10 April 2012

While the region continues to witness fresh supplies of residential units, the office space segment is faring no better, with new square metres of commercial floors coming on to the market.

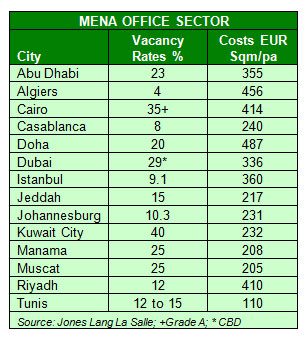

Average MENA prime office vacancy rates stand at or over 20%, according to Global Investment House.

In Kuwait City, average vacancy rates in office buildings average 40%, with Cairo (35%), and Dubai (29%), a distant second and third.

Abu Dhabi, with 23% vacancy rate, and Doha, with 20%, suggest the regional markets are awash with office supply.

Only Jeddah (15%) and Riyadh (12%), show a smaller gap between demand and supply, but they are merely playing catch up with their regional counterparts.

While that is great news for Gulf corporations and small businesses, it has left developers and individual investors in office real estate with an albatross around their necks.

"We have a negative outlook on all five office markets under coverage. Average prices and rents have dropped during 2011 on four of the five markets we cover on the back of high oversupply and stagnant demand growth," notes Global Investment House in a note to clients.

"Riyadh, the exception, saw some increase on average rents due to tenant upgrades, rather than demand growth, as new higher quality supply was made available. In our view, vacancy rates will increase and rents will drop in 2012 on new supply entering all five markets."

However, Global expects Riyadh vacancy rates to increase in the next two years as new high quality supply of 818,000 sqm, equivalent to 25% of 4Q11 offering, enters the market between 2012 and 2014. "Jeddah is expecting a larger 31% addition to its 4Q11 supply as an additional 159,000 sqm become ready for delivery in 2012," notes the Kuwait-based bank in a not to clients.

Riyadh, which has one of the highest costs per square metre in the region, is increasingly becoming favourable for occupiers, adds Jones Lang La Salle, an international real estate research consultancy.

"On the demand side, public sector entities remain the biggest source of competition, benefiting greatly from the country's huge stimulus measures," notes JLL in a report. "In the private sector, local conglomerates and consulting/engineering firms have been among the most active occupiers, while competition for space from multinational companies remains subdued. Relocations and upgrades to higher quality stock are being driven by the offer of improved workspace, security and increased parking. The number of serviced offices is on the rise, with Servcorp and Regus acquiring new space in 2011."

JLL expects some projects to be delayed but the overall trend appears to be downward pressure on prices.

DUBAI SUPPLY

Despite a slowdown in construction, the emirate added 800,000 square metres in office space 2011, with another 1.1 million square metres set to be delivered this year.

Areas such as TECOM, Jumeirah Lake Towers and Business Bay are all expected to come under pressure, although they held up much of last year.

Prime rents in the Dubai International Financial Centre remained flat at AED 2,370 per sq m per annum, while rents elsewhere in the central business areas remained stable at AED 1,615 per sq m per annum, says JLL.

"Costs for secondary quality space as well as buildings in secondary locations, continued to decline on the back of the large amounts of vacant space and subdued demand levels. The gap between asking and achieved rentals also continues to widen as landlords compete aggressively for tenants offering generous incentives and terms.and retain tenants," said JLL.

Abu Dhabi can also brace for a further drop in rental prices as more supply comes into the market to add to the 79,000 square metre built in the fourth quarter of 2011.

While costs continue to decline, landlords are throwing in fit-out contributions as an incentive to attract tenants.

CB Richard Ellis reports even greater incentives: Landlords are becoming increasingly flexible and realistic in their approach to leasing, with rent-free periods offered as standard market practice. For occupiers with strong covenants, extended rent-free periods of up to eight months per five years of term can be secured as landlords try to limit their risk exposure by avoiding extended rental voids.

"Rents were recorded at AED 3,800 in Q4 2011, with average effective rents for Grade A space standing at AED 1,700 per sq m per annum, down 55% from their peak," says JLL. "These average rates have been exceeded in a small number of buildings, mainly occupied by the oil and gas sector as well as government institutions. The gap in costs between Grade A and B space is expected to widen further."

KUWAIT CITY WORST HIT

Kuwait City is the worst hit with average vacancy rate of 40%, with up to 70% in new towers in central location, according to Global.

"Further pressure is on sight with an estimated addition of 1.2 million sqm; 30% to the existent stock is currently in the pipelines. Average office rents dropped by 22% during the year as average rents stood at KWD5-7 per sqm," says Global.

Kuwait City's fortunes are in sharp contrast to Doha, which commands nearly double the cost per square metre. The city has enjoyed the gas-led boom and has remained resilient despite the Arab Spring crisis, with the newly-built Tornado Tower and Al Fardan Commercial Tower, fully occupied.

"However, apart from a few large requirements, many companies are seeking office space in lower unit sizes, with most requirements being for space less than 500 sq m, notes JLL. "This continues to cause a mismatch between existing supply and the demand profile."

While the region continues to witness fresh supplies of residential units, the office space segment is faring no better, with new square metres of commercial floors coming on to the market.

Average MENA prime office vacancy rates stand at or over 20%, according to Global Investment House.

In Kuwait City, average vacancy rates in office buildings average 40%, with Cairo (35%), and Dubai (29%), a distant second and third.

Abu Dhabi, with 23% vacancy rate, and Doha, with 20%, suggest the regional markets are awash with office supply.

Only Jeddah (15%) and Riyadh (12%), show a smaller gap between demand and supply, but they are merely playing catch up with their regional counterparts.

While that is great news for Gulf corporations and small businesses, it has left developers and individual investors in office real estate with an albatross around their necks.

"We have a negative outlook on all five office markets under coverage. Average prices and rents have dropped during 2011 on four of the five markets we cover on the back of high oversupply and stagnant demand growth," notes Global Investment House in a note to clients.

"Riyadh, the exception, saw some increase on average rents due to tenant upgrades, rather than demand growth, as new higher quality supply was made available. In our view, vacancy rates will increase and rents will drop in 2012 on new supply entering all five markets."

However, Global expects Riyadh vacancy rates to increase in the next two years as new high quality supply of 818,000 sqm, equivalent to 25% of 4Q11 offering, enters the market between 2012 and 2014. "Jeddah is expecting a larger 31% addition to its 4Q11 supply as an additional 159,000 sqm become ready for delivery in 2012," notes the Kuwait-based bank in a not to clients.

Riyadh, which has one of the highest costs per square metre in the region, is increasingly becoming favourable for occupiers, adds Jones Lang La Salle, an international real estate research consultancy.

"On the demand side, public sector entities remain the biggest source of competition, benefiting greatly from the country's huge stimulus measures," notes JLL in a report. "In the private sector, local conglomerates and consulting/engineering firms have been among the most active occupiers, while competition for space from multinational companies remains subdued. Relocations and upgrades to higher quality stock are being driven by the offer of improved workspace, security and increased parking. The number of serviced offices is on the rise, with Servcorp and Regus acquiring new space in 2011."

JLL expects some projects to be delayed but the overall trend appears to be downward pressure on prices.

DUBAI SUPPLY

Despite a slowdown in construction, the emirate added 800,000 square metres in office space 2011, with another 1.1 million square metres set to be delivered this year.

Areas such as TECOM, Jumeirah Lake Towers and Business Bay are all expected to come under pressure, although they held up much of last year.

Prime rents in the Dubai International Financial Centre remained flat at AED 2,370 per sq m per annum, while rents elsewhere in the central business areas remained stable at AED 1,615 per sq m per annum, says JLL.

"Costs for secondary quality space as well as buildings in secondary locations, continued to decline on the back of the large amounts of vacant space and subdued demand levels. The gap between asking and achieved rentals also continues to widen as landlords compete aggressively for tenants offering generous incentives and terms.and retain tenants," said JLL.

Abu Dhabi can also brace for a further drop in rental prices as more supply comes into the market to add to the 79,000 square metre built in the fourth quarter of 2011.

While costs continue to decline, landlords are throwing in fit-out contributions as an incentive to attract tenants.

CB Richard Ellis reports even greater incentives: Landlords are becoming increasingly flexible and realistic in their approach to leasing, with rent-free periods offered as standard market practice. For occupiers with strong covenants, extended rent-free periods of up to eight months per five years of term can be secured as landlords try to limit their risk exposure by avoiding extended rental voids.

"Rents were recorded at AED 3,800 in Q4 2011, with average effective rents for Grade A space standing at AED 1,700 per sq m per annum, down 55% from their peak," says JLL. "These average rates have been exceeded in a small number of buildings, mainly occupied by the oil and gas sector as well as government institutions. The gap in costs between Grade A and B space is expected to widen further."

KUWAIT CITY WORST HIT

Kuwait City is the worst hit with average vacancy rate of 40%, with up to 70% in new towers in central location, according to Global.

"Further pressure is on sight with an estimated addition of 1.2 million sqm; 30% to the existent stock is currently in the pipelines. Average office rents dropped by 22% during the year as average rents stood at KWD5-7 per sqm," says Global.

Kuwait City's fortunes are in sharp contrast to Doha, which commands nearly double the cost per square metre. The city has enjoyed the gas-led boom and has remained resilient despite the Arab Spring crisis, with the newly-built Tornado Tower and Al Fardan Commercial Tower, fully occupied.

"However, apart from a few large requirements, many companies are seeking office space in lower unit sizes, with most requirements being for space less than 500 sq m, notes JLL. "This continues to cause a mismatch between existing supply and the demand profile."

© alifarabia.com 2012