Fresh worries have gripped global financial markets as French and Greek citizens ousted their respective governments that tried to enforce soul-wrenching austerity measures. Instead, voters have opted for parties that are promising growth and a rejection of the policies by previous governments.

Most analysts think the Eurozone is now in a complete mess.

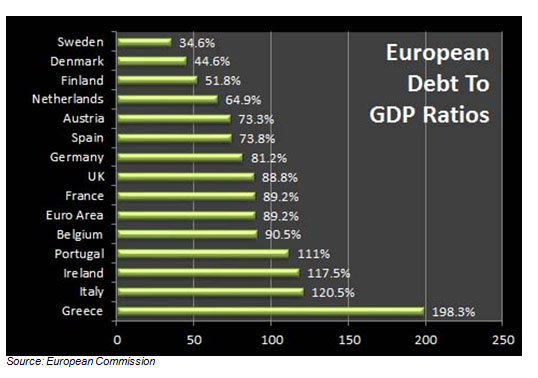

"In less than two years, we are now up to a total of seven European leaders or ruling parties that have been forced out of office, courtesy of the spreading government debt crisis -- tack on France now to Ireland, Portugal, Greece, Italy, Spain and the Netherlands. Even Germany's coalition is looking shaky," David Rosenberg, a renowned economist known for his bearish views, said in a note.

"This is quite a potent brew -- financial insolvency, economic fragility and political instability."

Greece's exit is not only possible (despite there being no provision yet for such exits) it is also probable, said Rosenberg. And that could see the whole union fall apart.

"In the final analysis, it won't be the Germans that decide, but the Greeks. The political movement for secession, my friends, is going strong -- and could happen this year," said the economist. "And when it does, don't think for a second as the Drachma printing machines are dusted off that we won't see a domino effect take hold in the rest of the periphery. Even if it doesn't, I would be surprised if a Greek exit from monetary union would not trigger a run on Portuguese and Spanish (even Italian and French) banks."

"Clearly, the Grexit scenario that we describe here is subject to major downside risk, namely that exit fear contagion following Grexit could be much stronger than anticipated, leading to a sequence of sudden stops in the external financing of periphery sovereigns, banks and other private entities," noted Citibank's Willem Buiter and Ebrahim Rabhari. "Unless an official ECB/EFSF/ESM/IMF firewall/ big bazooka can deter or negate such a withdrawal of market funding, there could be a sequence of forced exits from the [union], reducing the euro area to a greater [deutsche mark] zone."

The German government, which has spearheaded the austerity drive, has fired a warning shot to the two new goverments to adhere to the policies that were already agreed upon, and that could lead to substantial fireworks Brussels.

MARKET REACTIONS

Global financial markets have reacted negatively to news of a socialist government in Paris and a leftist government in Athens.

Markets are now pricing in a much larger risk premium as the euro problems that had been bubbling on the edges during the past few months have come back to the forefront once more.

Dr. Mohammed El-Erian, CEO and co-CIO of executive of bond giant PIMCO, says that Europe needs to iterate simultaneously to the following:

1. A better policy mix at the national level that delivers both growth and solvency over the medium-term;

2. Stronger regional firewalls to act as circuit breakers to counter technical contagion;

3. Enhanced capital adequacy and asset quality for certain banks; and better institutional underpinnings.

"And all this will only materialize properly in the context of a clearer vision of what Europe should look like in three years' time," says Mr. El-Erian.GULF MARKETS

Gulf markets are also giving up some of the gains they made ealier this year. Dubai market is on a nine-day losing streak and most of the key regional markets were in negative territory last month, with the S&P GCC index falling close to 3% on the back of a market correction and euro fears.

More importantly, oil prices are slowly receding, although they do remain at a healthy $113 for a barrel of Brent crude. Opec officials have been targeting a $100 per barrel price, and they must just get their wish sooner rather than later if the euro crisis implodes.

More than 25% of the GCC imports originate from the EU and historically the GCC has recorded large deficits with Europe, noted a Gulf Investment Corporation report, highlighting the importance of EU events on Gulf economics.

"However, the weakening of the EUR is expected to soften the trade deficit and also reduce imported inflation. Overall, inflation is expected to remain contained in the GCC region, with Bahrain and Qatar forecast to record 2012 rates of 3.3% and 2.1% respectively. While UAE is expected to record around 2.4%, it is expected to be marginally higher in Kuwait and Saudi Arabia, at 4.3% and at 5.0%, due to the faster and more widespread wage and salary increases which has triggered substantial increase in food prices and rents."

GIC thinks regional equity and debt markets will be dictated by geopolitical risk within the region, oil prices and macro data from Europe and the US.

"The primary market will remain receptive to good quality issuances. In the short-term, the market will continue to prefer high-growth over high-yield, till the global uncertainty recedes."

Brace yourself - we seem to be in for a roller-coaster ride.

© alifarabia.com 2012