jeddah had higher average occupancy levels than villas in Q2 2009, at 95% compared to 90%.

Market Outlook The supply of units is increasing faster than demand, particularly at the upper end of the apartment market. However, we do not see significant oversupply due to expected construction delays in the planned mega residential communities. As the market absorbs the stock offered for sale in stand alone buildings and small-scale development, prices could start to rise again towards the end of the year, albeit at a modest rate.

Developers in the middle income segment are still enjoying relatively healthy trading conditions. An increasingly two-tier market is likely to develop going forward, with factors such as the reputation of the developer and the quality of the ongoing management of the development becoming increasingly important in determining the rate of sales.

Retail market Supply The retail inventory in Jeddah currently stands at around 1 million sq m (gross leasable area [GLA] in organised malls). If all the announced projects proceed, this will increase to around 1.6 million sq m by 2014.

Significant levels of new supply in 2008 have resulted in oversupply. It is expected to take between one and two years for the market to absorb all the newly completed retail space.

Examples of major recent additions are Mall of Arabia, where Madinah Road meets the airport, and the Andulus Mall on the former airport site. Central Park (located across the street from Andalus Mall) is the only major mall scheduled for completion over the next 12 months.

Al-Hokair, SEDCO and Al-Habib are major landlords and rivals in the Jeddah shopping centre market.

They are competing through innovation and adding new components to their malls including traditional souq areas, jewelry markets, ice skating and even skiing.

Jeddah is also absorbing a large number of mixed use projects where the ground and mezzanine floors are retail showrooms, with the upper floors in office or residential use. Examples can be seen all over Jeddah, but they are especially prominent in Hera and on Amir Sultan Road.

A number of major mixed-use projects with significant retail components are proposed over the longer term. The Khozama redevelopment project by Dar Al Arkan and JDURC will add more than 100,000 sq m of retail space over the next 10 years. Another new retail cluster will emerge when the land to the south of the new terminal at the King Abdul Aziz International Airport is released (although commencement of this project is still three to four years away). The Jeddah Central and Historic districts will also have considerable retail components, although residential will be their main driver.

Demand Both religious and vacation tourism support retail demand in Jeddah. The Jeddah Spring Festival (in the second quarter) boosted spending as some 936,000 people from all over the Kingdom attended. The Supreme Commission for Tourism reported an average retail spending of almost SR 550 per day for each family. Pilgrims visiting Makkah and Madinah add an extra 3% to 4% to total retail spending in Jeddah.

Bin Dawood, Danube and Panda are the major hypermarket chains in Jeddah, while other players such as Carrefour and Geant are also entering the market. In stand-alone developments, Al-Haram, City Max, Extra and Electro have all reported good growth in sales.

Performance Headline rents in quality malls remain at the same level as recorded in the last quarter of 2008. Mall operators normally grant a grace (rent-free) period of two months but this may be increased to as much as six months for anchor tenants. This has reduced the effective rents. Anchor tenants (big hypermarkets) are moving from low-performing malls and are pushing to secure concessions of 10% to 30% on the asking rents.

Current average asking rents in retail malls across Jeddah are in the region of SAR 1,800 per sq m. Higher rents around SAR 2,000 to 3,000 per sq m have been established in the primary locations (such as the Aziz Mall, Red Sea Mall of Arabia). Shopping centres lacking a variety of restaurants and entertainment or those located in secondary locations have reported lower rents at approximately SAR 1,200 per sq m. Vacancy levels are increasing across the market.

While vacancies remain relatively low (less than 5%) in the Red Sea Mall, Aziz Mall and Tahlia Center, other malls that previously enjoyed 100% occupancy are now seeing more vacant units. Hera International, Jamjoom Center and Sawary Mall have lost their position and have seen vacancies increase to around 15%. These centres are likely to experience a decline in rents if they are unable to secure anchor tenants and quality restaurants.

Market Outlook The Jeddah retail market will see a "flight to quality" as old shopping centres lose customers to new ones. New mega malls will be managed more proactively in order to compete with stand-alone hypermarkets like Danube that are leveraging their volume and distribution. Developers will need to undertake more market testing before launching the next wave of projects.

Hospitality market Supply Jeddah is the gateway for nearly four million Muslim visitors who travel to Makkah and Madinah every year. Jeddah's location on the Red Sea coast has also made it a prime destination for leisure activities for Saudi nationals during the summer.

In the fourth quarter of 2008, initial contracts were signed for the first phase of an ambitious $38 billion tourism master plan for the development of 19 resort destinations along the Red Sea coastline.

These locations will target domestic rather than religious or international tourism. The government is also moving ahead with the multi-billion-dollar Al-Rayis project that will be Saudi Arabia's first resort town on the Red Sea Coast.

There are currently just over 3,600 quality hotel rooms in Jeddah. There has been almost no new supply of four- and five-star hotels over the last decade until very recently. Rosewood Corniche (127 rooms) is the only five-star hotel to have entered the market last year. Five-star properties dominate the quality hotel segment, as they represent 68% of the total quality hotel room supply.

A number of large mixed-use developments with hotels have been recently announced across Jeddah, although their delivery dates remain uncertain. With the addition of these mega projects, Jeddah's hotel room supply is estimated to increase to around 5,500 quality hotel rooms by 2014.

Demand The expansion of the King Abdul Aziz International Airport and the Islamic Sea Port, the promotion of the Red Sea coastline for water sports and its proximity to Makkah and Madinah are the major demand drivers for the hotel market in Jeddah.

Increased construction activity in King Abdullah Economic City (KAEC), King Abdullah University of Science and Technology (KAUST), Makkah and Madinah have also stimulated additional hotel night demand in Jeddah, though once completed, these projects may compete directly with Jeddah hotels.

Jeddah does not suffer from the same seasonality as other hotel markets in Saudi Arabia, although the period immediately preceding and following Hajj sees less traffic because of visa restrictions. New Umrah regulations are changing this pattern by allowing pilgrimage immediately after Hajj. The high season for hotels in Jeddah includes the periods of the annual Jeddah Festival (from June to August), the month of Ramadan and Hajj periods.

The appeal of the Red Sea means that Jeddah is the most popular destination for domestic tourists. The city has also benefited from the recent relaxation of visa rules that now permit group tourist visas. Many groups from European countries visited Jeddah this year, driving an increase in demand for hotel rooms.

Performance Since 2003, average occupancy has increased by around 2% per year, to reach approximately 73% in 2008. Occupancy rates were highest amongst five star hotels in the second quarter of 2009.

During the high season, average occupancy rates vary between 65% and 80%, while average room rates are between SR 550 and SR 1,000. Average occupancy ranges between 50% to 60% during the low season, whereas average room rates fluctuate between SR 400 to SR 600.

With occupancy and RevPAR increasing in recent years, the Jeddah market has the capacity to accommodate the additional five-star hotels which are expected over the next three years.

Market Outlook The planned development of Red Sea resorts is expected to enhance the Jeddah area's hold on the Saudi leisure tourism market. There will, however, be increased competition between a more diverse range of accommodation locations in the city, on the Corniche, near the airport or in resort locations outside of Jeddah itself.

The steadily increasing level of domestic tourism and the more rapid increase in business tourism suggest the Jeddah hotel market has the potential to achieve higher ARRs and RevPAR performance in the near future, despite the level of additional new supply entering the market.