In a report addressing the importance of Islamic Sukuk market and its impact on stimulating the Islamic economics

Increasing demand and popularity of products and structures compatible with Islamic Sharia'a following global financial crisis to form strong Sukuk demand base

KFHR Limited prepared a report on the Islamic Sukuk market. The report notes that the Sukuk market in 2011 will be driven by the recovery made in the global economic activities, flexible monetary policies, and sovereign fund-raising efforts to support economic growth as well as the revival of private sector projects. The report further predicts the entry of new players in the emerging markets, as well as new non-Islamic exporters willing to take advantage of Sukuk market with potential debut in Thailand, Japan and Europe, which will boost demand for Islamic Sukuk.

The following are the details of the report.

Global Sukuk Market 2010/ 2011

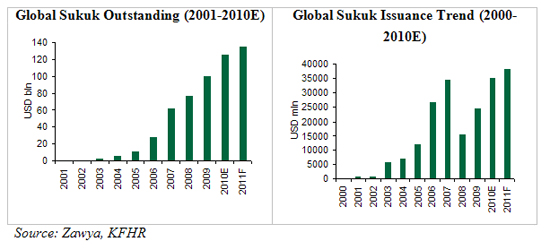

The sukuk industry has emerged as one of the main components of the Islamic financial system and has increasingly become an integral subset of the international financial system. Over the years, the sukuk market has grown by 10% to 15% annually to reach approximately USD100bln and contributed to 12% of the global Islamic finance assets in 2009. Prospects for the sukuk market remain bright. In 2009, global sukuk issuances surged by 58.8% yoy to USD24.7bln compared to the USD15.5bln raised in 2008.

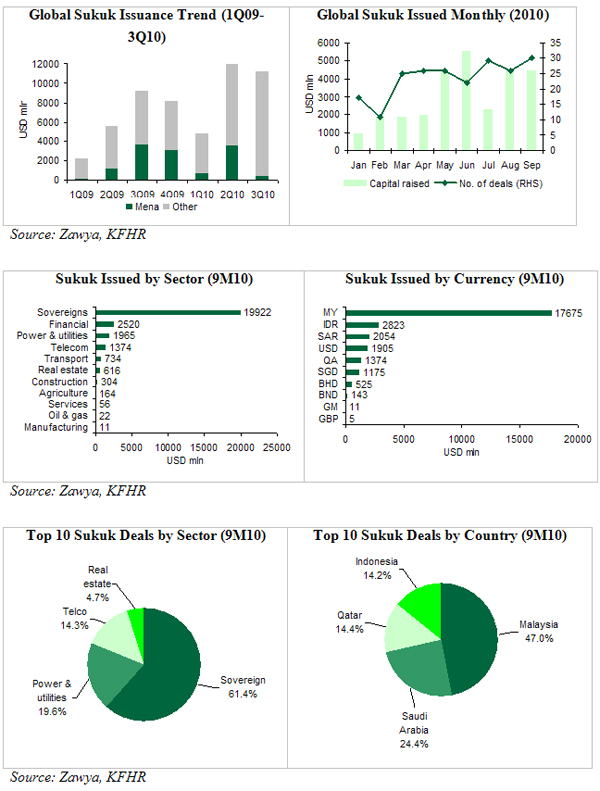

In the first nine months of 2010 (9M10), total sukuk issued globally increased further to USD27.9bln, 62.3% higher than the USD17.2bln raised in 9M09 and surpassing 2009 full year issuance of USD24.7bln. This was in line with a gradual global economic recovery and improved market condition and investor sentiment.

By issuer type, approximately 77.3% of 9M10's fundraisers were sovereign and quasi-sovereign entities, in line with the general interest of investors which saw a shift in preference to safe-havens and high quality issues. Financial services sector trailed behind at 9.8% of total sukuk issues while power and utilities sector stood at 7.6 %, driven by financial institutions' fundraising activities and continued infrastructure spending.

By country, Malaysia continued to dominate the global sukuk market, contributed to 72.3% of total value of sukuk issued in 9M10. Indonesia and Saudi Arabia trailed behind at 10.3% and 9.1% respectively. As such, by currency type, Ringgit-denominated sukuk deals topped at 63.8%, followed by Rupiah-denominated deals at 10.2% and Saudi Riyal-denominated deals at 7.4%.

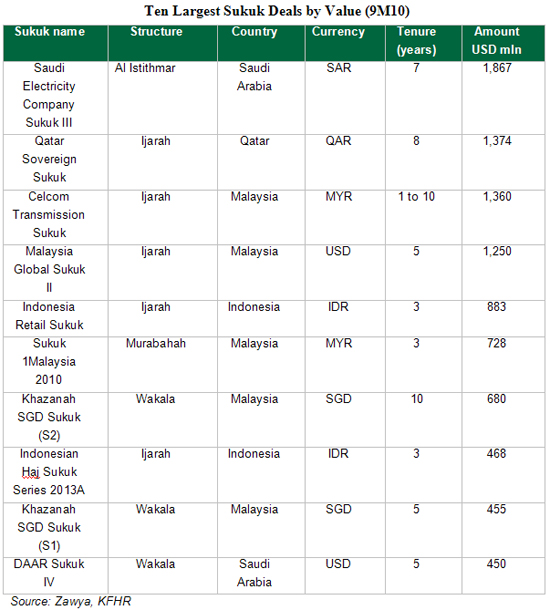

In 9M10, the ten largest sukuk deals accounted for USD9.52bln or 34.4% of total sukuk issued globally. Of the USD9.52bln, sovereign issues dominated at USD5.84bln or 61.4% of top ten sukuk issues, followed by power and utilities at USD1.87bln or 19.6% and telecommunication at USD1.36bln or 14.3%. By country, Malaysia led with an issuance size of USD4.47bln or 47.0% of top ten sukuk issues, Saudi Arabia at USD2.32bln or 24.4%, Qatar at USD1.37bln or 14.4% and Indonesia at USD1.35bln or 14.2%.

In 9M10, the largest local currency-denominated sukuk was a corporate issue from Saudi Arabia (SAR7.0bln or USD1.9bln equivalent) and the largest international USD sukuk was a sovereign issue from the Government of Malaysia (USD1.25bln). Other notable sukuk deals in 9M10 include a local currency-denominated sovereign issue from the Government of Qatar (QAR5bln or USD1.4bln equivalent) and SGD-denominated issues from Khazanah Malaysia Berhad via Danga Capital (totaling SGD1.5 bln or USD1.1bln equivalent).

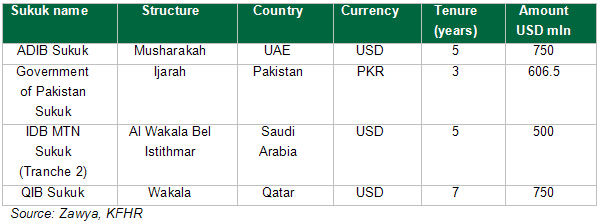

As of 18 November 2010, global sukuk issuance for the year thus far has surpassed our full year conservative estimate of USD30bln. Between end-3Q10 to 18 November 2010, the market saw a number of high profile international and domestic sukuk issues which include the following:

Based on the issuance momentum seen in 2010, the global sukuk issuance for 2011 is expected to surpass the USD34.2bln peak recorded in 2007, charaterised by the following:

- 2011 sukuk market will be driven by the recovery in global economic activities, accommodative monetary policies, continued sovereign fund raising to support economic growth as well as revival of private sector projects. The IMF projects World GDP growth of 4.3% for 2011 (2010: 4.6%), driven by robust growth in Asia, the Middle East and other emerging markets. This will ensure the revival of infrastructure projects on both the conventional and Islamic capital markets

- More sovereign issuers are anticipated to tap the sukuk market in 2011 as governments will continue to raise funds to support economic growth and fund fiscal deficits

- New emerging market players as well as new non-Islamic issuers are expected to tap the sukuk market with potential debuts from Thailand, Japan and Europe

- Increasing demand and popularity for Shariah compliant products and structures post the global financial crisis will form a strong demand base for sukuk

- Initiatives taken by various jurisdictions in developing legislative and regulatory frameworks, as part of efforts to attract foreign investments, would allow these new players to explore the sukuk industry for the first time

In gauging sukuk performance, according to the HSBC/NASDAQ Dubai US Dollar Sukuk index, which measures the difference between the average yield for sukuk and the London interbank offered rate (Libor), narrowed by 88.9bps to 378.5bps as at end-September 2010. As at 17 November 2010, sukuk spread over Libor tightened further to 352.1bps, reflecting stronger demand for sukuk as investors search for higher yielding assets vs. conventional investment in US Treasuries. According to the HSBC/ NASDAQ Dubai US Dollar Sukuk index, sukuk fetched an average return of 12.6% to investors thus far in 2010, significantly higher compared to US Treasuries average return of between 1.5% to 3.0% (across varying maturities).

It is important to note that the performance of the sukuk market will be affected/ dictated by world economic events (e.g. changes to fiscal and monetary policies, changes in sovereign ratings, financial market shocks in major economies etc) given that Islamic capital market exists within the global financial system.

Challenges that the sukuk market currently face include the following:

The demand for and supply of sukuk is still very much confined to Southeast Asia and the Middle East as international investors are still cautious of the GCC after the Dubai World debt restructuring. This is reflected in the higher yield premium investors demand to hold GCC debt. For instance, the extra yield investors demand to hold Dubai's 5-year government sukuk vs. Malaysia's 5-year government sukuk stood at 367bps as at 15 November 2010.

Secondary market liquidity remains a challenge for USD sukuk issues as existing sukuk investors prefer to hold these papers to maturity, and this is especially true for good quality sukuk issues which are usually rare and difficult to come by.

The cost for potential sukuk issuers tends to be more than non-Islamic debt because of the fees paid to Shariah advisory boards, thus putting them at a disadvantage over their conventional counterparts.

-Ends-

© Press Release 2010