MENA a promising and growing investment landscape for PE funding

The region is challenging but provides the largest global opportunity in private equity, writes H. Richard Dallas of Gulf Capital.

ZAWYA

February 27, 2013

27 February 2013

Private equity as an asset class has become a popular choice for investors across the world. With the world becoming increasingly globalized, investors are expanding and diversifying their geographic footprint towards emerging markets, including the Middle East and North Africa (MENA) region, in search of higher returns than may be available in more developed markets with stagnating or slow economic growth. Businesses and investors are recognizing the potential of the MENA region as a promising, growing investment landscape.

The region has undergone structural reforms in the past 30 years necessary to support economic growth for an expanding and youthful population base. The reforms have improved governance and encouraged economic participation of the local population through government financial stimulus, especially in oil producing countries with abundant liquidity. This, in turn, has generated a more stable investment environment for local and international investors and has opened doors to fresh investment opportunities. In recent times, the Arab Spring has also forced governments to further speed up reforms that encourage transparency in government and private sectors in order to shore up investors' confidence and create opportunities for new investments.

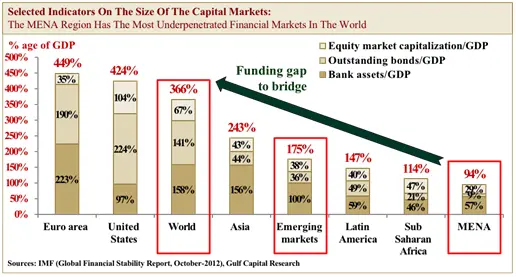

However, there is still a relatively limited pool of capital available to support these new investment initiatives in emerging markets. According to the Global Financial Stability Report released in October 2012 by the International Monetary Fund, the total size of MENA equities, bonds and bank assets amounted to around 94% of GDP, compared to other emerging market and world averages of more than 175% and 366% respectively. Therefore, in most instances, traditional sources of funding are not as readily available to support growth for business needs.

With the recent global economic downturn, coupled with the uncertainty from the Arab Spring events, capital raised from local banks and public markets has become increasingly difficult to secure, especially for small and medium-sized enterprises (SMEs). Regional financial institutions are hesitant to provide debt funding to SMEs and other corporate entities that need it for growth. Liquidity raised on the regional stock markets has not yet recovered to its historic levels, IPO markets still lack new issuance and trading volumes on the secondary markets remain volatile. Out of the total primary equity issuance of USD 50 billion since 2005, around only 11% was raised during the past three years. Within this environment, the private equity industry can fill an important part of the large funding gap and, thus, capture an increasing share of the regional corporate financing needs.

ZAWYA NEWSLETTERS

Get insights and exclusive content from the world of business and finance that you can trust, delivered to your inbox.