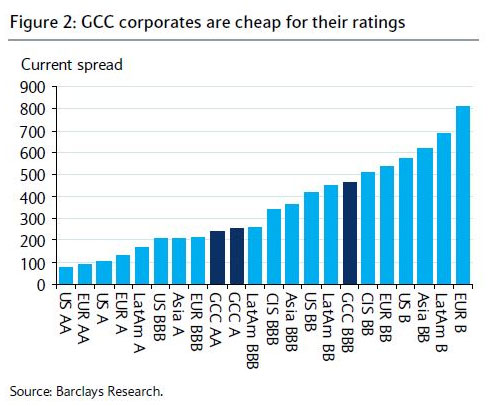

While the Gulf markets have enjoyed a good year so far, GCC debt market has not been able to reverse its year-to-date underperformance versus other emerging market benchmarks.

"While global EM credit funds have enjoyed healthy inflows, most GCC credits are not included in global EM benchmark indices and may thus have been unable to benefit from these flows to the full extent," said Andreas Kolbe, an analyst at Barclays Capital.

Gulf corporate earnings were strong in the first quarter and the healthy inflow of hydrocarbon-related revenues and government spending in the economies should give investors the confidence to participate in the bond bonanza that's gathering steam.

Investors have been wary ever since they were stung by Dubai's debt crisis over the past few years, but stressed government-related entities such as Dubai Investments and Jebel Ali Free Zone are now working with creditors. DIFC has USD1.25-billion Islamic bond in June while JAFZA has a USD2-billion sukuk maturing in November.

Various Dubai entities still have USD12.2-billion in debt negotiations outstanding, according to Exotix Investment research. This includes USD6-billion debt by the Dubai Group, which may be problematic.

"News reports reveal that international lenders are losing patience and might resort to legal action," said Exotix in a note. "A Dubai govt back-stop will not be provided, yet the govt has agreed to subordinate its shareholder loans (USD3.5bn in total, which is not included in the USD6bn figure). UAE banks account for 60% of lenders by USD exposure."

Other outstanding debt includes Drydocks World (USD2.2-billion), Zabeel Investments (USD1.6-billion), Dubai Holding Investment Group (USD1.2-billion) and Limitless (USD1.2-billion).

With much of Dubai's debt issues being resolved, and the rest of the major economies and corporations in Abu Dhabi, Saudi Arabia and Qatar in enviable fiscal positions, Barclays Capital believes the Gulf's underperformance has created entry points.

Another reason for the Gulf lagging behind was the threat of an Israeli attack on Iran, which is receding by the day as the Tel Aviv government dithers and discussions between western powers and Tehran get under way.

"We think that the year-to-date underperformance is mainly based on technical factors. Global EM credit funds have enjoyed solid inflows over the past couple of months. However, as most GCC credits are not included in benchmark EM indices, the region likely has benefited less from the robust stream of inflows than other regions (such as Latin America or CIS states)."

Barclays top picks include Rasgas, Dolphin Energy, DP World and Dubai Holding debt.

TUNISIAN PROMISE

Elsewhere in the region, Tunisian bonds also offer tremendous potential, especially as they have hardly benefited from the constructive environment for

emerging market credit year-to-date.

"We think this underperformance is unjustified. Tunisia's growth has recovered to almost positive territory (although the subdued EU growth outlook remains a major downside risk). Steady improvement in the political situation has encouraged gradual but steady returns of tourists and FDI, though in small steps, and improvement in exports," Barclay's Kolbe said.

Tunisia has also been bolstered by Qatar's purchase of USD500-million government bonds which would go a long way in alleviating budgetary issues.

NEW DEBT

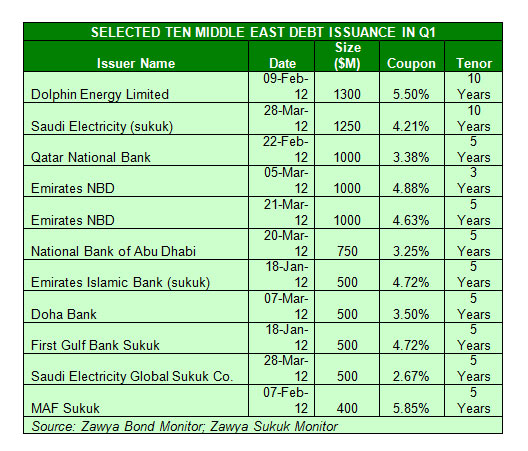

A renewed focus on MENA credit is under way as companies seek to take advantage of rising regional business opportunities. Not surprisingly, four of the six regional funds launched in March were focused on fixed income, according to Zawya Funds Monitor.

Middle East debt issuance in the first quarter doubled to USD11-billion compared to the same period last year. These included Doha Bank's USD500-million (coupon: 3.5%), Qatar National Bank's USD1-billlion bond (3.375%), Emirates NBD's USD1,000-billion bond (4.875%) and Dolphin Energy's USD1.3-billion bond (5.5%), according to Zawya Bonds Monitor.

RISE OF FINANCING

While the collapse of the euro and a slowdown in China remain real threats for the global economy, MENA and Gulf markets have seen massive uptick in investor and business confidence.

Another example of improved investor sentiment is rising equity market and greater talk of initial public offerings, as companies feel confident in stepping back into the market to raise financing.

The potential of Qatar and UAE being upgraded to the MSCI emerging market status would also help raise the region's profile as an investment destination and attract new sources of investments, across the spectrum of opportunities - in debt and equity.

Given the expansionary policies under way in the Gulf, bond issuance looks set to grow as companies explore all forms of funding to take advantage of the regional governments' massive investment programme.

© alifarabia.com 2012