Islamic equity funds have come a long way since their launch in the 1980s. While the first Islamic banks were established in the Middle East in the 1970s, it took about ten more years until the first Islamic equity funds arrived.

Zawya Dow Jones News

July 11, 2010

Sunday, Jul 11, 2010

By Tariq Al-Rifai

Of DOW JONES INDEXES

DUBAI (Zawya Dow Jones)--Islamic equity funds have come a long way since their launch in the 1980s. While the first Islamic banks were established in the Middle East in the 1970s, it took about ten more years until the first Islamic equity funds arrived. And surprisingly the first products were launched in the U.S., Singapore and South Africa, followed by Malaysia and then finally the Middle East.

In 1996, there were approximately 40 Islamic equity funds globally, today there are more than 400. This impressive growth was paralleled by a surge in assets under management. From 2000 to 2008, assets under management in Islamic equity funds grew at an average annual rate of 30%. To express this in dollar terms: in the year 2000 there was roughly $3.8 billion under management in Islamic equity funds, by the end of 2008 these assets reached $30 billion. However, a closer look at this growth reveals some interesting trends and key issues undermining the industry's future.

TRENDS

The first funds were created as a result of strong demand by Muslim investors, who asked managers to create funds that comply with Islamic investing principles. And fund managers responded positively to this demand. Swiss private banks were among the first who realized the interesting potential and did not want to miss the opportunity. Respectively, Swiss bankers created tools for Muslim investors to enable them to gain exposure to the global equity market through their Islamic global equity instruments.

As a result of the increasing number of funds, soon Dow Jones Indexes was asked by fund managers to launch the first-ever range of Islamic indexes to track this growing market. With the launch of the Dow Jones Islamic Market Indexes in 1999, Dow Jones Indexes helped raise the profile of the industry globally. Many new financial institutions entered this market and within a year U.S. and European fund managers got ahead of the Swiss banks and became the largest managers of Islamic funds in terms of volume.

Their timing was poor, however. In 2001, the dotcom bubble burst and tech-heavy Islamic funds were severely hit by losses. Funds didn't start to regain their value until 2004 when local equity markets in the Gulf took off. This created a new trend - investing locally - that would last for a decade. Instead of continuing to invest in global equity markets, Middle East investors focused on their own markets. Local markets outperformed New York or London and Islamic investors in the region preferred to keep their money closer to home.

As a result, demand for Gulf equity funds was on fire. The value of the stock markets in the region surged along with oil prices, which peaked at $147 a barrel in July 2008. However, in the second half of 2008 GCC markets overheated as global markets crumpled amid the credit crisis.

SMALL MARKET

Even though Islamic funds have enjoyed two decades of strong demand, it remains a young and small industry. Many fund managers rushed into the market hoping to gain access to the huge pool of Muslim wealth only to realize that finding investors for their funds was more of a challenge than they had expected.

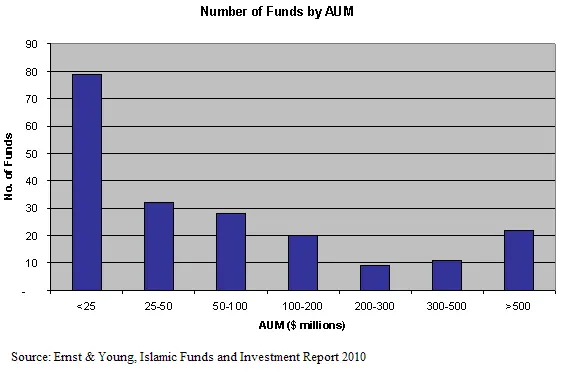

There are some Islamic funds of significant size but the majority remains below $20 million in value. The largest funds, with very few exceptions, are those managed by retail banks in Saudi Arabia, and to a lesser extent, Kuwait and the United Arab Emirates. Funds managed by Swiss private banks failed to raise new assets once Gulf equity markets took off in 2004. This was mainly due to investors' focus on local markets in the GCC, where returns were higher, than development markets such as the U.S. and Europe. Also, U.S. and other European fund managers had trouble to sign up new investors for their funds because they lacked the necessary distribution networks.

The percentage of households owning funds in the Middle East and the Gulf in particular, remains well below other emerging markets. This can be attributed to a number of factors including the lack of a savings culture within the region. Trading in real estate is more exciting than putting money in funds to watch them grow steadily over time.

ZAWYA NEWSLETTERS

Get insights and exclusive content from the world of business and finance that you can trust, delivered to your inbox.